If you’ve ever wondered to yourself, “what happens to my Pre-IPO investments if I die (or get divorced)?”…

Here’s the short answer:

- With proper planning, your assets will be passed on to the people you want them to go to, and to be used in the way you specify.

But if you don’t?

There’s a good chance the tax man winds up with more of it than you’d like him to…

Your loved ones wind up fighting over your assets (while racking up a massive legal bill for their troubles)…

And the gift you thought would help your family winds up being a point of divisiveness.

That’s why today, we’ll be talking about one of the simplest forms of estate planning…

And the #1 thing you want your family to avoid.

The Evils of Probate

Before we go any further…

DISCLAIMER: I am not a lawyer and don’t play one on TV. Please do not take anything you’re about to read as legal advice. It is for informational purposes only and should be considered a starting point.

When it comes to estate planning, the starting point of all conversations you have with your advisor is something called Probate.

Probate is a legal process that takes place after someone dies. It includes:

- Proving in court that a deceased person’s will is valid (usually a routine matter)

- Identifying and inventorying the deceased person’s property

- Having the property appraised

- Paying debts and taxes, and

- Distributing the remaining property as the will (or state law, if there’s no will) directs.

Generally speaking, probate sucks and should be avoided because…

1) It can be expensive.

All legal fees must be paid before any of your heirs get what you’ve left them.

To make things worse, if you own property in other states, your family could face multiple probates, each one according to the laws in that state.

OUCH!

2) It takes time.

The American Bar Association (ABA) estimates the timetable at six to nine months for the average estate… but it can also go longer, especially if there is a contested estate.

During part of this time, assets are usually frozen so an accurate inventory can be taken.

Nothing can be distributed or sold without court and/or executor approval.

This means if your family needs money to live on, they must request a living allowance, which may be denied.

3) Your family has no privacy.

Probate is a public process.

This means the court is required to post notice so any “interested party” can see what you owned, whom you owed, who will receive your assets and when they will receive them.

This is a great way to tell creditors, angry exes, and entitled relatives they can now make claim to what rightfully belongs to your family.

4) Your family has no control.

Have you ever gone to the doctor and had no idea what it’s going to cost or how long it will take? Probate is like that, but worse.

You family will have no idea how much it will cost, how long it will take, and what information is made public.

This is why wealthy people do everything they can to avoid having their property go through probate.

They want to make sure their loved ones – or the charitable causes they care about – get everything they’re supposed to… WITHOUT having to deal with some drawn out legal process.

Broadly speaking, there are two main ways wealthy people accomplish this goal.

Wills and Trusts

You probably know you should have a will… but you might not know exactly what it can do and what it can’t do.

A will is a document that states your final wishes.

It is read by a county court after your death, and the court makes sure that your final wishes are carried out.

Most people use a will to leave instructions about what happens with their property after they die. But it can also be used to…

- Name guardians for children and their property

- Decide how debts and taxes will be paid

- Provide for pets

Contrary to what you’ve probably heard, a will may not be the best estate planning tool for you and your family.

The main reason is – of course – probate. A will does not avoid probate when you die.

In fact, for a will to be valid, it has to go through probate before it can be legally enforced.

Also, because you have to die in order for your will to go into effect… it provides no protection if you become physically or mentally incapacitated.

This means the court could potentially take control of your assets before you die if you don’t have proper directives in place.

Fortunately, there is a simple and proven method common in estate planning: a living trust.

A living trust is a legal document that – just like a will – contains your instructions for what you want to happen to your property when you die.

But here’s the important difference…

When you set up a living trust, you transfer assets from your name to the name of your trust, which you control — such as from “Joe and Jackie Smith, husband and wife” to “Joe and Jackie Smith, trustees under trust dated (month/day/year).”

Legally you no longer own anything. Instead, your trust does.

This means when you die, there’s nothing you “own” that needs to go through probate.

The concept is simple, but this is what keeps you and your family out of the courts.

It may also solve a lot of the problems a will does not.

For example…

- Saving money: The fewer assets that need to go through probate means fewer potential legal fees.

- Control of your wealth: You get to decide exactly when, and to whom, your assets go to… even when there are complex situations such as children from more than one marriage.

- Protecting your legacy: A properly constructed trust can help protect your estate from your heirs’ creditors or from beneficiaries who may not be adept at money management.

- More privacy: Probate is a matter of public record. A trust helps your assets to avoid probate and pass to your heirs privately.

Not only does it avoid probate, this structure can give you far more control over your assets, both while you’re living and upon your death.

For example, you can:

- Put conditions on your gifts. (i.e. I give my house to my daughter if she finishes college)

- Leave instructions for final arrangements (i.e. I want these funds to be used to commission a 10 foot tall statue of me riding a horse).

- Leave property for your pet.

- Make arrangements for money or property that will be left another way. (i.e. Property in a trust or property for which you’ve named a pay-on-death beneficiary.)

Now, there’s a LOT of different trusts you can set up, and each has its own special features, benefits, and drawbacks…

And you should definitely talk to an estate planning attorney about your specific needs.

However, if you don’t have a trust (or other estate planning vehicle) set up, you have a simple alternative that can help provide a basic layer of protection for your Pre-IPO investments.

How to Add Beneficiaries to your Pre-IPO Investments

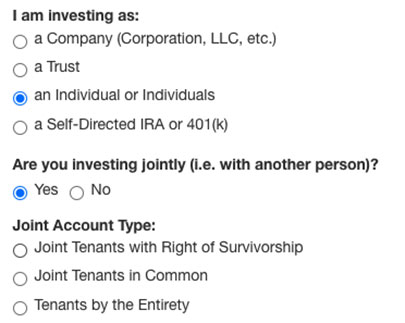

If you’ve made an investment on the Equifund Crowd Funding Portal, you’re already familiar with completing the “Subscription Agreement” using the online investment wizard.

If you’ve invested as an individual during that process, you may have seen an option that says “Are you investing jointly (i.e. with another person)?”

If you are investing as an individual, you can chose to invest jointly with another person.

There are three types of joint account types you can choose when completing your subscription agreement.

- Joint Tenants with Right of Survivorship (JTWROS): This refers to a legal ownership structure involving two or more parties for any type of financial account or another asset.

Each tenant has an equal right to the account’s assets and is afforded survivorship rights if one of the account holder(s) dies.

A surviving member inherits the total value of the other member’s share of property upon the death of that other member.

- Joint Tenants in Common (JTIC): This refers to a legal relationship in which two or more people own a piece of property or another asset where no rights of survivorship are afforded to any of the account holders.

Unlike other common legal relationships, when one owner dies, the surviving owner(s) does not automatically inherit their portion of the asset.

Each tenant in the account can stipulate how their assets are to be distributed upon their death in a written will.

A deceased owner’s portion of the asset can only be transferred to the surviving tenants if it is noted in the individual’s will.

- Tenants by the Entirety (TBE): This refers to is a method in some states by which married couples can hold the title to a property.

Property that is held in TBE is comparable to community property. Both spouses mutually own the entire property as a whole rather than any type of subdivision, where each would have individual ownership.

Final Thoughts

If you’re not excited about pondering your eventual death – and what happens to your assets after – welcome to the club.

But if you’re in the position of “head of household” or “steward of family wealth,” you owe it to the people (and causes) you care about to have a plan in place.

If you’re in a situation where you’ve already made an investment and you’d like to add a beneficiary, you will need to contact the transfer agent for each investment you have.

However, because investment products are regulated, there are certain safeguards and protections in place designed to reduce or eliminate fraud when it comes to changing ownership.

To help you navigate this process, we put together this free guide called How to Retitle Your Pre-IPO Shares.

As always, please consider talking to a qualified estate planning attorney to help you with your own individual needs.

Sincerely,

Jake Hoffberg – Publisher

Equifund