If you’ve ever wondered why you have to provide sensitive information – like your social security number – when investing…

Or you’ve ever felt frustrated having to upload additional documentation – like a driver’s license and proof of address – to prove your identity…

We’ve got some good news.

First… the reason we do this has to do with America’s attempt to combat money laundering, identity theft, and financial fraud.

Second… we’ve completely overhauled our membership website to make identify verification faster and easier for our members to complete.

In just a moment, we’ll give you a full walkthrough on exactly how to update your profile and submit identity verification documents…

But first, let’s take a look at…

A Brief History of Money Laundering & Banking Regulation in America

Money laundering is the process of introducing illegally obtained money back into the economy.

The goal is to exchange the illegally acquired money (dirty money) for legally acquired money (clean money), and therefore, avoid suspicion from law enforcement.

Money laundering is also a key ingredient in terrorist financing. However, it wasn’t until relatively recently that American policy paid much attention to it.

Prior to the 1970s, money laundering was barely considered a crime.

At the time, tax evasion was the more serious offense; In the 1931, Al Capone – who had reportedly boasted, “They can’t collect legal taxes from illegal money” – was sentenced to 11 years in prison for failing to file tax returns.

That all changed when the US Congress passed the Bank Secrecy Act (BSA) in 1970, as a response to the trend of criminals in the US using ‘secret foreign bank accounts’ to perpetrate money laundering and other illegal activities.

The BSA also introduced several reporting requirements:

- Currency transaction reports (CTR): for cash transactions exceeding $10,000 in a single day.

- Suspicious activity reports (SAR): For activity deemed suspicious according to a set of criteria, such as an unusually high volume of transactions or transactions with high-risk countries.

- Foreign bank account reports (FBAR): For US citizens that hold foreign financial accounts with $10,000 of value or more.

- Currency and Monetary Instrument Report (CMIR): For cash purchases of instruments (i.e. money orders or cashier’s checks) that exceed $10,000

The law faced several constitutional questions and challenges, eventually reaching the Supreme Court in 1973 in The California Bankers Association v Schulz, and again in 1976 with The United States vs Miller.

In both cases, the Supreme Court ruled in favor of the US Government.

Then, thanks to the Reagan administration’s “War on Drugs,” money laundering become a more serious policy issue.

In an effort to combat the sale of illicit drugs, money laundering was made a federal crime for the first time ever thanks to the US Money Laundering Control Act of 1986 (MLCA).

Section 1956 of MLCA prohibits individuals from engaging in a financial transaction with proceeds that were generated from certain specific crimes, known as “specified unlawful activities” (SUAs).

The MCLA also sets forth fines and penalties for anyone who knowingly:

- Engages in a financial transaction in criminally derived property;

- Engages in a commercial transaction which is part of a scheme to conceal criminally derived property, or to disguise the source or ownership of criminally derived property; or

- Transports or attempts to transport a monetary instrument or funds from a place in the United States to or through a place outside the United States, or vice versa, as part of a scheme to conceal criminally derived property, or to disguise the source or ownership of criminally derived property.

Then, 9/11 happened and the government decided more serious steps were required to detect and prevent terrorist financing through money laundering.

On Oct 26, 2001, the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act (The USA PATRIOT Act) was signed into law by President George W. Bush.

The Patriot Act had a variety of consequences across many segments of public and private life in America.

In the banking sector, it strengthened and expanded the reporting and record-keeping mandate of the BSA. It also required firms to implement anti-money laundering (AML) programs, with appropriate internal AML policies, controls, and procedures.

In enhancing the BSA’s record-keeping requirements, the Patriot Act emphasized the need for firms to verify the identity of the customers with which they were doing business (known as “Know Your Customer” or KYC).

KYC refers to the process implemented by a financial institution or business to:

- Establish verified customer identity.

- Understand the exact nature of the customer’s activities. This is to confirm that the source of associated funds is legitimate.

- Assess money laundering risks.

Together, these AML and KYC requirements became known as the Customer Identification Program (CIP).

According to the CIP rules and policy, financial institutions including banks must verify the identity of individuals who wish to use their services to conduct financial transactions.

The minimum requirements for opening a financial account in the US are:

- Name of the customer

- Address of the customer

- Date of birth

- Tax Identification Number (TIN) / Social Security Number (SSN)

The documents verified for the purposes of KYC may include social security card, passport, driver’s license, and credit/debit cards.

Here’s what information we need from you in order to comply with KYC/AML regulations

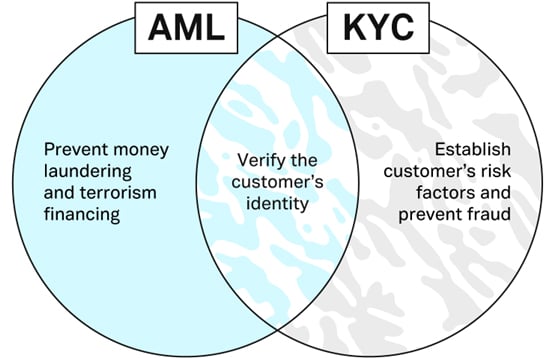

AML procedures primarily focus on being reactive to suspicious activity, KYC rules attempt to be more proactive in preventing bad actors from using the financial system in the first place.

Image source: Plaid.com

While Equifund is not a banking institution, we follow all AML/KYC regulations as part of our compliance protocols.

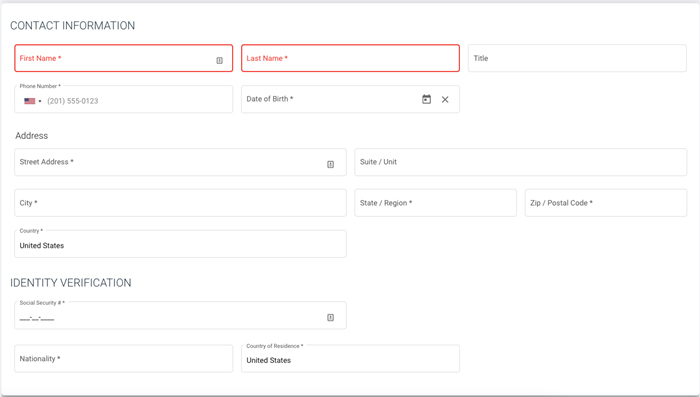

In order to verify your identity, we have to collect what’s called Personal Identification Information (PII); this includes your name, address, date of birth, nationality, and tax identification number (i.e. your social security number if investing as an individual).

If you haven’t logged into the new membership website, you’ll need to reset your password (go here to do that).

Inside your “My Account” page, you will see a list of PII we are required to collect as part of our CIP. You will need to enter all of this information before you can invest in any opportunities listed on Equifund.

Please note that any extremely sensitive information required for KYC is encrypted in our database.

This information is then checked against a database of “watchlists” and “blacklists.” If the information you provided does not match information in these databases, our AML/KYC provider will “clear” your identity and your transaction can be accepted.

In some cases, our AML/KYC provider will ask for additional documentation in order to verify your identity. This may include things like:

- A valid government issued identification (i.e. driver’s license, passport).

- Proof of address (i.e. utility bill, bank statement)

To upload these documents, you can do so in the Document Upload tab in your My Account section. My Documents section of the member dashboard.

If your account is set up as an “Individual” account, you will be asked for two documents:

- A valid government-issued identification: state-issued identification card, driver’s license, or federally-issued passport are accepted. Military IDs are not accepted. All photos must be in color, with all four corners of the identification visible.

- Proof of address (in English): Must be a utility bill, bank statement, or letter from a government agency. Compliance requires these documents to be in English, dated within the last 90 days.

If you are investing as a Corporation, Trust, or IRA, in addition to providing documentation for all parties investing (called “Associated Persons”), you will always need to provide additional documentation verifying ownership of the entity.

For Corporations (i.e. LLC, S-Corp, C-Corp), you will need to provide:

We also have to follow “Know Your Business” (KYB) laws and verify who owns the corporate entity.

If you are investing through a corporation/LLC/partnership, the following documents are needed before we can process your investment:

- Articles of Incorporation / Corporate Bylaws: This is a set of formal documents filed with a government body – typically the Secretary of State – to legally document the creation of a corporation.

- Proof of Company Address (in English): Must be a utility bill, bank statement, or letter from a government agency. Compliance requires these documents to be in English, dated within the last 90 days.

In some cases, you will also be asked to provide:

- Proof the company is in good standing

- EIN verification letter provided by the IRS

For Trusts, you will need to provide:

Similar to the requirements above, we also have to verify the ownership structure of Trust investments. To do this, we require the following documentation:

- Trust Agreement (or Trust Deed): This is an estate planning document that allows you to transfer ownership of your assets to a third party. The Grantor is the person who created the Trust. A Trustee is a person who acts as a custodian for the assets held within a Trust.

- Proof of address (in English): Must be a utility bill, bank statement, or letter from a government agency. Compliance requires these documents to be in English, dated within the last 90 days.

For Self-Directed IRAs (SDIRA) you will not need to provide additional information, as long as your individual KYC clears

This means if you have a custodian controlled SDIRA, you will likely not be required to submit any additional documentation.

However, if you have a checkbook IRA – which are structured as a corporation or a trust – you will need to upload the appropriate documentation.

Final Thoughts

AML and KYC has been criticized over the years for a variety of reasons; most notably, the negative impact it has for financial firms onboarding new customers.

Not only can the complexity overwhelm new customers and make it harder to get accounts opened and transactions processed…

The costs of compliance – and technology required to do AML/KYC at scale – can be a meaningful expense.

As you may know, Equifund charges a non-refundable $24 transaction fee.

Why? Because that’s about how much it costs Equifund to comply with KYC/AML, per transaction.

[Note: To clarify, Equifund does not take custody of investor money, nor do we take custody of shares. Funds are held in escrow at a quailified financial institution until the transaction has been completed.]

We understand that our flat $24 fee might be inconvenient for smaller-dollar investors to pay versus a percentage-based fee.

However, a percentage-based fee unfairly penalizes larger investors.

In the future, we hope to be able to lower these transaction costs as we grow.

In the meantime, we hope you’ll take a few minutes to update your profile with your current information…

And if needed, upload any KYC documentation we need to process your investments on Equifund.

Your early-stage experts,

![]()

Equifund.com