While everyone else is talking about the complete sideshow that is the Trump legal drama…

Here are the stories that haven’t been getting much attention:

- Japan and the United Kingdom both entered into “technical recessions” – two consecutive quarters of year-over-year GDP contraction; Also happening, Japan’s stock market (The Nikkei) is 100 points away from hitting a new all time high

- Mortgage Bankers Association CEO Bob Broeksmit is saying new rules for banks would be the ‘end of real-estate finance as we know it’

- Fed’s Barr Says Regulators Are Eyeing Commercial Real Estate Risk

- Legendary fund manager Stanley Drukenmiller’s family office – Duquesne – dumped shares of Amazon, Alphabet, and Broadcom and scooped up shares of gold miners Barrick Gold and Newmont

Let’s dive in,

-Equifund Publishing

P.S. As a reminder, we cannot provide any individualized advice or investment recommendations.

If you need help, please consult with a qualified financial professional who is licensed to provide investment advice.

Is the most predicted recession of all time finally here?

In case you needed yet another reminder that the stock market isn’t the economy, let’s take a look at what’s going on with Japan and the United Kingdom.

Both countries have officially entered into technical recessions – two consecutive quarters of year-over-year GDP contraction…

The countries’ stock markets don’t seem to have noticed.

- In the UK: The FTSE 100 hit a new all-time high of 7,906.58 on Friday, February 3rd, 2023. At the time of writing, the Index is sitting at 7,711.

- In Japan: The Nikkei 225 is ~50 points shy of its December 1989 record of 38,957.

According to the Wall Street Journal,

The growth numbers from the U.K. and Japan mirror similarly weak conditions in much of continental Europe and China.

The divergence between the U.S. and the rest of the rich world is in large part a story of surprising U.S. strength.

The U.S. grew much faster than economists had expected it would at the start of 2023, while Europe was badly hit by high energy prices from the Ukraine war and rising interest rates.

Economists forecast the growth gap will narrow somewhat over the course of the year, but remain wide.

To be sure, the declines in activity in Europe and Japan have been relatively modest and are a reflection of slow-growing economies that by nature fall into contraction more often than those that have a higher sustained level of growth.

Normally, we wouldn’t care a whole heck of a lot about what’s going on overseas…

But in the highly connected, globalized financial system – especially as we move into what appears to be a weakening global economy – this means everything is relevant.

For whatever reason, the United States – with its sixth straight quarter of growth – continues to defy recession predictions, but it’s anyone’s guess if we’re going to be able to nail the “soft landing” or not.

The soft-landing dream is over; instead, the US economy is headed for a recession in the middle of 2024, Citi says.

On the surface, the data looks great: The economy is benefiting from historically low unemployment, strong consumer spending, and robust GDP growth.

But there’s more going on with the numbers than meets the eye.

One place the economy is showing a weakness is the labor market. January had a blowout jobs report, adding 353,000 jobs to the economy.

But … if you scratch beneath the surface, the number of hours worked is falling, the number of full-time workers has decreased, and sectors such as the restaurant industry have stalled on hiring.

While the labor issue is an entirely different rabbit hole…

If history is any indication, it is usually a real estate led crisis that triggers a banking crisis, which then triggers a full-on collapse.

And for that reason, all eyes are turning to the slow motion dumpster fire that commercial real estate is becoming.

Is commercial real estate (CRE) about to collapse?

We’ve been covering this story for the past several issues now…

Basel III – and the increased reserve requirements – aren’t exactly being well received.

So, if it feels like the volume on this narrative is getting turned up across financial media outlets, it’s because it probably is.

Here’s a quick around-the-horn on headlines from the past few week.

But the cherry on top has to come from Mortgage Bankers Association CEO Bob Broeksmit,

They’re called the ‘end-game proposal,’ but only one of those words is accurate.

Basel III could be the end of bank real-estate finance as we know it.

While that might seem a bit hysterical, it’s an argument worth unpacking.

Broeksmit highlighted that approximately 50% of commercial real estate lending is managed by the banks that are under scrutiny.

If these banks are required to hold larger reserves, it means less capital can be allocated to areas in need of revitalization, in effort to support job creation.

But perhaps more worrisome, is how banks would have to handle defaulted commercial real estate loans.

According to Broeksmit,

If just one loan goes bad, regulators want to assign a 150% risk weight not only to that loan, but to all of that borrower’s loans.

It reflects the old adage that ‘one rotten apple spoils the whole barrel.’ But while that may be true in other industries, it has absolutely no bearing on ours.

The fact is that each commercial financial transaction is separate and distinct. If you have an office loan that goes bad in Manhattan, it has nothing to do with a loan on a multifamily property in Miami.

As one might expect, this increasingly alarming narrative is causing all sorts of regulatory scrutiny surrounding commercial real estate loans.

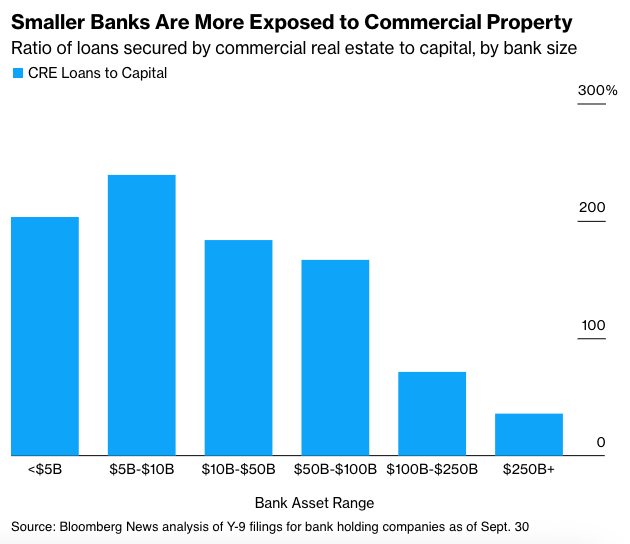

About two dozen banks in the US had portfolios of commercial real estate loans in late 2023 that federal regulators indicated would merit greater scrutiny, a sign more lenders may face pressure from authorities to bolster reserves.

The three watchdogs — the Federal Reserve, Federal Deposit Insurance Corp. and Office of the Comptroller of the Currency — indicated they would focus on banks whose portfolios of commercial real estate loans are more than triple their capital.

Within that pool, examiners would zero in on portfolios that had grown dramatically: at least 50% in the past three years.

Interestingly enough, this whole situation has the attention of former Treasury Secretary Lawrence Summers, who says it’s more important for the Federal Reserve (and other agencies) to probe for financial risks in CRE than it is to boost capital standards.

The chronic problem in banking is a failure to pay attention to the market value of assets, and that’s a particularly pronounced problem with commercial real estate, where there isn’t always a liquid market for properties.

It would be much more productive for our central bank to be focused on the question of real estate portfolios in the banks they supervise [than] some of the more abstract and politically driven arguments about various kinds of capital charges on the largest banks.

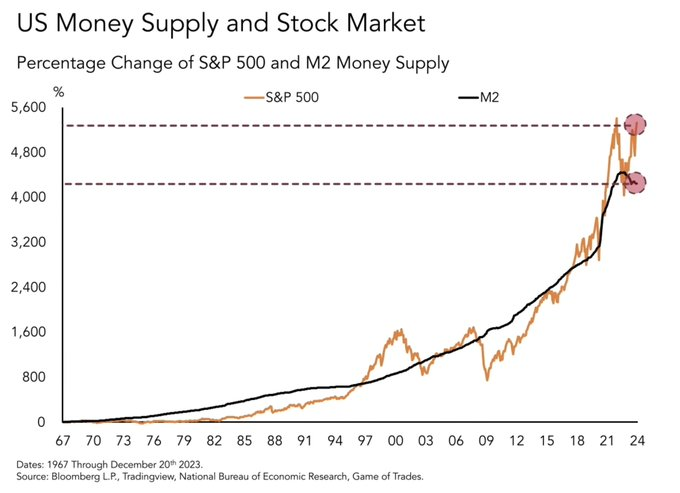

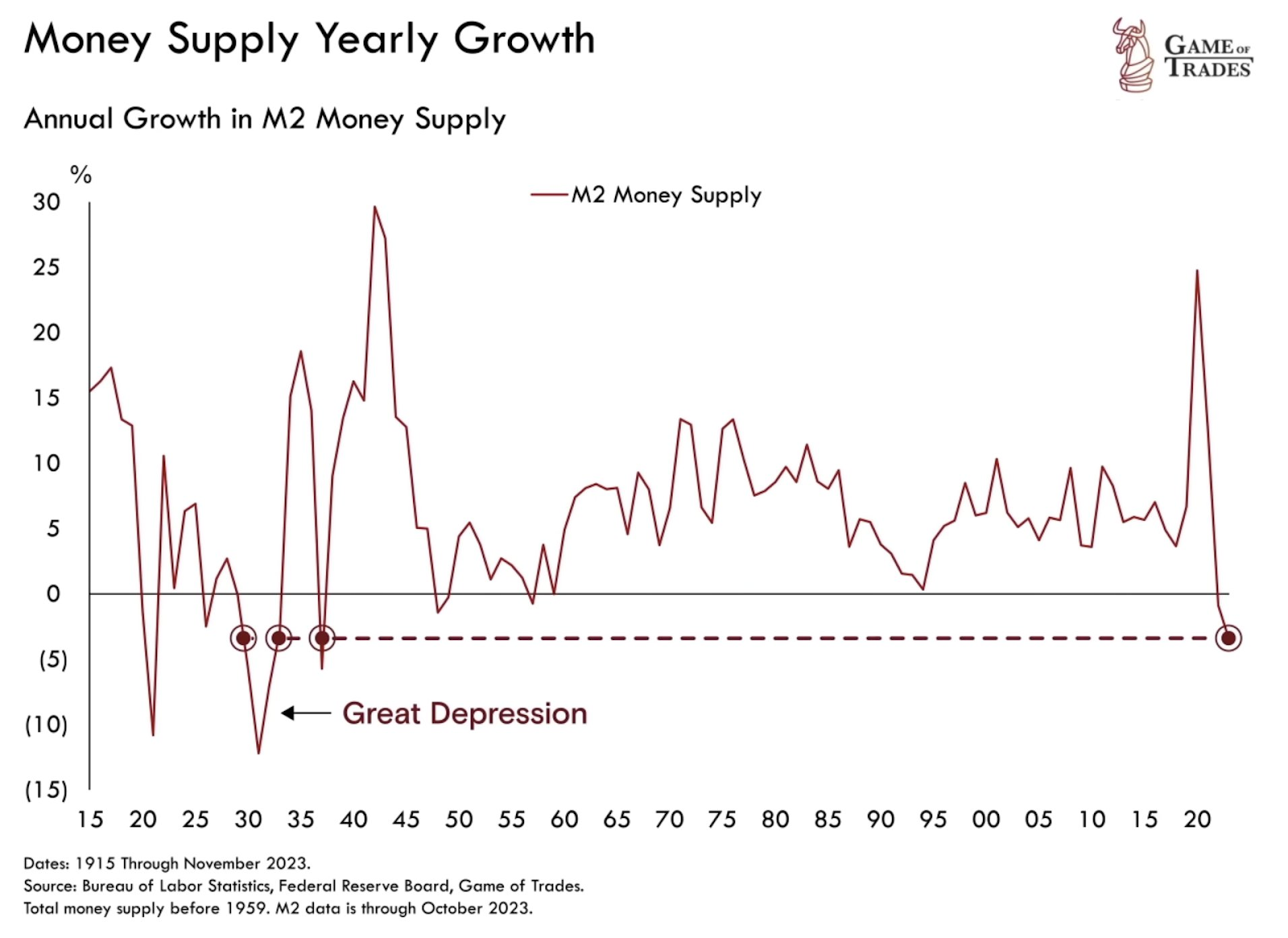

We’ve mentioned this in previous issues – generally speaking, the inevitable cause of all market crashes is a liquidity crisis. Once the money supply dries up, the default cycle begins.

If we take a look at the M2 Money Supply, we can see that the expansion of M2 has a strong correlation to growth in the stock market.

So what is happening with M2/S&P 500 right now? A very strange divergence that doesn’t make a ton of sense…

What is supporting the current stock market trends if M2 and liquidity are starting to dry up?

While we won’t make any predictions here on what will or won’t happen…

This is the reason why we are of the opinion that small balance investors should consider prioritizing downside protection and liquidity vs chasing after yield.

Sure, you might leave some money on the table by getting out too soon…

But there’s certainly something to be said about having cash on the sidelines, when you can pick up quality assets at a discount, simply because you have capital to deploy.

AI + Gold = 2024 in a nutshell?

If you had to deal with the cognitive dissonance that is the competing narratives, “the most predicted recession of all time” and “Holy Crap AI!”…

You too might come to the same conclusion that Stanley Druckenmiller just did – AI stocks + gold miners

Drukenmiller’s Duquense Family office executed significant changes to its portfolio in Q4-2023.

The move, which saw the complete divestment from 11 holdings, and a reshuffling of several others, highlights a clear focus on AI…

As well as a “barbell portfolio” style hedge, via investing in beaten down gold miners, Barrick Gold and Newmont.

One of the strangest things in the markets today is that despite gold nearing all-time highs, many gold stocks are priced at 50-80% discount to net asset values.

According to Taylor McKenna, CFA analyst at Kopernik Global Investors LLC,

Currently, you can buy gold in the ground at the largest gold producer with the longest mine lives for under $200.00 an ounce.

Even if you add lifting cost and then a margin on top of that, it’s still well below the current gold price of $2,000

In case you’re wondering why we’ve continued to cover the gold story over the past few issues, it’s not because we’re gold bugs or otherwise insinuating you should add gold (or mining stocks) to your portfolio.

More to the point, we’re definitely not making calls for “Gold $5,000” or the death of the dollar.

The reason we continue to cover it is to point out the most important question we must answer as investors – what determines the price of the stock?

Answer: the irrefutable law of supply and demand!

You can pound the table all you want that these stocks are undervalued relative to the price of gold…

Unless there is more demand (buying pressure) than supply (selling pressure), the stock price isn’t going to go higher.

Case in point – the AI Hype that added trillions of dollars of market cap to the Magnificent 7.

But what happens when that narrative runs out of steam, and investors begin to buy into the gold narrative?

Maybe… just maybe… the long awaited “gold squeeze” will finally happen, and these mining stocks could become attractive opportunities.