For investors looking for a way to turn a small bet on oil prices going higher into potential gains, you might consider buying junior oil stocks, oil futures, or options contracts… but each has its risks.

- Trading physical oil in the short and medium term can be difficult and costly.

- Futures and options can be complicated and extremely risky for investors who do not have a deep understanding of the derivatives markets.

- While oil stocks may appear to be surging, they tend to be far more volatile than most investors can stomach.

But what if there was a way to make a bet on oil that offered the downside protection of real assets, the more predictable cash flow of real estate, and the upside potential of technology stocks?

Even better, what if you could buy into this investment opportunity at a discount to market value?

Chances are, you’d be looking at what could rightfully be considered the value investor’s “sweet spot.”

And just in case you’re wondering what the Patron Saint of Value Investing, Warren Buffet, thinks about energy stocks…

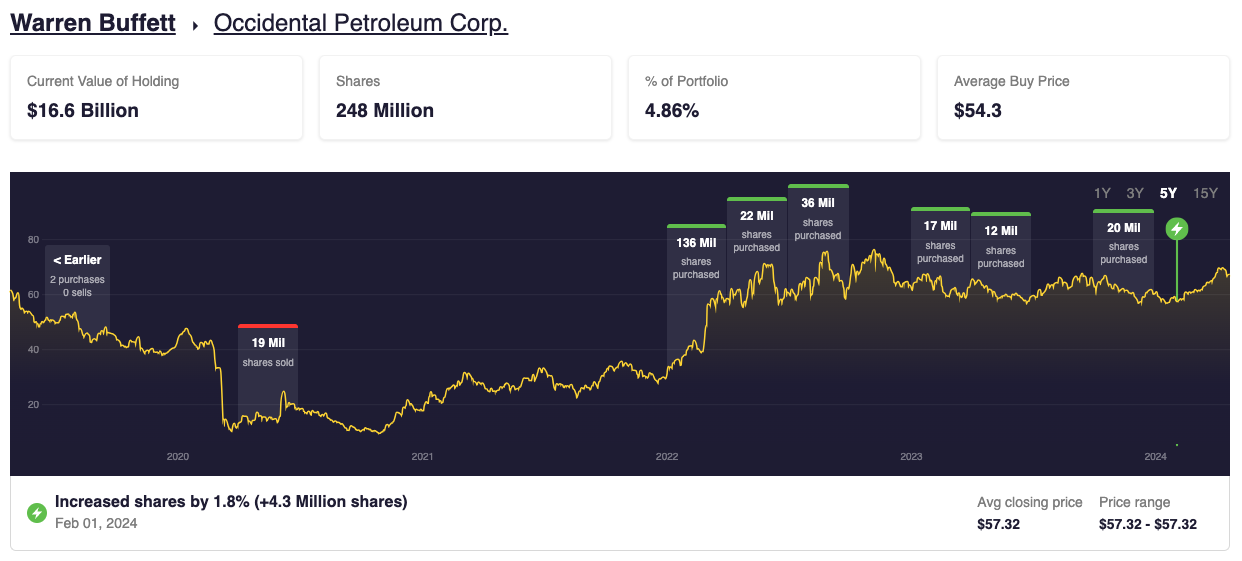

Berkshire Hathaway added $588.7 million – more than 10 million shares – to his bet on Occidental Petroleum (OXY) between Dec. 11-Dec. 13 @ ~$56/share; then, another 5.18 million shares on Dec 19th, and another 4.3m shares on Feb 1, 2024.

Source: StockCircle

With ~$15 billion of total capital invested into OXY since 2019 – a ~28.2% stake of this $53 billion company – thanks to OXY’s dividend, Berkshire receives ~$218.3 million in annual dividend income from this position.

Occidental pays a dividend, currently yielding 1.5%. Berkshire receives $218.3 million in dividend income from this position. Source: Yahoo Finance

According to Berkshire’s 2023 letter to shareholders

We particularly like [OXY’s] vast oil and gas holdings in the United States, as well as its leadership in carbon-capture initiatives, though the economic feasibility of this technique has yet to be proven.

Both of these activities are very much in our country’s interest.

Under Vicki Hollub’s leadership, Occidental is doing the right things for both its country and its owners.

No one knows what oil prices will do over the next month, year, or decade.

But Vicki does know how to separate oil from rock, and that’s an uncommon talent, valuable to her shareholders and to her country.

Just to be clear, we’re not making any sort of buy/sell recommendation on OXY…

But if one of history’s best investors has major positions in oil and gas stocks – Berkshire’s fifth largest position is Chevron and sixth largest position is Occidental Petroleum – we take notice.

So, before you go hunting for “value” in the volatile energy sector – especially in smaller, private oil and gas projects…

The #1 thing you must understand is how oil and gas assets are valued, what types of corporate milestones drive valuation, and the many ways management may return capital to investors.

That’s the topic of today’s issue of Private Capital Insider.

Let’s get into it,

-Jake Hoffberg

A Brief Primer on Investing in Oil and Gas: Why Family Offices are getting in when institutions are getting out

One of the themes we’ll come back to over and over again in Private Capital Insider are the major problems small balance investors have when putting capital to work in private deals.

Generally speaking, we can think about these challenges across five categories:

- Access: Getting access to the top funds is already hard for professional investors with hundreds of millions of dollars under management. You – the average retail investor – have almost no chance of getting invited into the “club.”

- Underwriting: Even if you did have access, you likely don’t have the time or resources required to perform any substantive due diligence.

- Check Size: Even if you did have access and could underwrite the deal, you may not have enough money to meet the minimums (or if you do, it’s probably a significant portion of your investable assets).

- Liquidity: Even if you could get your money in a deal, most retail investors don’t want to get locked up for 7-10+ years.

- Fees: If you are investing through fund vehicles, fees over the life of the fund can seriously eat into returns. In order to produce a 15% net-of-fee return, an investor in a fund vehicle needs to have the manager produce a gross-of-fee return of 22-24%+ (depending on fee structure).

All said and done, this does not paint a favorable proposition for retail investors looking to diversify into private markets on their own.

For this reason, it’s highly likely that retail investors will rely on some sort of relationship with an intermediary/promoter/advisor of some sort to “introduce” them to the types of investment opportunities they are looking for.

However, before we jump head first into a sexy sounding “single stock” opportunity – especially an early stage investment opportunity in the private markets…

We think it’s a good idea to be aware of all the available options you have to express your investment thesis to establish an appropriate “benchmark.”

Why? Because inevitably, you’re going to have questions – like “is this a good investment opportunity?” or “how much should I invest?” – that can only be answered relative to your other available options (called “Opportunity Cost”).

For example, if you believe there’s money to be made in energy stocks due to rising oil and gas prices, and you’re looking for a way to get “exposure” to this theme…

Generally speaking, you’ve got four major strategies to choose from:

- Passive – Buy and Hold Sector-Based ETFs: The idea here is to “hire” a manager to do the stock picking for you.

- Semi-Passive – Create your own basket: Maybe you like the idea of a diversified basket of stocks for the “energy” allocation in your portfolio, but you want something more customized than the currently available products.

- Active – Day trading options, futures, and leveraged ETFs: Just in case oil and gas stocks aren’t volatile enough for you, there’s no shortage of “lottery ticket” style opportunities for short term bets.

- You Only Live Once – Bet it all (or just way too much) on a single stock: As bad of an idea as this is, we find it’s surprisingly common that individual investors put WAY too much money into a single position they may not fully understand.

Which strategy is right for you? Again, this is another question that can only be answered relative to your financial goals and asset allocation model (i.e., what percentage of your portfolio are you looking to allocate to energy?).

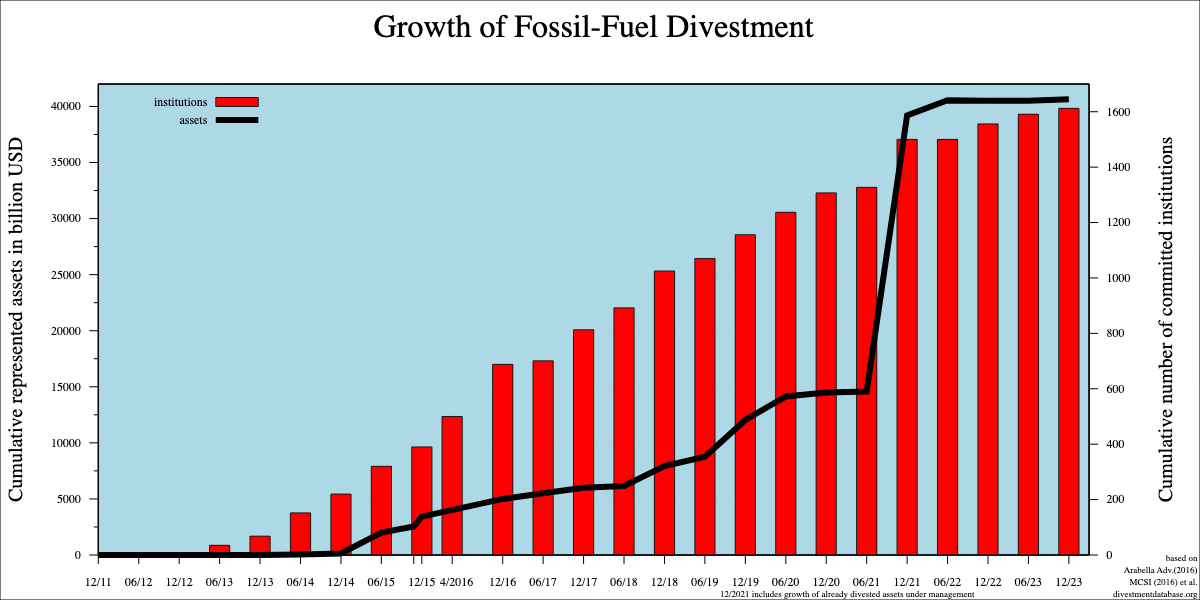

For example, in a world where more than 1,600 institutional investors have soured on energy and are actively divesting from the sector – By 2022, $22 trillion had been divested from fossil fuels across public and private markets, with over $40 trillion assets now committed to divestment, representing almost two-thirds of the total global pension fund assets under management ($56 trillion)…

Family offices are stepping up to fund oil and gas plays, as this “forced selling” creates an obvious buyers market with the chance to pick up quality assets at attractive valuations.

According to Joe Flack, attorney for Jackson Walker,

I think they’re interested in producing assets because they have consistent returns relative to other assets they would invest in.

According to Mike Vlasic, whose family office has invested profitably in oil and gas for decades,

Most people aren’t looking at the oil and gas boom-bust cycles in the right way.

While many companies faced bankruptcy during the busts, the cycles also showed the industry’s resilience.

The oil and gas industry in this country is extremely sophisticated, has tons of ingenuity and has thrived and survived in a variety of market conditions that other industries would not.

According to one of the Vlasics’ early partners, Frank Lodzinski of Earthstone Energy,

The industry has shown greater discipline than it has in the past in terms of controlling its leverage and developing free cash flow that it uses for returns or for growth.

The discipline has offset some of the fears of volatility and massive commodity price swings.

And just in case you’re not convinced this is actually happening, be sure to check out this Digital Wildcatters Podcast with the head of Stephens Inc’s Energy practice.

We took a deal out I guess about four years ago to all typical PE funds and we didn’t get any kind of reception. It was clear the market had changed.

We stood up a family office coverage group about seven or eight years ago – really a financial sponsors coverage group covering family offices – covering like 350 family offices and started working with that group to identify which of their families were interested in investing in oil and gas.

They started trickling in and I think we’re [now serving] like 50 to 70 [families].

We closed two deals last year, so you know there is money coming into the space.

The way our family office coverage group kind of qualifies families that they want to work with they can they need to be able to cut at least a $20 million check per deal.

Getting family offices to divert their attention away from these other sectors that were on fire at the time. [Editor’s note: things like crypto/web3/AI]

In the last three years … we’ve had more and more families that are trying to get out of what they’ve previously been investing in and are showing a lot of interest in Upstream.

Back in the shale boom, the way valuations worked, you had to put a lot of value on the upside.

If you back that into your effective cash flow multiple you’re investing it was off the charts.

They’d say “there’s no way I’m coming in at 10 times EBITDA” or whatever it was, but I think [they now see] all this capital is leaving the space for kind of irrational reasons.

Because that capital is leaving the space, we can come in and invest at two to three and a half times cash flow.

To be clear, just because family offices are investing in upstream oil and gas plays doesn’t mean you should.

But if you are considering an Upstream investment – and ideally one where you can get in at an attractive valuation – let’s talk about how these assets are priced.

An Introduction to Valuing Oil and Gas Stocks

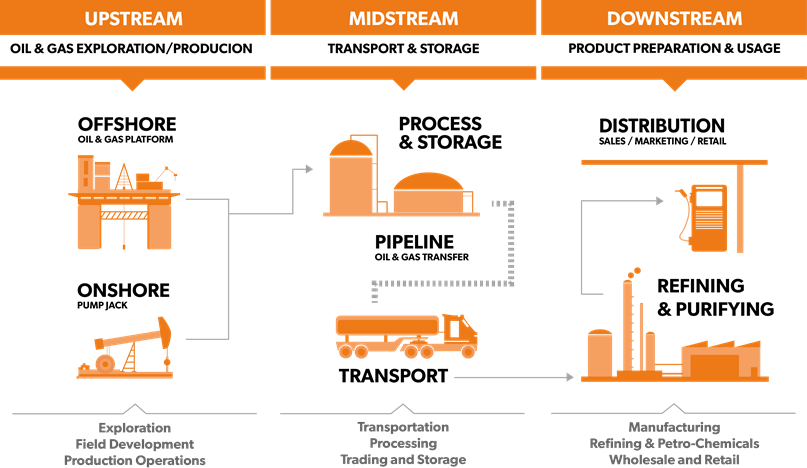

The oil and gas industry’s value chain is classified into three distinct segments or sectors:

- Upstream (also known as exploration and production, or “E&P”) extracts feedstocks used to produce fuels and petrochemicals

- Midstream moves and stores feedstocks and finished products

- Downstream processes crude oil and natural gas into finished products

Source: Eland Cables

We’re going to stay focused on Upstream for this article, as this is the most likely type of company you’ll see in private markets.

Generally speaking, the value of an E&P company may be estimated by calculating the fair value of its reserves and then aggregating this with the value of other net assets on its balance sheet, assuming those net assets have been assigned market value.

Reserves can be classified into three main categories:

- P1 – Proved Reserves: quantities of oil or natural gas that are recoverable in future years from known reservoirs under existing economic and operating conditions

- P2 – Probable Reserves: quantities that have a 50% probability that the reserves quantities will be lower than estimated, in accordance with the engineering definition of the American Petroleum Institute

- P3 – Possible Reserves: quantities that have a 10% probability that reserves quantities are higher than estimated, and a 90% probability that reserves quantities will be lower than estimated

Reserve reports, generally prepared independently by petroleum (or reserve) engineers, are used for this purpose. The reserve report is essentially a discounted cash flow model for a company’s oil and gas reserves, on a pre-income tax basis.

The report typically includes the present value (PV) of the projected income based on various benchmark rates, frequently ranging from 10% to 25% discount (often referred to as PV 10 to PV 25).

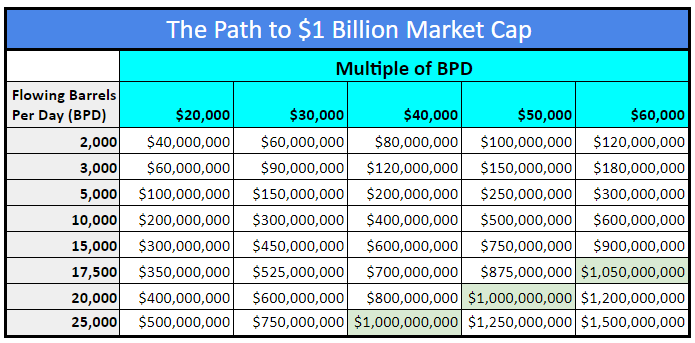

While the discounted cash flow model is a mainstay of valuation techniques, flowing barrels per day (BPD) is a key metric used by oil and gas companies in both operational and valuation contexts.

Essentially, BPD represents the volume of oil or gas produced daily from a particular well, field, or asset. For this reason, BPD is crucial for assessing the production capacity, revenue potential, and overall performance of oil and gas assets.

Here’s how upstream oil and gas companies utilize BPD as a valuation metric:

- Production Forecasting: BPD serves as a fundamental input for production forecasting. Oil and gas companies use historical production data, reservoir analysis, and well performance metrics to estimate future production levels.

By projecting the expected BPD output over time, companies can assess the revenue generation potential and make strategic decisions regarding asset development, investment, and operational planning.

- Revenue Estimation: BPD directly impacts revenue generation for oil and gas companies. The daily production volume, along with prevailing commodity prices, determines the revenue stream derived from the sale of oil and gas products.

Companies use BPD as a basis for revenue forecasting, budgeting, and financial planning. Higher BPD levels typically translate to increased revenue potential, assuming stable or favorable market conditions.

- Asset Valuation: BPD plays a significant role in the valuation of oil and gas assets, particularly producing fields or reserves. When assessing the worth of an oil or gas asset, investors, analysts, and industry professionals consider the current and projected production levels.

Higher BPD figures indicate greater production capacity and revenue potential, which can positively influence the valuation of the asset. Valuation methodologies such as the Income Approach often incorporate BPD projections to estimate future cash flows and derive the present value of the asset.

- Comparative Analysis: Oil and gas companies and investors often use BPD as a basis for comparative analysis. When evaluating different assets or investment opportunities, stakeholders may compare the BPD metrics to assess relative production efficiency, reservoir quality, and operational performance.

Comparative analysis helps in identifying high-performing assets, optimizing portfolio allocation, and identifying potential acquisition or divestiture targets.

- Operational Performance Evaluation: Monitoring BPD provides oil and gas companies with insights into the operational performance of their assets.

Fluctuations in BPD levels may indicate changes in reservoir dynamics, well productivity, or production efficiency. By tracking BPD metrics over time, companies can identify operational challenges, optimize production processes, and implement strategies to enhance asset performance and maximize production yields.

Similar to other industries, as the company increases in size and scale, investors are often willing to assign higher multiples as the certainty of future cash flow increases.

This means that as the company begins to grow in size and scale, the valuation multiple on BPD may potentially increase.

According to Pytheas Energy’s management team,

If you can buy for anything less than $20,000 BPD, we think that is a great deal. When oil is over $65, we believe the fair market value for that well is around $40,000 BPD.

If oil is over $80 – like many analysts are predicting it will be for the next few years – we could see BPD as high as $50,000-$60,000.

If all goes according to plan, we are looking to acquire a property, modernize operations and equipment, and otherwise increase BPD on the asset… we could potentially sell parts of our portfolio for a 6-10x return on invested capital in an 18- to 24-month window.

However, while BPD is a useful “look back” metric of historical production and growth/decline, it cannot be relied on in a vacuum for valuation, as it does not take into consideration future production/future cash flow for distributions.

For this reason, to establish a more precise valuation, we also have to consider revenue, margins, targeted yields and distribution model – as well as how these values may change over time as the business matures in size.

However, it’s important for investors considering an E&P investment to understand what this type of valuation model is sensitive to – namely, fluctuations in commodity prices and production rates.

Let’s start with commodity risk…

If oil prices increase (decrease), this has the potential to increase (decrease)…

- the value of the underlying properties

- the cash flow from the assets acquired

- The overall liquidity in the market for these assets

If you want to learn more about oil price forecasts, be sure to check out some of our other coverage on the topic.

[Editor’s note: Our view at Equifund is we think oil prices are likely going to continue to trade above $80 – with a potentially clear path to $100+ – for the next few years]

However, because every investment is subject to the market forces that determine the commodity price, it’s a risk we just have to accept.

In order to manage commodity risk, the major thing we need to keep an eye on is the average price of oil and gas required to produce at a profit (referred to as the “all-in sustainable cost” or AISC in the mining world).

While this commodity risk has the potential to create plenty of volatility that could blow up the investment opportunity…

Oil has to be one of the best commodities to own in a rising inflation environment (as energy prices tend to be a significant driver of inflation).

However, assuming oil prices remain above the AISC of the field, the main thing we’re looking at is management’s ability to improve production.

Now let’s talk about execution risk…

Every E&P has essentially the same “Fix and Flip” business model – buy low, sell high, and don’t lose too much money in between.

Fundamentally, this means we need to believe in Management’s ability to originate (and close) deals, manage the property, and dispose of them at a profit.

On the buying and selling side…

One of the nice parts about buying oil and gas assets is that there’s a very “bright line” method for determining asset values – the reserve reports

Unlike other early stage companies where much of the valuation is speculative, based heavily on the future value of the intellectual property or technology, with much of the value relying on an often aggressive forward looking forecast…

All producing wells come with a reserve report that more or less tie future production to historical production rates – which, in turn, sets the fair market value for the asset.

While asset-light businesses (i.e., technology companies) might have the ability to grow rapidly and deliver extraordinary returns, they offer little downside protection for investors.

Conversely, asset-heavy businesses (i.e., oil and gas companies) have actual assets on the balance sheet that provide downside protection.

Not to mention, when you’ve got a highly in-demand commodity like oil and gas, there’s basically always a willing buyer somewhere.

For the sake of simplicity, let’s just say that buying and selling oil and gas assets is relatively straightforward, and everyone is equally as good at it.

This means the true “value creation” mechanism for shareholders lies in Management’s ability to improve output of the wells.

For a lot of obvious reasons, there’s a level of excitement around how artificial intelligence can help with this.