While everyone else is talking about the Biden-Trump rematch, more drama around the Musk/OpenAI lawsuit, and the State of the Union…

Here are the stories that haven’t been getting much attention.

- U.S. bank profits drop 44% in Q4 as big firms cover failed bank costs: The U.S. banking sector saw its profits drop by nearly half in the last quarter of 2023, as large firms began paying hefty fees to help recoup costs incurred by several bank failures last spring, the Federal Deposit Insurance Corporation reported Thursday.

- NYCB Raises More Than $1 Billion in Equity Led by Steven Mnuchin’s Firm: Commercial real estate lender New York Community Bancorp received an equity investment of more than $1 billion, gaining a vote of confidence in the struggling lender from investors, including former US Treasury Secretary Steven Mnuchin.

- Fed’s Powell Says Significant Changes to Bank Capital Plan Likely: Federal Reserve Chair Jerome Powell said that U.S. regulators are likely to significantly change their plan to require large lenders to hold more capital — a move that would mark a major win for Wall Street giants.

- Powell: ‘There will be bank failures’ caused by commercial real estate losses: Powell also said Thursday he expects to see some banks fail due to their exposure to the commercial real estate sector, which has declined significantly in value following the shift to remote work. Probably nothing, right?

And if we had to sum it all up in one FinTweet, here it is.

That’s what we’re covering in today’s Weekend Edition of Private Capital Insider.

Let’s dive in,

-Equifund Publishing

P.S. Gold also hit an all time high, miners are still trading a deep discount, and pretty much no one is talking about it. While this is certainly a story we’re tracking as part of the “most predicted recession of all time” narrative, we’ll see where we are after we get through next week.

Also notable news we’ll likely cover next weekend, HR 2799 passed the House and is on its way to the Senate.

The NYCB Thing Gets Worse. Then Better. But Also Worse.

As a reminder, we don’t like to make predictions, nor do we particularly enjoy doom and glooming.

But the slow motion dumpster fire that is NYCB is like the news story that keeps on giving.

For whatever reason, this single regional bank stock manages to connect to a variety of other stories we’ve been following in Private Capital Insider.

For those not in the loop on what’s going on, here’s the short version…

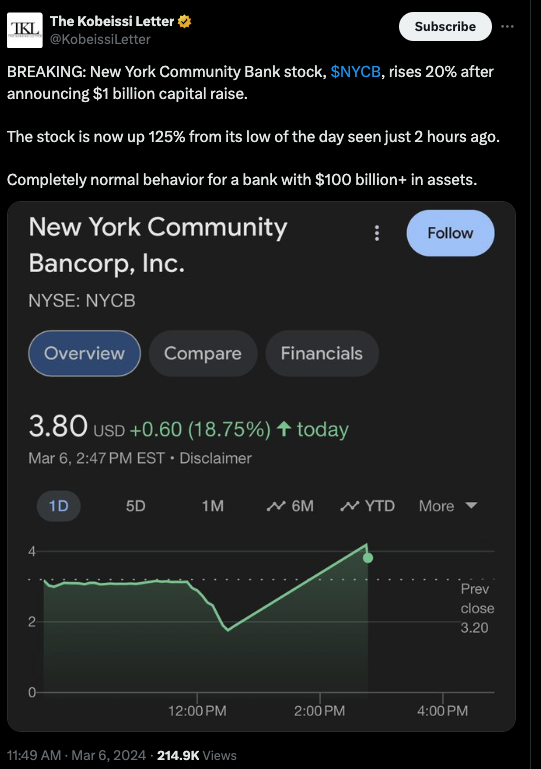

- Friday, March 1st: NYCB revealed major weaknesses in its ability to monitor risks and replaced Thomas Cangemi as CEO with Flagstar Bank’s Sandro DiNello… and the stock tanks on the open.

- Wednesday, March 6th: NYCB announces they need to raise funds. After The Wall Street Journal reported on the fundraising effort, the stock plunged more than 40%.

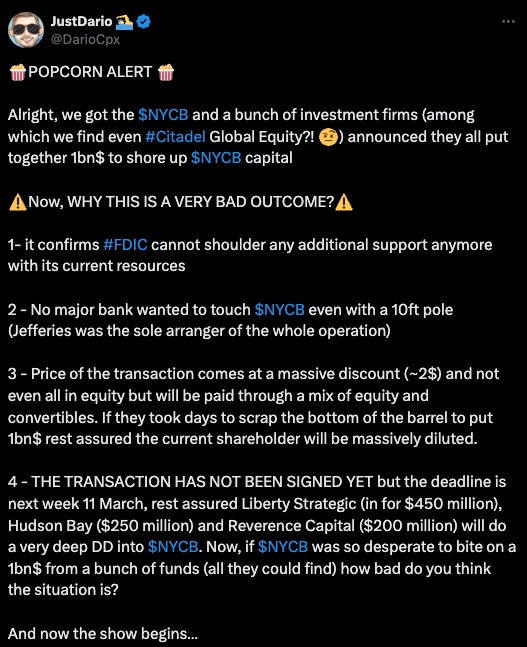

Steven Mnuchin, along with a rather interesting cast of characters, steps in with a $1bn offer that will dilute the heck out of existing shareholders.

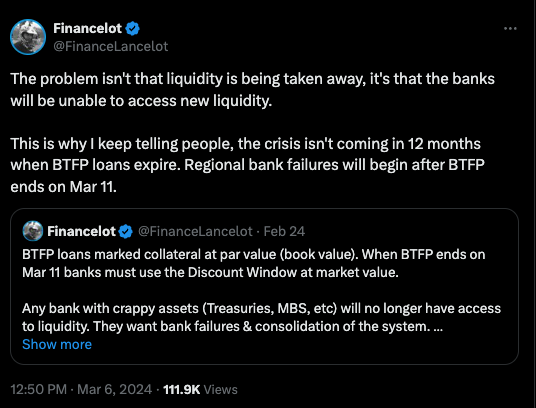

However, the deal doesn’t officially close until Monday, March 11th – which just so happens to be the end of the Federal Reserve’s BTFP (which we covered in the March 2nd Weekend Edition).

To kick things off, let’s start with a bit of a roundup of the mainstream media coverage.

According to Jenny Van Leeuwen Harrington on the March 6th CNBC Halftime Report Investment Committee:

Maybe the regulator shouldn’t have let them acquire [Signature Bank]. No, in retrospect, they should have, because what that did was bump them into that 100 billion asset level.

And what this arrogant management team did was fail to realize a year ago when they got those assets, that they should have brought in other management who had experience at the big bank level.

If they brought them in a year ago, maybe they would have managed that transition to a larger scale bank better.

The other thing that I want to make a point on is this share price at $1.86 is really upsetting. And part of it is because there’s a lot of predatory players out there.

There’s too many parties right now incentivized to pick off NYCB’s really valuable assets there – Real estate, loans, mortgage servicing business, and there’s all these predators who know how to manipulate the share price very effectively.

So they may be buying those at fire sale assets.

We the public shareholders get punished the most. It’s a huge disappointment.

Lots to unpack here, but let’s go in order.

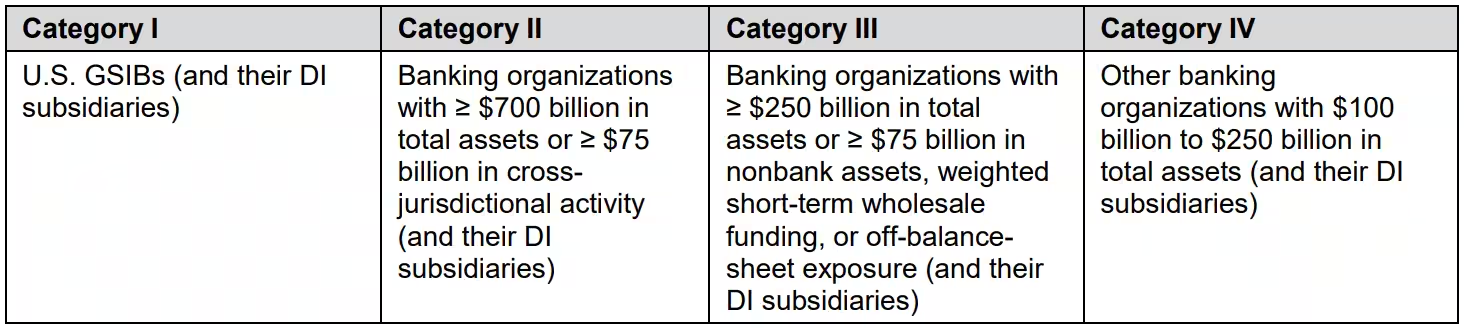

When NYCB acquired Flagstar Bank – and then parts of Signature Bank – this moved NYCB into a “Category IV” Bank.

One of the changes motivated by the Silicon Valley Bank (SVB) collapse in March is the requirement, applicable to all banks with >$100bn assets (i.e., Cat I-IV), to include unrealized gains and losses from their AFS (Available-For-Sale) and HTM (Held-To-Maturity) portfolios in their regulatory capital.

This was one of the drivers of the SVB collapse, when a deterioration in their HTM portfolio, due to the rising interest rates environment, sparked the panic across depositors about the solvency of the bank.

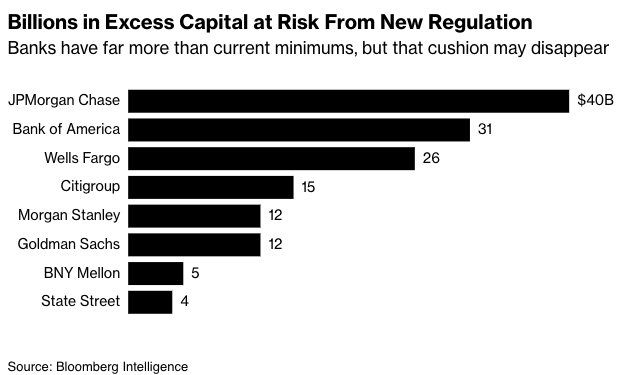

This acquisition also moved NYCB directly into the crosshairs of the Basel III reserve requirements. If approved, they would force a 19% jump in the required capital for the biggest lenders.

While there is some growing indication these reserve requirements may change – Federal Reserve Chair Jerome Powell said that U.S. regulators are likely to significantly change their plan to require large lenders to hold more capital…

Until they do, willingly putting your bank into these crosshairs is just… a weird decision.

Second, the management team

Last week, NYCB revealed major weaknesses in its ability to monitor risks, and replaced Thomas Cangemi as CEO with Flagstar Bank’s Alessandro DiNello.

So who are Mnuchin & Friends bringing in to lead NYCB?

Joseph Otting, the former head of the Office of the Comptroller of the Currency – and previous turnaround CEO for Mnuchin when he bought failed mortgage lender IndyMac (which became OneWest) – will become CEO, replacing DiNello, who had taken over less than a week ago.

Mnuchin, Otting, Reverence’s Milton Berlinski, and Hudson Bay’s Allen Puwalski will join the NYCB board, which will be reduced to nine members and purged of all legacy NYCB directors.

Third, the entrance of predatory players and potential market manipulation

While CNBC didn’t go into much detail on this topic, it’s one worth paying attention to.

Here’s one of the strangest parts about this deal. According to Bloomberg,

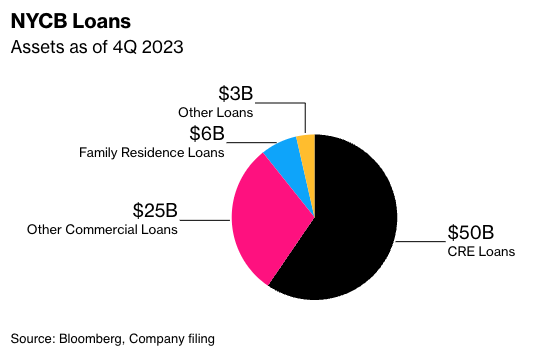

NYCB is a major lender to owners of apartment buildings subject to tough New York rent laws, limiting the revenue units can generate.

It also financed offices in a region beset by vacancies in the work-from-home era.

Credit-rating firms have slashed the company’s grades to junk, with Moody’s Investors Service predicting the bank may set aside more money for souring loans over the next two years.

In 2019, New York renters won sweeping new protections that stopped landlords from raising rents on regulated apartments. Owners were outraged, and their banks found themselves under pressure.

NYCB’s loan portfolio was almost all mortgages, mostly multifamily, and most of those subject to New York rent rules.

Remind me again why exactly anyone wants to acquire a book of loans concentrated in rent-stabilized buildings?

Maybe they don’t.

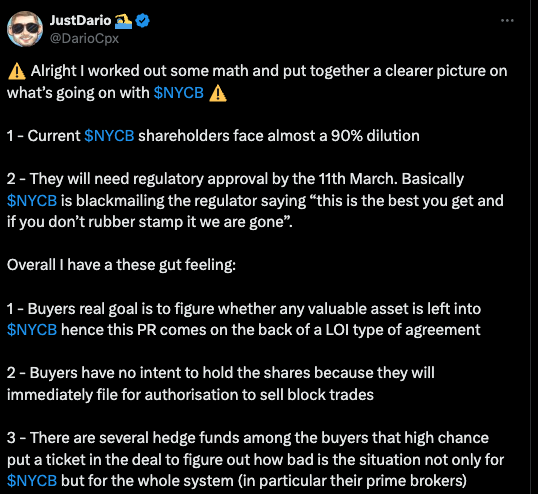

Let’s take a look at what FinTwit thinks.

Could this be just another round of “pass the hot potato of toxic assets,” while scraping out all the good ones?

Or maybe the better question… What happens when the bank that bailed out a failed bank, fails?

Apparently, if you’re Mnuchin & Friends, you get one of the most incredible trades of all time, when you basically double your money in two hours.

I wonder if they shorted the stock on the way down too?

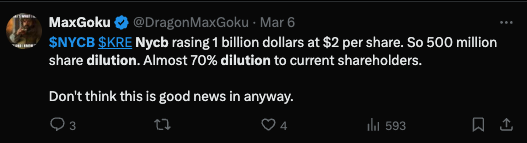

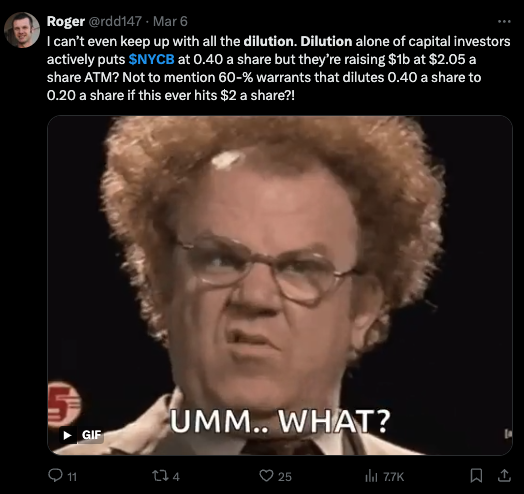

Fourth, the highly dilutive terms that have all but wiped out the previous investors.

The new capital infusion has boosted shares since the announcement Wednesday afternoon, with analysts saying it bolsters confidence despite dilution to existing shareholders.

Further details were given Thursday, with NYCB saying the new investors will hold 41.4% of the firm on a converted fully diluted basis.

The firm is issuing nearly 60 million shares of common stock at a price of $2 each, as well as warrants with a term of seven years.

However, this 41.4% number DOES NOT include the warrants, which have a strike price of $2.50 – a 25% premium above what they paid for the common stock.

I guess we’ll see what happens next week.