While everyone else is talking about Bitcoin’s dramatic upward swing, Elon Musk suing OpenAI, and more Trump drama…

Here are the stories that haven’t been getting much attention.

- Gold Futures closed at a new record high, despite ETF outflows. This week marks 15 consecutive weekly closes above $2,000, with all-time high daily and weekly closes.

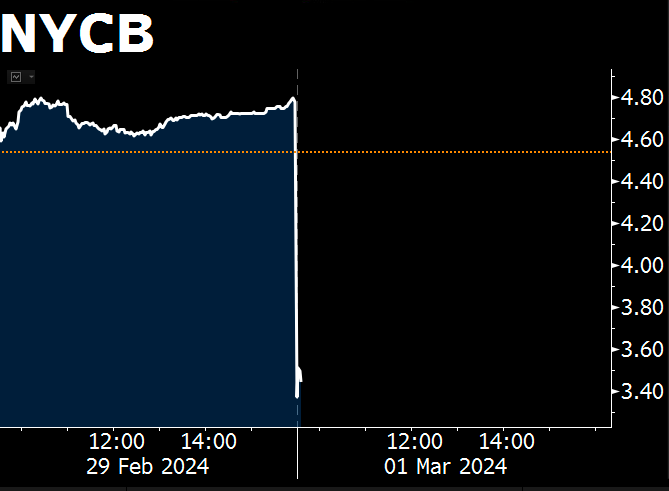

- The pending regional bank crisis continues as New York Community Bancorp stock dropped ~30% at the Friday open. They’ve also fired their CEO as losses mount to $2.7bn.

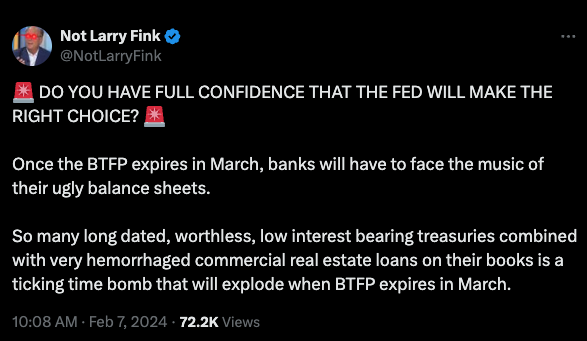

- The Federal Reserve’s Bank Term Funding Program ends March 11th, and things could get spicy.

That’s what we’re covering in today’s Weekend Edition of Private Capital Insider.

Let’s dive in,

-Equifund Publishing

P.S. As a reminder, we cannot provide any individualized advice or investment recommendations.

If you need help, please consult with a qualified financial professional who is licensed to provide investment advice.

Behold a Pale Horse: The End of The Fed’s Bank Term Funding Program

“Behold a Pale Horse” is a book written by Milton William Cooper, published in 1991.

It covers a wide range of conspiracy theories and controversial topics, including government cover-ups, secret societies, and UFOs.

The title is derived from a passage in the Bible’s Book of Revelation, which describes the Four Horsemen of the Apocalypse, with the pale horse representing death.

While we don’t like to engage in the often-foolish errand of predicting the future…

What we do like to do is build assumption-driven forecasts that describe how certain scenarios might play out.

For regular readers of the Weekend Edition, we’ve dedicated plenty of space towards the slow motion dumpster fire that continues to be the regional banking sector.

This was especially illustrated with New York Bancorp taking a swan dive on Friday, March 1st, dropping ~30% at the open.

So if you’re watching the markets and wondering “what will be the pin that finally pricks the bubble?” and triggers the consensus shift in the market (i.e., the Pale Horse)…

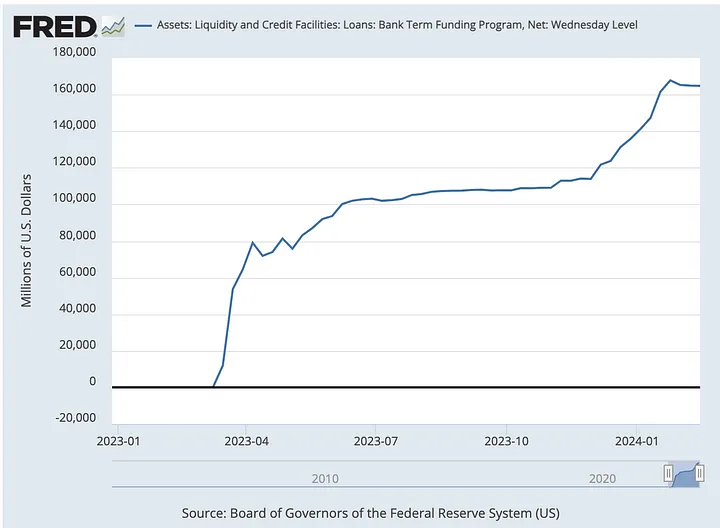

Let’s take a look at the hot topic on FinTwit these days, the Federal Reserve’s Bank Term Funding Program (BTFP) that is set to expire on March 11th, 2024.

For those who’ve never heard of the BTFP, it’s a temporary emergency measure created by the Federal Reserve in March 2023 in response to the bank runs that caused the failures of Signature Bank and Silicon Valley Bank.

This temporary program has allowed banks to take advances from the Fed for up to a year by pledging Treasurys, mortgage-backed bonds, and other debt as collateral, which is valued at par.

By allowing banks to pledge these bonds, they can meet customer withdrawals without having to sell their bonds at a loss, which is what Silicon Valley Bank did last March, sparking a run on the bank that sent tremors through the industry.

The program offers loans of up to one year in length, and to eligible depository institutions – such as banks, savings associations, credit unions, and others – that pledge collateral eligible for purchase by Federal Reserve Banks in open market operations.

Here’s why…

The traditional role of central banks is to be a lender of last resort, and the traditional means by which the U.S. Federal Reserve provides this backstop to the financial system is through what’s known as the discount window.

And yes, once upon a time, that was a literal window the bankers would use to borrow cash by pledging collateral, but received less than it’s worth (i.e., the discount).

The Federal Reserve created the discount window to help banks avoid bank runs.

However, because of this so-called “haircut” they take on borrowing, the discount window was often seen as an undesirable option…

And by extension, using the discount window attached a stigma to any financial institution using it.

The classical view of the lender-of-last-resort (LLR) role begins with the work of Henry Thornton and Walter Bagehot in the late eighteenth and nineteenth centuries.

Both authors stressed that the LLR was necessary not strictly to support individual banks, but to prevent a rapid fall in the money stock and to support the financial system as a whole during tumultuous times.

To meet these broader objectives, Bagehot offered his famous dictum that the LLR should lend freely but at a high rate (relative to the pre-crisis period) to any borrower with good collateral, where good collateral included loans to private firms and bonds.

The high rate was advisable, Bagehot reasoned, in part to limit demand from banks as well as to mitigate moral hazard—that is, to discourage banks from taking excessive risk in the expectation that the central bank would come to their assistance with emergency credit.

If a bank facing a severe shortage of funds were not able to access either the interbank market or the discount window, it would be forced to rapidly liquidate loans and other assets.

The premature liquidation of bank assets that might result is costly for the “real” economy, as it severs valuable relationships between banks and borrowers that may have been cultivated over years and destroys the information embedded in those relationships.

Such relationships are not easily replaced, so the failure of a bank can cause financial distress to its borrowers, particularly smaller firms without access to capital markets.

And just in case you think banks are probably abusing the discount window for some sort of government sponsored free cash giveaway…

Let’s do a quick review of what happened in 2008.

- The Federal Reserve dropped interest rates to basically zero, kept it there for years, and gave banks access to essentially unlimited free money.

- Banks then borrowed practically interest-free money to buy yielding Treasuries or mortgage-backed securities.

- Then they pocketed the interest rate spread.

Why bother lending money to businesses and consumers when you can take a risk-free trade?

Then, in 2022, we finally saw interest rates ratchet up…

And even though everyone assumed the Fed would pivot and drop rates, they didn’t, and carnage ensued.

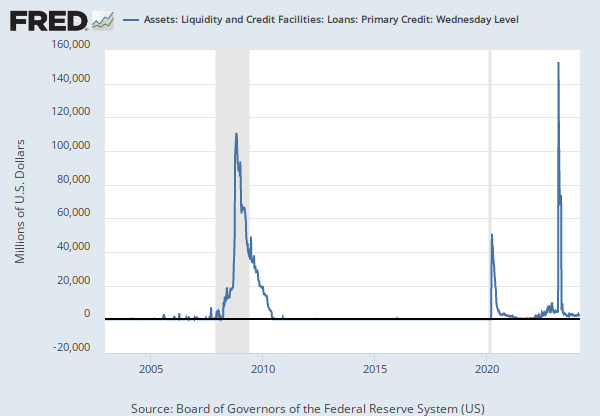

Immediately following the bank failures in 2023, we saw record high levels of borrowing from the discount window.

And then, the BTFP was announced and – as you’d expect – even more borrowing happened: In the first week of the BTFP, banks borrowed $11.9 billion from the program, along with more than $300 billion from the already-established Fed Discount Window.

Except unlike the discount window, under the BTFP, financial institutions DID NOT have to take the haircut – instead, they could borrow against them at face value (par).

Typically, the amount banks can borrow is based on the current market value of their bond portfolios. As bonds tanked, their borrowing ability shrank.

But by valuing collateral at par, the Fed allowed banks to borrow as if the value of the assets never dropped.

Simply put, the BTFP allows banks to borrow more than they otherwise could…

And more importantly, did so in a way that created yet another risk-free trade for banks.

The lower interest rate charged by BTFP created a profitable arbitrage opportunity. Banks could borrow money from the BTFP at a relatively low interest rate (using undervalued bonds as collateral) and then deposit the money in its reserve account at the Fed to earn a higher interest rate than it was paying on the loan.

For instance, the Fed charged a 4.93 percent interest rate on a BTFP loan as of Jan. 23. At the same time, the central bank was paying 5.4 percent on reserves.

This allowed banks to earn nearly 50 basis points by borrowing money and then depositing it in their account at the Fed.

It would be like you taking a 7 percent second mortgage from ABC Bank and then depositing the money into an ABC Bank account that paid you 8 percent interest.

Of course, you would never find that kind of deal in the real world.

As an analyst told Reuters, the interest rate discrepancy “gave banks free profits, which is not a good look.”

Which is why the Fed announced on January 24, 2024 they were closing this free money trade, and raising interest rates on the BTFP to match interest earned on reserve balances.

But now comes the critical question…

One year later, did any of these banks ever bother to address the underlying problems? Or did the can just get kicked down the road?

And with the increasing reserve requirements of Basel III… how many of these banks will be able to survive without another “free money” program like the BTFP?

Only time will tell, but in the meantime, let’s take a look at what’s going on with gold.

Could the End of the BTFP (and Rate Cuts) Finally Trigger the Fabled Gold Bull Run?

Even though the 10 Bitcoin ETFs are vacuuming up cash at record rates…

Gold – and gold miners – continue to defy logic as investors’ attention is firmly on Bitcoin and the “Just Add AI!” narrative.

But just like in the fable “the boy who cried wolf” – could we see the gold bull market that’s decades in the making finally come true?

This week marks 15 consecutive weekly closes above $2000, with all-time high daily and weekly closes…

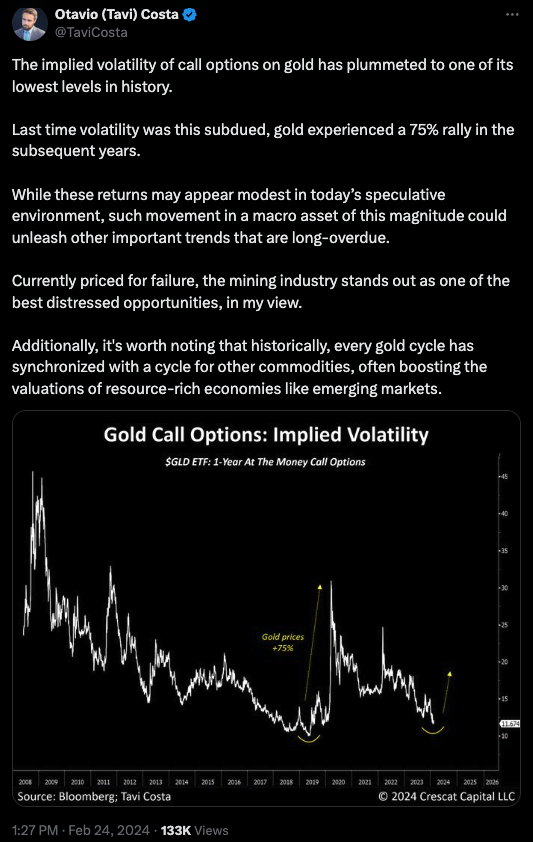

Implied volatility on gold call options has plummeted to one of its lowest levels in history, which could be a signal it’s ready to pop…

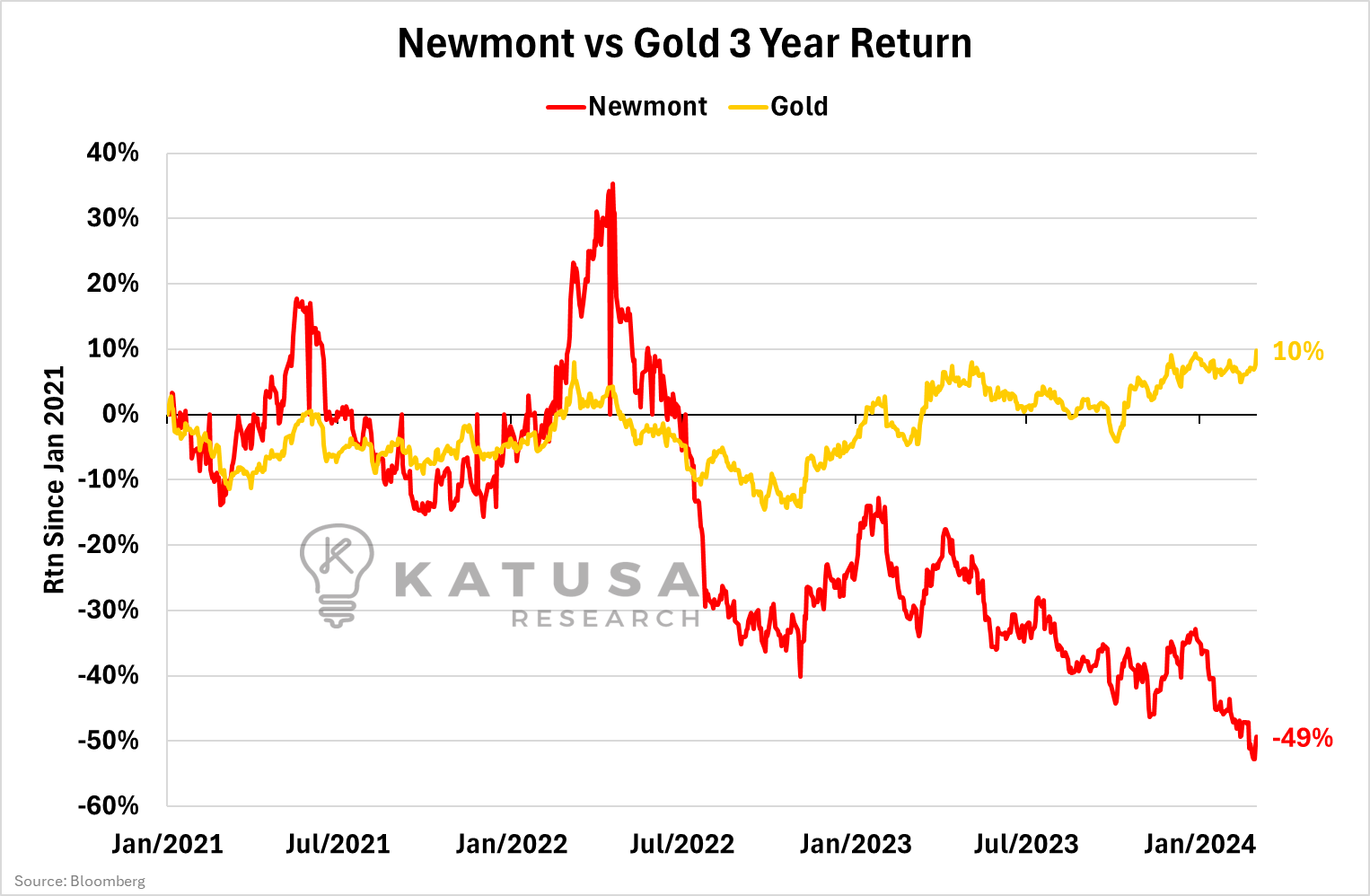

Gold mining stocks (like Newmont) are still in the dumps, trading at a significant discount…

And hardly anyone in the mainstream financial media seems to be reporting on the action in gold, as it seeks to break the psychologically significant $2,100/ounce barrier – a new all-time high.

Market analysts at CPM Group are also not optimistic that the gold market can hold Friday’s gains as it is caught in a well-defined trading pattern:

Gold prices have sold off most every time they have tested resistance levels, and as prices test strong support levels, investors step back into the market, initiating new longs once more.

This has kept gold prices in a wide range, mostly above $2,000.

But the real kicker here is this…

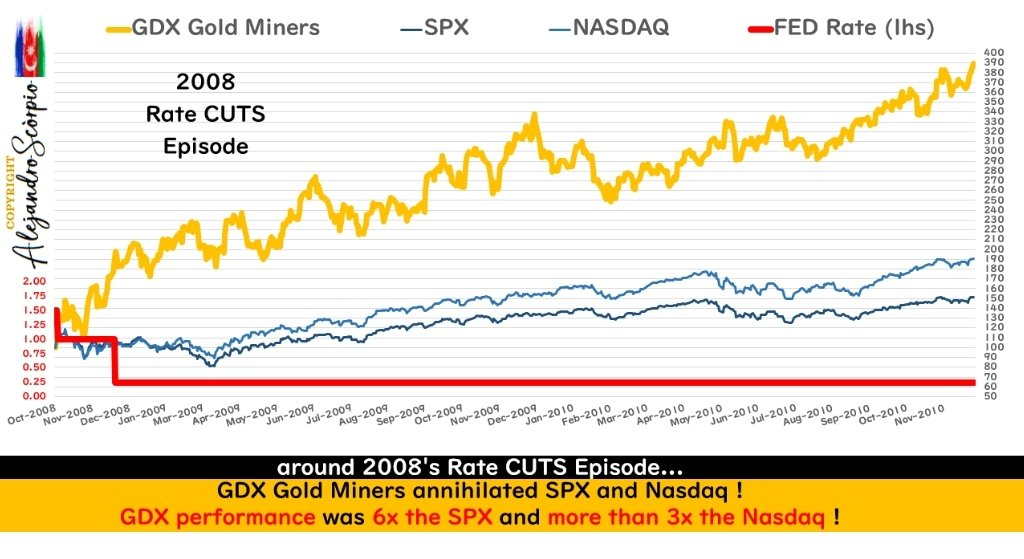

Even though the Bitcoin ETFs are swallowing up enormous amounts of capital, what will happen to gold prices if – in response to the BTFP ending – we get rate cuts instead?

If we get a repeat of 2008, we could see gold make a significant move higher.