If we believe the secret to successful investing is to correctly identify trends before the market has reached a new consensus on price (i.e., we are narrative driven investors)…

lmost by default, this means we need to have access to information BEFORE it becomes mainstream.

And perhaps more importantly, we need to have the courage and conviction to invest in unloved, out-of-cycle, and under-invested segments of the markets.

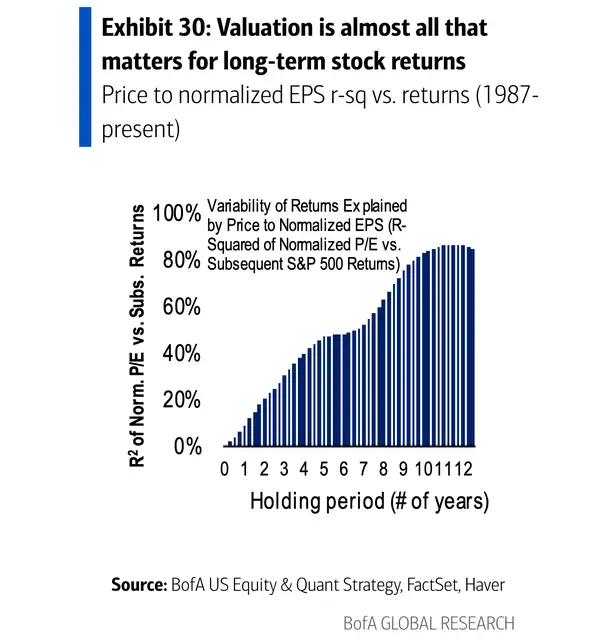

Why? Because according to Bank of America, valuation levels explain 80% of the market’s return over a 10-year period.

And if we are to believe this one simple idea is true – that the valuation we invest at is arguably the most important factor…

Is price the only thing that makes a “good deal” good?

That’s the topic of today’s issue of Private Capital Insider.

-Jake Hoffberg

Private Investor Networking: Unlocking your biggest competitive advantage in private markets

In a previous issue of Private Capital Insider, we talked about one of the “secret weapons” for investing in private markets…

Networking!

According to Denis Shapiro, author of The Alternative Investment Almanac: Expert Insights on Building Personal Wealth in Non-Traditional Ways,

I came to the realization that the stock market was a great tool for asset appreciation, but unfortunately, the benefit of its almost universal liquidity comes with unlimited volatility which, in turn, creates income uncertainty.

Luckily, what also began to emerge during my research for better ways to pick stocks and become a better landlord was a specialty in a certain skill set: networking.

My network started to serve as the foundation for everything I did as an investor.

Why? Because if you don’t have proprietary data – and ideally, access to that information before other people do – it’s extremely difficult to gain any sort of “edge” when investing…

Especially as a small balance check writer!

For clarity, this isn’t to suggest trying to get ‘inside the company’ information before it is public, as trading on inside information is almost always illegal.

What we’re talking about is underwriting and due diligence; gaining knowledge and insight into sectors, industries, and business models from “Insiders” in those specific niches… in an effort to gain a greater understanding of the risk/rewards within those types of investment opportunities.

This is especially important within opportunities where there is limited sources of real time data and “boots on the ground” information sources.

That’s why earlier this week, I decided to attend a monthly social event hosted by a national angel investor community – at a rather swanky restaurant – to do some “boots on the ground” investigating.

After I feasted on the upscale burgers (aka “sliders”) and pizza (aka “flatbread”) – not to mention, spent the ~$26 + tip that cocktails cost in places like this…

I had the chance to talk to a handful of entrepreneurs, investors, and fund managers about what they’re investing in (as well as why they like this specific angel group).

So, what did we talk about?

When we weren’t talking about how awesome it is to retire in your 40s and 50s, thanks to a significant liquidity event… not to mention the many houses, boats, cars, bottles of scotch, and cigars they have…

The conversation eventually centered around some version of…

To no surprise, many of the now-retired software engineers sitting on an 8-figure nest egg like to invest in software companies involved in spaces where they’ve built software.

A startup attorney I talked to – who told me plenty of war stories of deals gone bad – was very excited about a cyber security deal he was working on (not to mention anything AI).

A former CEO of a biotech company was primarily investing in real estate (I unfortunately didn’t get to ask him much about it).

And a fund manager with 20 years of investing experience said “I’m not a venture investor, and I don’t like to invest in startups. I want to invest in profitable companies that can scale.”

None of these answers were particularly surprising…

But what was surprising is the response I got from almost everyone when I told them what I like to invest in…

Well underwritten deals that are structured (and priced) in a way that allows me to generate an attractive return within 18-36 months (not 7-10 years), ideally via an IPO so I can hold my position longer if I want to…

Here’s why…

As a small-balance check writer who is investing my own money – not a fund manager getting a guaranteed salary to take risk with other people’s money…

- I am obsessive about managing downside risk.

I’m sure we can all agree that we’re looking for above-market returns to compensate for the risk we’re taking…

But that doesn’t mean I want to take stupid risks in order to chase returns.

- I care a lot about liquidity

I don’t want to be stuck in a fund for 7-10 years, I want to be liquid in 18-36 months.

- I want to invest in actual companies, run by competent operators, who are focused on growing enterprise value and profitability.

Why? Because good products don’t necessarily make good companies… and good companies don’t necessarily make good investments.

But good investments often have one important thing in common… They can get access to all the money they need because investors trust managements’ ability to forecast results.

In other words, the company has excellent financial controls, reporting systems, and governance.

That’s why, for the most part, I don’t care about:

- Massive Total Addressable Markets: Big markets almost always mean competing against cashed-up competitors and entrenched incumbents, which in turn means raising a LOT of money – and probably operating at a loss – for a long time.

With my small check size, I’d rather invest in a business that will need less than $30m (ideally less than $15m) in total equity capital to reach profitability in the next 18-36 months.

- What sector they operate in: In fact, I almost prefer it if they’re not in a “hot” sector. Ideally, I am investing in “out of cycle” deals that will turn “hot” as I approach the desired exit window (18-36 months).

This gives me a better chance to “buy low, sell high” instead of trying to “buy high, sell higher”

- What they sell (only that there is existing demand for the solution): you do not need to “change the world” or have “breakthrough technology” to sell products and services to customers looking to buy. But you will need enormous amounts of money to convince people to buy things they don’t already want.

If the company hasn’t figured out what their product is and how to sell it – or can’t otherwise prove there is existing demand they can snap into – that is a hard pass for me.

“Sales and marketing” is where money goes to die.

- A visionary founder or tech wunderkind: Before you see them on trial for whatever fraud or ponzi scheme they were running, you probably saw them on the cover of Forbes or giving a TedTalk somewhere.

While charismatic people often attract investor attention, I have no interest in using my money to pay for expensive people to do research and development.

“R&D” is also a place where money goes to die.

- A name brand investor: I would probably prefer there isn’t any institutional level money in the deal, as that probably means I’m going to be paying up.

In fact, we’ll take it a step further…

To some degree, the ONLY thing I care about is “who am I going to sell my shares to at a future date?”

Because like it or not, if you’re investing in early-stage companies, this is almost certainly the ONLY way you’re getting a return on capital.

And to bring our conversation back to its beginning…

This is the reason why valuation/price is one of the most important factors of a “good deal.”

In the Game of Money, almost everything can be explained through supply and demand.

For example, there is a nearly infinite demand for money with a finite supply of it.

In a nutshell, that’s what makes the “money business” such a great business.

And if you’re in a position where you are one of a few suppliers of capital, in a niche that you understand very well…

This gives you an enormous “edge” over larger investors in broader asset classes.

However, as a small-balance check writer, you have to manage this supply/demand imbalance on the frontend (i.e., you can get in at a good price on favorable terms)…

With all of the capital requirements on the backend (i.e., the company can continue to raise capital on attractive terms that protect your equity).

The only problem? Because you are a small check writer, you have no real ability to underwrite the deal, price the deal, or otherwise negotiate the terms.

And more to the point, you have no ability to control the deal once you’re in it, in order to protect your position on the cap table, or otherwise drive business results.

So how do you get yourself into this “good deal” goldilocks zone where you can get your small check in the deal BEFORE a major inflection point that drives valuation?

In many ways, it means you need to invest alongside a “banker” – sometimes called a sponsor or lead investor – who can do this work for you.

It’s easier to underwrite a banker than it is to underwrite an individual investment

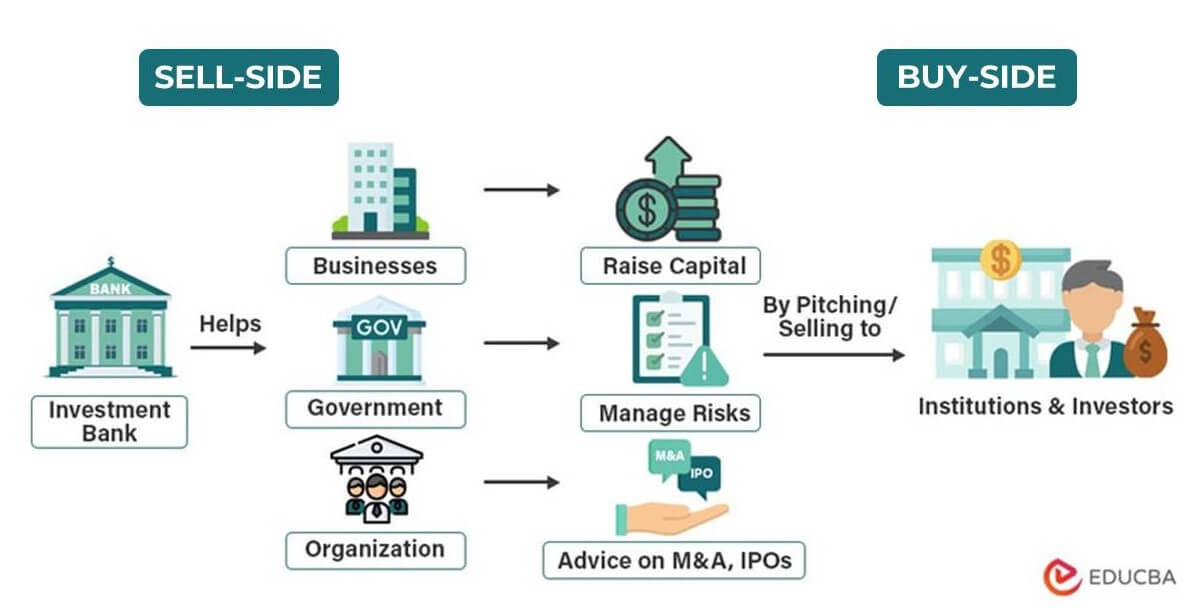

If Equifund operated inside of the “normal” institutional channels, we would probably be considered an “investment bank” or “sponsor” of some kind (i.e., we are on the sell side).

And if we wanted to get distribution from the traditional broker/advisor channel in order to get our offering “recommended” to their clients…

Chances are, they would spend more time underwriting Equifund as a firm than they would underwriting an individual offering.

Why? Because underwriting is time consuming – it takes the same amount of time to underwrite a $5-10m financing as a $50-100m financing, but you can put more capital to work in the larger deal (and it’s probably lower risk).

But if the advisor has a relationship with the sponsor, understands how they think about deal structuring and valuation, and there’s an assumption of good governance…

It’s kind of like going to a restaurant where the chef knows what you like to eat, and no matter what you order, it’ll be something you’ll enjoy.

And for the chefs in our restaurant, underwriting and due diligence is all about looking to properly price in the execution risk of the stage we’re in right now.

Great management teams want to work with Equifund because we offer them an attractive proposition – for great operators who aren’t great fundraisers, we will help you raise all the capital you need, while you focus on growing the business.

And as long as management teams can accept a lower valuation on the frontend to compensate our members for the execution risk at this early stage…

When they raise their next round of financing, assuming they achieved their forecast, it sets them up to be in an excellent position to continue raising capital at higher valuations on more favorable terms.

And if there is always a market for the company’s equity, because it’s priced correctly for the market environment we’re in…

It means we – the small-balance check writers – have far more opportunities to sell our shares to someone else.