While the mainstream financial media is talking about Rupert Murdoch retiring from Fox in what may or may not be the plot line from hit TV show Succession, the Fed raising rates (again), and “Oil $100+” on the horizon…

In today’s Weekend Edition, we’re doing a follow-up to our weekday edition about uplistings.

The most famous example of a stock that had a tremendous performance post-uplisting is none other than the energy drink company, Monster Beverage.

- Monster Beverage (Nasdaq: MNST) – Formerly known as Hansen Natural, the company went public in 1990.

The company announced its shares would trade on the Nasdaq Global Select on July 5th, 2007. Since then, the stock has climbed ~1,400% (vs the S&P Total Return’s 293%).

It is now one of the largest beverage companies with over $6 billion in annual revenue.

But aside from this very extraordinary example, how do stocks fare after they go through the uplisting process?

That’s what we’re talking about today.

Let’s dive in,

-Equifund Publishing

Scoreboard: How Stocks Perform Post-Uplisting

Let’s kick this off with the core hypothesis of uplisting – does it actually improve trading volume, reduce bid-ask spreads, and otherwise generate positive shareholder value?

According to a study published in the April 2021 issue of The Financial Review:

Previous empirical studies of OTC securities suggest that retail investors display greater levels of divergence of opinion, which is magnified in firms that are opaque and difficult to short.

To the extent that exchange listing broadens the firm’s investor pool and reduces the proportion of retail traders, OTC firms may experience a decrease in volatility and an increase in price discovery after listing on a national exchange.

Both our univariate and multivariate difference-in-differences tests indicate that treatment firms vis-à-vis control firms experience a dramatic improvement in stock liquidity after listing to a major exchange.

For the average treatment firm, relative to the average control firm, dollar volume increases by 80.21%, bid–ask spreads fall by 143 basis points (bps), and price impacts decrease by roughly 36% after listing, other factors held constant.

Our results indicate that both the least-liquid and the most-volatile OTC treatment firms, relative to control firms, experience the greatest liquidity gains from exchange listing.

To be fair, the study only tracks the 190 “treatment” stocks over a 120-day event window surrounding the uplisting date, and makes no mention of long-term impact on volume or pricing (more on this in just a moment)…

But what I find most interesting about this study is the reason the authors believe cause these positive results – institutional ownership.

More specifically, stocks with greater institutional holdings tend to be priced more efficiently.

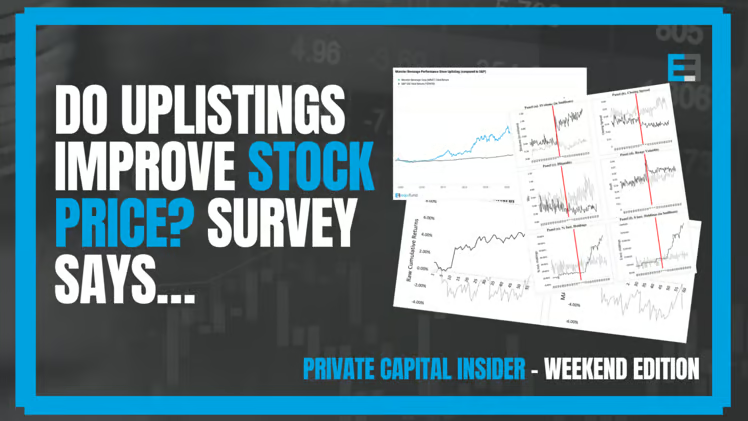

The chart below plots average liquidity and institutional ownership measures for the 190 treatment stocks (solid line) that uplisted to national exchanges during the sample period, and for the 190 matched control firms (dotted line) in the 120-day event windows surrounding the events (60 days before uplist and 60 days after).

For reference, I’ve added a vertical red line to show the date of uplisting to make it easier to read.

According to the study,

In Panel a … we analyze changes in dollar volume around exchange listings. We show that average dollar volume for treatment stocks increases abruptly at exchange listing and remains elevated in the subsequent 60 days.

In Panels b and c … we examine both trading costs and price impact around exchange listings. Our graphics show that average closing spreads for treatment stocks begin to decrease around the exchange listing dates and remain lower in the following 60 days.

In Panel d, we examine the effect of exchange listing on volatility. Interestingly, we find a substantial increase in average volatility for treatment stocks in the few days around exchange listing, which then drops off substantially before stabilizing at a level still above prelisting averages.

In Panels e and f … we examine whether institutional holdings change around exchange listings. We show that institutional investors increase their holdings of treatment stocks substantially in the postlisting period.

However, it appears that the increase in % Inst. Holdings starts about 10 trading days after exchange listing.

This is important because it means that the uplisting effect is more a function of market structure changes and not simply a reflection of institutional investors pushing OTC firms to list for liquidity gains.

In fact, the opposite appears true, that the liquidity gains from uplisting attract institutional traders.

Now, let’s take a look at the actual stock performance following the listing.

According to the data, the treatment firms had superior raw AND market-adjusted returns, compared to the control.

Interestingly enough, the 10-day delay aligns perfectly with the ~10-day delay noted earlier regarding percentage increase in institutional participation.

Based on this, the authors conclude that the results seemed to indicate that the stock price increase associated with exchange listing from the modern OTC markets is driven almost entirely by an increase in institutional trading.

Unfortunately, the authors don’t provide this data in their study.

For this reason, we’ll turn to a series of articles published by Sergio Heiber on Seeking Alpha, who put together his own study on the effect uplisting has on stock prices.

The various studies used stocks that were uplisted from OTC to a senior exchange in 2015 – 2018.

According to Heiber, for the 2017 and 2018 sample:

- ~68% of uplisted stocks enjoyed a stock price appreciation in the six months leading to uplisting

- The average six-month gain for the entire group was 26%.

- Almost four out of every five uplisted stocks for this two year period went on to higher 52 week highs with the entire group averaging a 48% gain.

- The magic is temporary thought, as within a year the majority of stocks have lower prices than their uplist price.

- The entire group is trading on average 16% lower than their uplist price.

- Biotechs are the most volatile sector while Material stocks are the least explosive.

- The majority of stocks tend to run up within the six months leading to uplisting and continue to run to new highs afterwards before selling off.

Unfortunately, Heiber doesn’t include any data or discussion around institutional ownership for the sample group, nor does he provide any conclusions regarding the cause of the short-term pump, and long-term slump…

However, he does caution that many companies claim they are seeking an uplisting, but never complete one… as well as the obvious “hey, it could be a pump and dump” warning as well.

What can we learn from these two studies?

A stock that goes through a successful uplist could have extraordinary upside potential if it can continue to drive corporate milestones (like Monster Beverage has), and attract institutional investors.

But that doesn’t mean it’s a “sure thing” to bet on stocks that are looking to uplist.