A self-directed IRA LLC (SDIRA LLC) offers a range of benefits for investors looking to diversify their portfolios and take direct control of their retirement savings.

Unlike a standard IRA, a SDIRA LLC gives you the flexibility to invest in real estate, private equity, crowdfunding projects, private loans, cryptocurrencies, and more.

Take Peter Thiel for instance. The billionaire investor famously used his self-directed Roth IRA to invest in private companies like PayPal and Facebook—amassing over $5 billion tax-free.

With a self-directed IRA LLC you also gain checkbook control, which eliminates the need for custodian involvement.

In this article, we’ll delve into the workings of self-directed IRA LLCs, exploring its benefits, regulations, and how you can leverage it to potentially grow your wealth exponentially.

Key Takeaways:

- Greater Control: By setting up a self-directed IRA LLC, investors have the power to make investment decisions quickly without relying on their SDIRA custodian.

- More Investment Options: With the LLC structure, investors can diversify into alternative assets, which can potentially enhance the returns of the IRA.

- Liability Protection: The general rule in all states is that creditors cannot take the assets of an LLC to pay off personal debts or liabilities of the LLC’s owners. In other words, if you (IRA owner) owns 100% of an LLC, a creditor of the LLC cannot go after your IRA assets outside of the LLC. This is one of the benefits of using an LLC that your IRA completely owns.

- Dedicated LLC: Investors will need to establish an LLC specifically for the IRA and transfer their retirement funds into the LLC.

What is a Self-Directed IRA LLC?

A self-directed IRA LLC is a retirement platform that combines the tax benefits of an IRA with checkbook control over your investment decisions. The IRS sets the guidelines on what you can invest in, but within those boundaries, the possibilities are vast for an IRA account holder.

What’s the difference between a Self-Directed IRA vs. Self-Directed IRA LLC?

Unlike traditional IRAs, which are typically limited to stocks, bonds, and mutual funds, self-directed IRAs allow you to invest in a much broader range of assets, including real estate, private equity, precious metals, cryptocurrency, and more.

The downside of a traditional self-directed IRAs is that in order to make any investment, it has to go through your custodian’s compliance process. This can result in transaction fees charged by the custodian, as well as significant delays in completing the investment process.

But a self-directed IRA LLC (also called a Checkbook IRA or a Self-Directed IRA with Checkbook Control) solves this issue. Here, the IRA owns a special-purpose LLC and the account holder serves as the manager of the LLC, gaining the power to personally direct investment activities.

This is important for a couple reasons. At Equifund, many of our members want to invest in our listings using their SDIRA. However, many firms who offer SDIRAs are not very familiar with Regulation Crowdfunding and Regulation A+ securities.

In general, they have compliance processes that are not reasonable with the legal requirements funding portals have regarding online offerings. In many cases, we have had to reject investments from members because their SDIRA custodian was non-cooperative during the transaction process.

In other cases, the custodian has actually denied the member the ability to invest in an offering they would be legally allowed to because of SDIRA internal compliance policies (especially around cannabis and crypto oriented companies).

With a checkbook IRA, you would have complete control over what you invest in, as long as it is not a prohibited transaction (e.g. life insurance contracts and collectibles). We’ll dive deeper into prohibited transactions later on in the article.

Additionally, one of the challenges with custodian controlled SDIRAs is that many are not structured to hold publicly traded securities – only private ones. This means if part of your investment strategy is investing in companies that may IPO one day, this could create additional – and costly – administrative burdens and delays.

Benefits of Investing Through a Self Directed IRA LLC

A self-directed IRA can be an attractive option for an IRA holder who wants the following benefits:

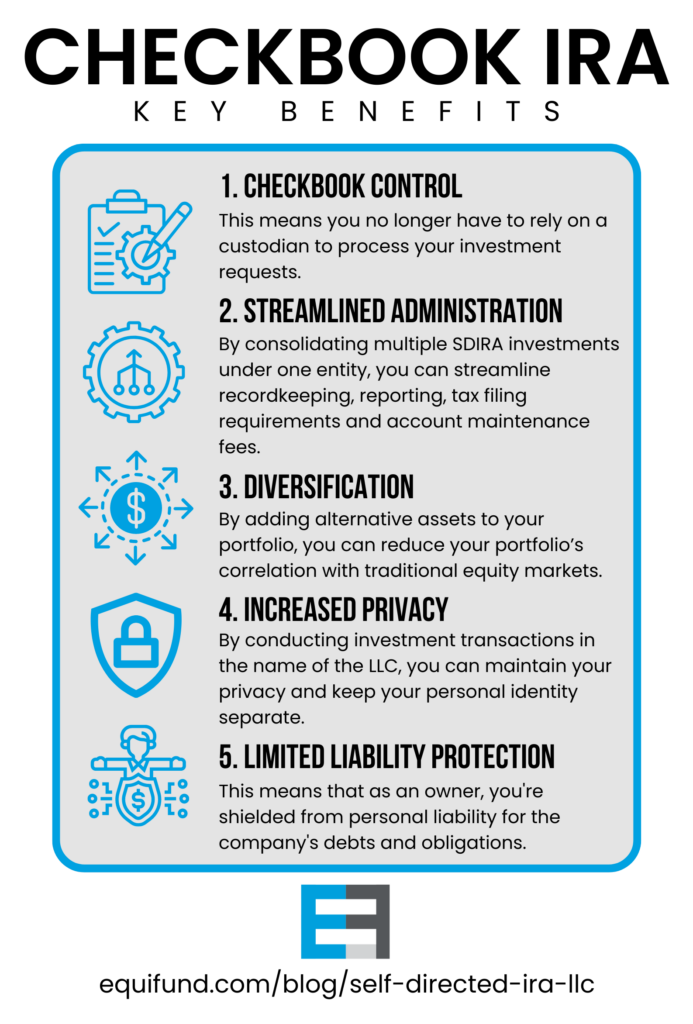

Checkbook Control

This means you no longer have to rely on a custodian to process your investment requests.

Streamlined Administration

By consolidating multiple SDIRA investments under one entity, you can streamline recordkeeping, reporting, tax filing requirements and account maintenance fees.

Diversification

By adding alternative assets to your portfolio, you can reduce your portfolio’s correlation with traditional equity markets.

Increased Privacy

By conducting investment transactions in the name of the LLC, you can maintain your privacy and keep your personal identity separate.

Limited Liability Protection

This means that as an owner, you’re shielded from personal liability for the company’s debts and obligations.-

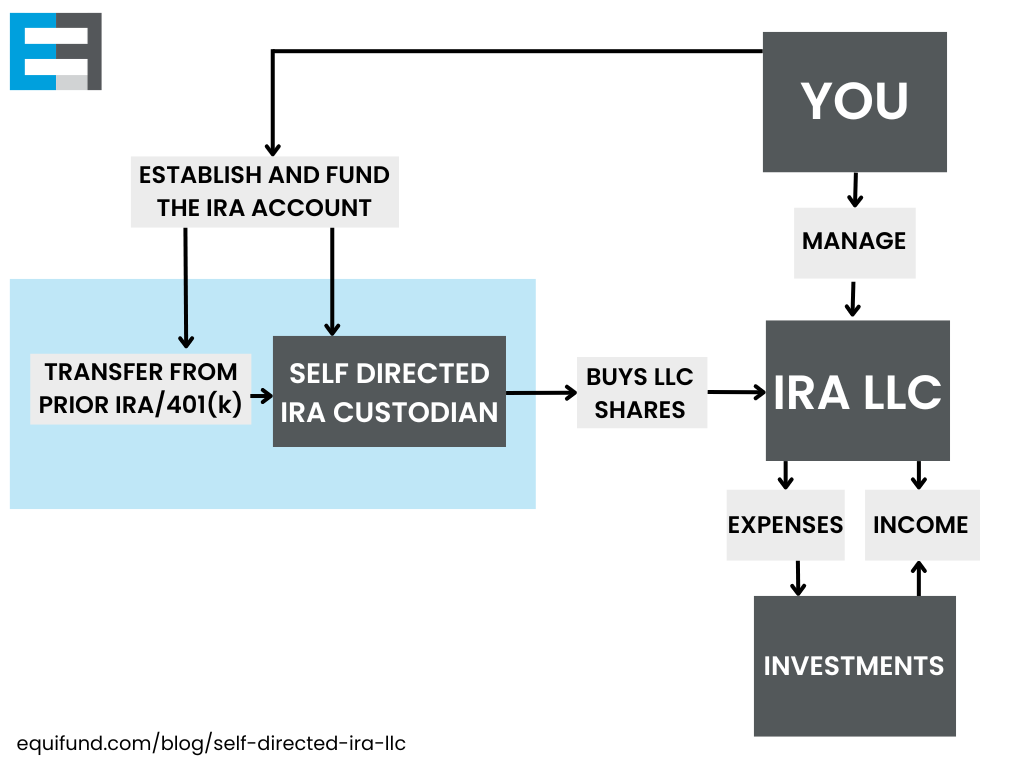

How does a Self-Directed IRA LLC Work?

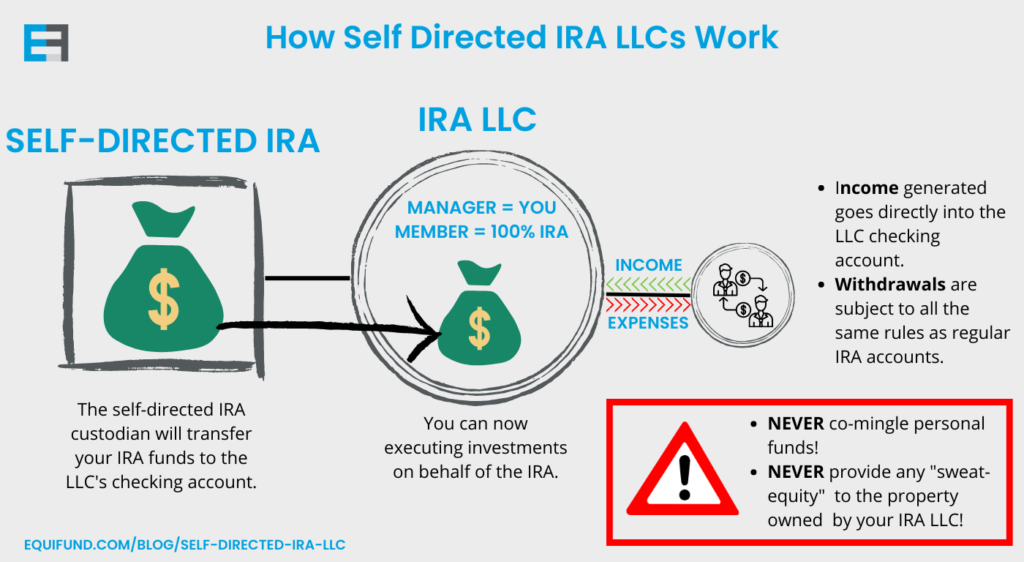

A self-directed IRA LLC involves two layers:

- An IRA account held by a trusted custodian that handles compliance and reporting requirements.

- A specially crafted Limited Liability Company (LLC) wholly owned entirely by the IRA.

The IRA’s cash is invested into the LLC, ensuring tax advantages. As the manager of the LLC, the investor has signing authority and full control over the IRA-owned LLC’s capital:

- You are responsible for executing investments on behalf of the IRA.

- Initiating investments or paying expenses is as simple as writing a check or sending an ACH/wire.

- Any income or capital gains generated from investments goes directly into the LLC checking account.

- Withdrawals are subject to all the same rules and regulations as regular IRA/401k accounts.

Can I Roll Over my Retirement Account into a Self Directed IRA LLC?

Yes, you can rollover current IRA accounts into a SDIRA LLC, as long as they are eligible for rollover. This includes most IRAs, former employer’s 401(k) plans, and even inherited IRAs.

Rolling over money from a qualified retirement account into a non-qualified retirement account does carry risk, however. This includes immediate taxation and potential penalties on the transferred funds, the loss of legal protections from creditors and bankruptcy, the forfeiture of future tax-deferred growth, and changes in rules about required minimum distributions.

However, keep in mind that a current employer retirement plan may not be eligible for rollover. Please check with your plan provider for clarification on what you may or may not be eligible to do.

What are Self-Directed IRA LLC prohibited transactions?

It’s vital to adhere to IRS rules, as engaging in prohibited transactions can lead to penalty taxes and the loss of the IRA’s tax-deferred status.

According to IRC Section 408(a)(3) and IRC Section 408(m), life insurance contracts and collectibles like art and jewelry are excluded from investment possibilities. And under IRC Section 4975, all disqualified persons, including fiduciaries, family members, business partners, and major shareholders, are prohibited from engaging in transactions with your Self-Directed IRA LLC.

Examples of prohibited transactions include:

- Selling or leasing investment property to disqualified persons

- Lending money or extending credit

- Benefiting from IRA assets personally

One simple way to keep a layer of separation between your SDIRA and disqualified persons buying private real estate through Reg-CF or Reg-A+ offerings on platforms like Equifund.

Do I need to file a tax return for my Checkbook IRA?

The IRS treats checkbook IRAs as a “disregarded entity,” so there’s no need for an additional tax filing. However, the IRA is subject to filing a tax return (Form 990T) in the event that UBTI or UDFI taxes are generated. In addition, your custodian will likely ask you to file a report stating the fair market value (FMV) of assets held in your self-directed account at the end of each year.

Lastly, keep in mind that you’ll still have to pay annual filing fees for the LLC that houses your checkbook IRA, and the fees will vary depending on the state where you formed the LLC.

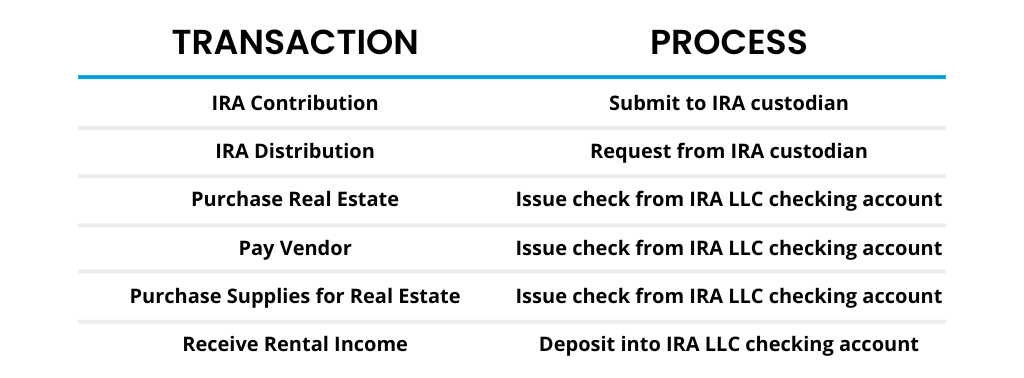

IRA LLC Contributions and Distributions

According to IRS guidelines, all IRA contributions and distributions must be reported, meaning these transactions must go through your IRA custodian.

So, when making contributions to your IRA, you’ll need to deposit the money into your self-directed IRA account, rather than your IRA LLC. Similarly, when taking distributions from your IRA, it should be done from your IRA account and not your IRA LLC.

In the latter case, the custodian would handle the necessary paperwork and process the distribution according to the IRS rules. It’s important to note that any distributions from your IRA may be subject to taxes and penalties if you’re not of eligible retirement age or if they fall under certain distribution categories.

How to Open a Self-Directed IRA LLC

Let’s walk through the process of opening a self-directed IRA LLC step by step:

Step 1. Reach out to an IRA LLC facilitator

Start by connecting with an IRA LLC facilitator like Check Book IRA or IRA Financial.

Step 2. Open a Self-Directed IRA with a Custodian

The facilitator will guide you in opening a self-directed IRA with a self-directed IRA custodian. This custodian will act as the financial institution that holds and administers your self-directed IRA funds.

Step 3. Customize your LLC for IRA investments

Working with the facilitator, you’ll create a customized limited liability company (LLC) specifically designed for your IRA investments. This LLC will serve as a vehicle through which your self-directed IRA can make investments.

Step 4. Register your LLC and establish a business checking account

Once you’ve decided on a name, register your LLC with the state according to its requirements. Each state may have specific rules, such as filing articles of organization and paying establishment or annual fees. Additionally, you’ll need to open a business checking account for the IRA LLC at a local bank.

Step 5. Transfer funds from the IRA custodian to the LLC

The self-directed IRA custodian will transfer your IRA funds to the LLC’s checking account.

Step 6. Conduct transactions through the LLC checking account

With the funds in the IRA LLC checking account, you can now make investments, write checks, and receive deposits related to your IRA investments. For instance, you could purchase rental property or make other eligible investments, all managed through the LLC’s checking account.

How much does it cost to set up and manage a Self-directed IRA LLC?

While the setup fee may vary depending on the custodian or provider, it typically ranges from $50 to $300.

Investors should also be aware of “hidden” fees like:

- Annual fees, which can be based on the asset type or its value.

- Transaction fees for buying, selling and transferring funds.

- Administrative costs associated with alternative assets

To calculate all of this for yourself, you can download this Self-Directed IRA Fee Comparison Template.

How to invest with a Self-Directed IRA LLC

By leveraging a self-directed IRA LLC, you can follow in the footsteps of investors like Peter Thiel and access private market investment opportunities that may yield substantial long-term returns.

The added advantage of this investment strategy is that alternative assets often require a longer hold period, which may align perfectly with retirement savings meant to grow untouched until you’re ready to enjoy them.

One of the major challenges when it comes to making private market investments is sourcing great deals. To that end, you can browse the private market offerings provided on Equifund Crowdfunding Portal, which undergo a rigorous 8-12 weeks of due diligence before listing.

To invest in private equity and private real estate offerings with your SDIRA, you c Comment start an set up your checkbook IRA LLC on Equifund. Once Comment end your individual account is set up, you can add a corporate account to your profile and you’re off to the races.