The 5-Step Guide to Investment Due Diligence for Retail Investors

Investment due diligence is the process of analyzing investment opportunities to understand the risks and rewards. It involves examining corporate records, financial records, personnel matters, intellectual property matters, and legal matters.

Uplisting Stock Strategy – How to Go From OTC to Major Exchange

Uplisting (sometimes referred to as a second IPO)is when a stock transitions from a junior exchange like the OTC markets to a major one, such as Nasdaq or NYSE.

The PIPE Investment Guide: How to Buy Once & Profit Twice

Private Investment in Public Equity (PIPE) is a financing strategy that allows investors to buy stocks from a publicly traded company at a fixed, often discounted, price.

22 Small Business Tax Write Offs to Maximize Your Return in 2023

Top 22 small business tax write offs: 1. Home Office Deductions, 2. Business Supplies and Equipment Write Offs, 3. Professional Services Deductions, 4. Vehicle Expenses and Mileage Deductions, 5. Business Meal Deductions…

Pytheas – How to Execute Subscription Agreements

https://equifund.com/content/uploads/2024/04/How-To-Execute-Sub-Agreements-Pytheas.mp4

📈Gold heats up as Feds pause rate hikes

On June 14th, the Federal Reserve’s monetary policy committee said Wednesday it would pause its historic rate-hiking campaign, as it waits for the effects to trickle further through the economy.

The Insiders Guide to Tax Reduction Strategies

How to build generational wealth faster by paying fewer taxes.

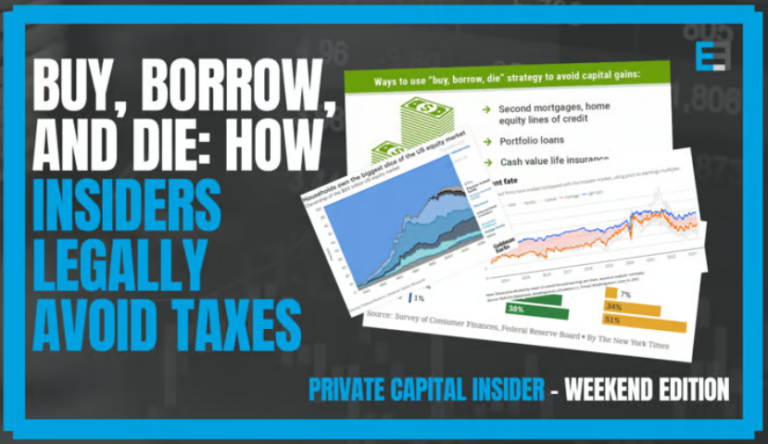

📈Buy, Borrow, and Die: How Insiders legally avoid taxes

Looks like many of our readers enjoyed our most recent issue of Private Capital Insider – ”Unlocking the Generational Code.” If you enjoyed that issue, today,

The 5-Step Guide to Investment Due Diligence for Retail Investors

Investment due diligence is the process of analyzing investment opportunities to understand the risks and rewards. It involves examining corporate records, financial records, personnel matters, intellectual property matters, and legal matters.

Uplisting Stock Strategy – How to Go From OTC to Major Exchange

Uplisting (sometimes referred to as a second IPO)is when a stock transitions from a junior exchange like the OTC markets to a major one, such as Nasdaq or NYSE.

The PIPE Investment Guide: How to Buy Once & Profit Twice

Private Investment in Public Equity (PIPE) is a financing strategy that allows investors to buy stocks from a publicly traded company at a fixed, often discounted, price.