Over the past few issues, I’ve focused our investor education content on how to use basic corporate finance principles to start managing your short term cash flow needs and reduce portfolio drag.

But once you’ve captured all of those easy wins, and you’ve done what yo//u can to improve cash flow and credit metrics…

Now we can get into the “fun part,” where we start to look at deals, make investments, and manage our portfolio.

Let’s dive in,

Jake Hoffberg

P.S. We appreciate that for many people, their life savings is not a game.

However, we choose to present our investor education as a game, because the purpose of games is to develop key skill sets you can use in the real world (and hopefully have fun along the way).

As a reminder, securities sold under Reg CF, Reg A, and Reg D are often considered high risk and speculative in nature. Please do not invest funds you cannot afford to lose, or otherwise need immediate access to.

The Big Idea

Outsider Portfolios vs Insider Portfolios

As a general consideration, we all want to get the highest returns possible, with the least amount of risk.

But here’s the problem with risk. It’s notoriously hard to quantify and price correctly. That’s why you’ll often hear financial professionals talk about something called “non-correlated risk.”

If two assets are considered to be non-correlated, the price movement of one asset has no effect on the price movement of the other asset.

Said another way, we don’t want all of our assets to be exposed to identical risk factors; if the “risk” actually happens, it impacts everything.

If you’re an “Insider” to the capital markets, you’ve got access to a wide variety of financial products and trading strategies that seek to offer this non-correlated risk…

But when you’re an “Outsider” to capital markets, chances are you wind up with an “off the rack” portfolio that looks something like this:

If you’re in your older years, you might be in the classic “60% equities, 40% bonds” (called “60/40”) portfolio.

According to Vanguard: The goal of the 60/40 portfolio is to achieve long-term annualized returns of roughly 7%.

But here’s the problem. Even if those returns were guaranteed – which they aren’t – it takes ~10 years to double your portfolio at a 7% compound annual growth rate (CAGR).

If you want to 3x your portfolio over the next 10 years, you need a ~12% CAGR. 5x in 10 years requires ~17.5% CAGR. 10x in 10 requires ~29% CAGR.

Now, depending on your risk tolerance and time horizon, you might be comfortable moving into a more aggressive portfolio model and taking on more risk…

But here’s the perennial problem with concentrating all of your assets into a model portfolio that ONLY has publicly traded securities:

There’s essentially no meaningful diversification from stock market risk… which is the whole point of diversification in the first place.

That’s why Private Capital Insiders (like family offices, high net worth individuals, and institutions), have portfolio allocations that look something like this:

In this model, the traditional 60/40 is collapsed into a 27/6 (or ~33% of the total portfolio allocation)…

But, nearly half of the portfolio is invested in Private Equity and Real Estate.

On April 20, 2023, Founder and Chairman of TIGER 21, Michael Sonnenfeldt, was featured on CNBC’s Street Signs Europe to discuss how the group’s Members have changed their asset allocation in recent quarters.

Private equity has become the membership network’s largest allocation at 31%, surpassing real estate for Q4 2022. Despite the pullback in allocations, 70% of Members are still looking for new opportunities in real estate for the next year.

Historically, Members held around 12% cash, but more recently, have pulled back to 10%, signaling that they are still comfortable with long-term investments that hold value yet continue to hold cash to weather any storm.

Insiders don’t invest this way by mistake. They do it because the historical evidence suggests adding alternative investments provides persistent outperformance.

- Private Equity investors are looking to generate 20% – 30% annual returns.

- Opportunistic Private Real Estate funds are looking for 16% – 20% annual returns.

This is great news if you’re an investor like the Yale Endowment Fund, with billions of dollars in AUM (Assets Under Management) and a multi-decade time horizon. Over the past 30 years, Yale’s investments have returned an unparalleled 13.1% per year (or a whopping 40x multiple).

Up until recently, the only realistic option for retail investors to add Real Estate and Private Equity to their portfolio is to become a landlord or a business owner.

Thanks to the exempt offering frameworks found in the JOBS Act, we’re starting to see increased retail access to these private asset classes.

And thanks to a groundswell of support for expanding retail access to private asset classes, we could see a massive expansion of opportunities, as Wall Street firms increasingly view Retail Money as the final frontier of available capital.

Here’s why…

On January 14th, 2020, John Finley – Chief Legal Officer at Blackstone – gave a presentation to the SEC titled “Expanding Retail Access to Private Markets”

In it, he revealed some rather shocking numbers…

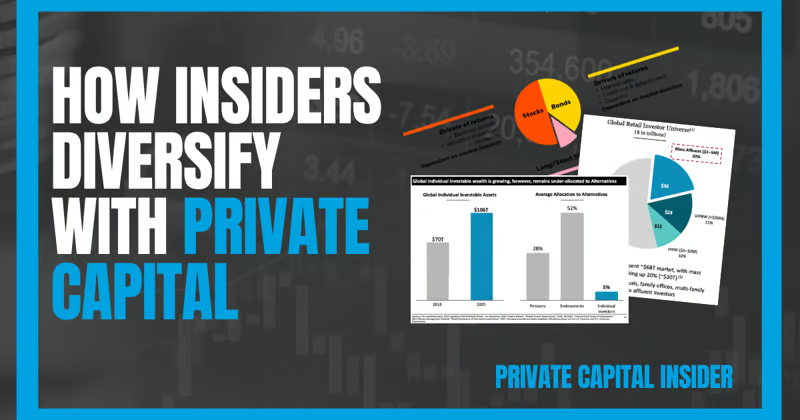

Retail investors represent ~$68T of global assets, with $1-$5m households representing roughly $30T of assets (or ~20% of all global assets).

But that’s just the tip of the iceberg…

By 2025, the total pool of retail assets is expected to balloon to $106T worldwide!

This means every 1% of assets re-allocated to alternatives represents as much as $1.06T of money in motion.

Combined with the explosive growth of retail traders entering the markets since the start of COVID-19, we could see a radical shift in the way capital markets function.

“It’s a land grab,” said Matt Brown, chief executive of CAIS, a platform that gives independent financial advisers access to so-called alternative investment products. “You’re seeing the mutual-fund boom 2.0,” he said, referring to the rise in popularity of mutual funds during the 1990s.

To prove the point, here’s Blackrock’s new push to add alternative investments into the 60/40 portfolio.

According to Blackrock’s website:

Long/short strategies have two major benefits for 60/40 portfolios.

First, by going short companies, they can greatly expand the opportunity set to generate returns. Second, by going long and short in equal amounts, they can tap into changes in security dispersion.

Dispersion is independent of market direction, and can act as a new source of return that is not available in the 60/40 framework.

Is this a good idea? I have no idea (and chances are, neither do you).

But I do know that you’re going to get pitched more and more of these types of “just add alts!” solutions in the coming years ahead.

So before you start adding in some of that “alternative” magic to your portfolio, the first thing you need to do is create a plan.

More on that in just a moment, but first, a quick poll.

Playbook

A Primer on Portfolio Construction

If I had to sum up the single biggest problem retail investors (i.e. “Outsiders”) have when managing their own money, it’s this:

Outsiders make investment decisions based on an emotionally driven financial model that takes into account Hype, the Fear of Missing Out, and Fake Scarcity.

On a regular basis, we receive emails from our members asking something to the effect of “Should I invest in [XYZ]?” or “Is [XYZ] a good investment?”

Besides the fact that we legally can’t answer this question, as it would be considered “individualized advice”…

It’s impossible to determine the merits of any single investment opportunity on its own. You need some sort of criteria by which to judge the opportunity.

For this reason…

Insiders make investment decisions based on an assumption-driven financial model that takes into account their financial goals, the required rate of return to achieve those goals, the current cost of capital, and all available investment opportunities at that time.

What is an assumption-driven financial model?

As the name suggests, it is a mathematical representation of what could happen in the future (a model), based on certain assumptions about the future.

In corporate finance, the assumption-driven model is then used to build something called a Pro Forma.

For example, a company will report its actual sales and expenses for the quarter that just passed (historical financials), in addition to its forward-looking revenue projections.

What does this have to do with managing your personal portfolio?

Investors and corporate management are in the same fundamental business: applying scarce resources toward the best long-term outcomes (called “capital allocation”)

How do they determine where those best long-term outcomes are?

It all starts with building a financial model, defining your key assumptions, and then managing your risk along the way so you don’t blow yourself up.

Remember: All capital has a cost.

If you have money sitting in cash right now, there’s a cost to using that capital (opportunity cost, downside protection).

If you need to raise capital by selling an asset, you’ll likely have to pay fees and taxes to convert it to cash.

If you have to borrow it, it means paying interest.

So before you start taking flyers on sexy sounding investment opportunities with a chance at 10x-100x+ returns…

Do yourself a favor, and ask yourself a few simple questions:

- What is my current portfolio allocation model?

- Where in my model does this investment opportunity fit?

- Why am I investing in this, and not adding to my existing positions?

- Do I understand the risks, and am willing to take them?

- Where is the money for this investment coming from?

- Is this the best use for this capital?

Final Thoughts

As Kevin Ashton, author of How to Fly a Horse: The Secret History of Creation, Invention, and Discovery, once said, “The greatest test of your expertise is how explicitly you understand your assumptions.”

If you don’t understand that (a) there should be a financial model; (b) that model has assumptions; (c) you can – and should – challenge those assumptions, and model what happens if those assumptions change…

It’s hard to describe what you’re doing as “Investing.”

More to the point, if anyone is managing money on your behalf – and you don’t understand the assumptions of the model they’re using – don’t be afraid to ask questions.

The #1 thing we don’t want to see in the model is something that looks like the famous Sidney Harris cartoon “Then a Miracle Occurs.”

Or for those who are young enough to have seen the famous “Underwear Gomes” episode from South Park…