Last week, we kicked off our “Private Capital Worldview” series with a look into KKR’s “Regime Change” thesis.

This week, we continue with the world’s largest alternative asset manager and corporate landlord, Blackstone.

Slight plot twist: While the majority of asset managers tend to publish regular market outlooks and analyses, Blackstone has a much different approach to publishing – educational programs designed for the wealth management / financial advisory channel instead.

Why? It all comes back to retail investors.

Let’s dive in,

-Jake Hoffberg

P.S. Today’s edition builds off the foundational investment philosophy we discussed in the January 17th (Searching for “Truth” in Early Stage Investing) and the January 25th (Turning ideas into investments (that hopefully make money) editions of Private Capital Insider.

P.P.S Looking for back issues of Private Capital Insider?

Blackstone and the Quest for Global Retail Money

Blackstone was founded in 1985 by Peter G. Peterson and Stephen A. Schwarzman, with $400,000 in seed capital.

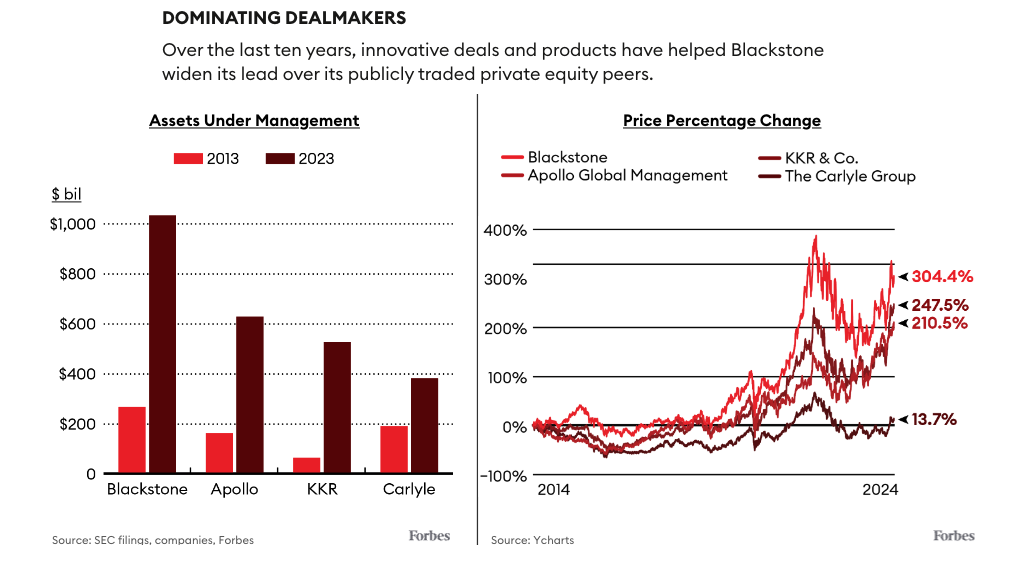

Today, Blackstone is the largest alternative asset manager in the world, with more than $1 trillion of assets under management (AUM).

While there’s plenty of palace intrigue surrounding the nearly 40-year history of the firm…

It’s Blackstone’s efforts to penetrate the retail investor channel that I find the most interesting.

In the 80s and 90s, the establishment worried about the so-called “Barbarians at the Gate,” as private equity rose to power.

But now, as private equity and venture capital have saturated the institutional markets, the Barbarians of Wall Street are about to face off against the Apes of Main Street.

Taking inspiration from the line “apes together strong” in the movie “Rise of the Planet of the Apes”… retail investors, calling themselves “apes,” believe if they are united, they can outlast those that are short on their favored meme stocks.

For the past decade, Blackstone has been working on growing its retail platform; at the end of Q3 2017, 18% of the firm’s $387.4 billion AUM was retail investors.

On the company’s 2017-Q3 earnings call, Joan Solotar – head of private wealth solutions at Blackstone – said, “there’s no reason that ultimately it won’t account for half the assets we manage” in the next 5-10 years.

Who do they think those assets will come from? According to Ms. Solotar, “We are targeting the $1 million to $5 million investor. They are really under-penetrated in the alts business.”

Then, on January 14th, 2020, John Finley – Chief Legal Officer at Blackstone – gave a presentation to the SEC titled “Expanding Retail Access to Private Markets.”

In it, he revealed some rather shocking numbers…

Retail investors represent ~$68T of global assets, with $1-$5m households representing roughly $30T of assets.

But that’s just the tip of the iceberg…

By 2025, the total pool of retail assets is expected to balloon to $106T worldwide!

And with an average five percent allocation to alternatives, even a modest increase to a 10% allocation could represent an extra $5.3T of assets shifting to alternatives.

If retail matched pensions at a ~30% allocation, it would mean an extra $26.5T of assets flooding into alternatives!

Combine that with the explosive growth of retail traders entering the markets since the start of COVID-19, and we could see a radical shift in the way capital markets function.

Today, nearly a quarter of Blackstone’s $1T in assets come from private wealth, growing at a compound annual rate of more than 30%.

‘It’s not lost on distribution partners—who are being approached by everyone under the sun—that competitors have seen Blackstone’s success, and are jumping on the bandwagon,’ said Solotar.

“It’s a land grab,” said Matt Brown, chief executive of CAIS, a platform that gives independent financial advisers access to so-called alternative investment products. “You’re seeing the mutual-fund boom 2.0,” he said, referring to the rise in popularity of mutual funds during the 1990s.

With $1 trillion in assets and unrivaled returns, the private equity giant has conquered Wall Street, but its 76-year old founder, Steve Schwarzman, isn’t finished.

If you get Schwarzman, whose net worth currently hovers around $38 billion, talking about the business he created in 1985, you’ll soon realize that the old leveraged buyout game that he helped perfect is going through a revolution.

In the United States, traditional private equity—raising money from large institutions to acquire stodgy companies, taking on mounds of debt and then slashing costs and rejiggering the capital structure for quick profits—is dying, or, at best, a slow-growth business.

There are more than 2,000 private equity firms today, up from fewer than 500 a decade ago.

The new game, dubbed alternatives, is all about growth. Firms buy companies in areas like logistics, infrastructure, life sciences and e-commerce, and make them bigger, not smaller.

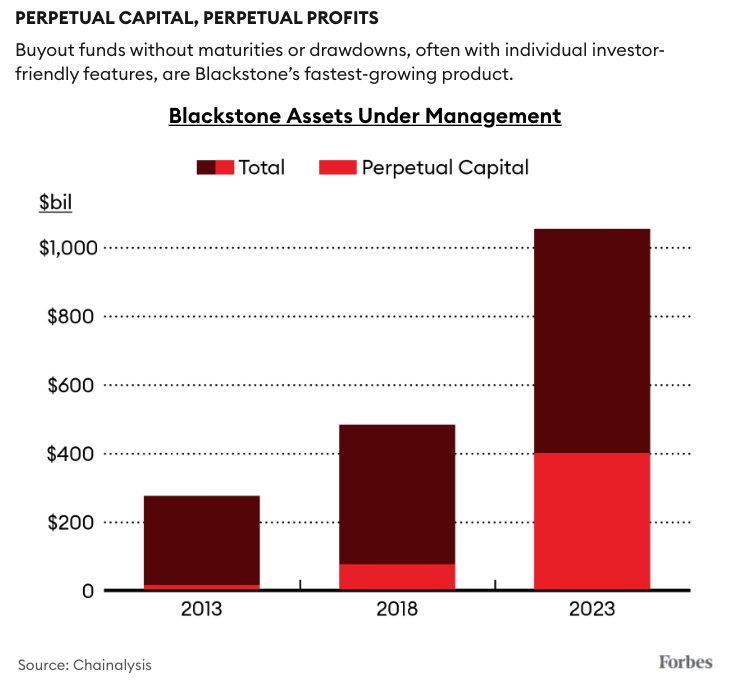

Unlike old-school buyouts in which fund lifespans were limited to ten or 12 years, contributing to a slash-and-churn culture, the hottest funding source in the business is now something called perpetuals: buyout funds that are often individual investor–friendly and have no end date.

Like Warren Buffett’s Berkshire Hathaway, Blackstone’s new schtick is buy and hold, and the new funds enforce this by limiting redemptions.

Up from almost nothing a decade ago, these novel perpetual funds now account for 38% of Blackstone’s $1 trillion in assets under management and even more of its fee income.

And this massive push into semi-liquid private funds – also called “evergreen” or “perpetual” funds – is the cornerstone strategy driving…

Blackstone’s $80 Trillion Opportunity

In a stroke of cosmic good luck for my research, on February 5th, 2024, Forbes published a cover story on Blackstone president, Jonathan Gray, and his plan to further expand the Blackstone empire.

Raised in the suburbs of Chicago, Gray joined Blackstone in 1992, after graduating from the University of Pennsylvania.

By 2005, at just 34 years of age, Schwarzmann tapped Gray to lead the firm’s growing real estate division.

According to Schwarzman, Gray distinguished himself with a pair of astute strategic insights, which led to two of Blackstone’s most profitable deals:

- The acquisition of Sam Zell’s massive Equity Office Properties for $39 billion, and

- Blackstone’s $26 billion acquisition of Hilton Worldwide, which included properties like New York’s Waldorf Astoria and Hilton Hawaiian Village

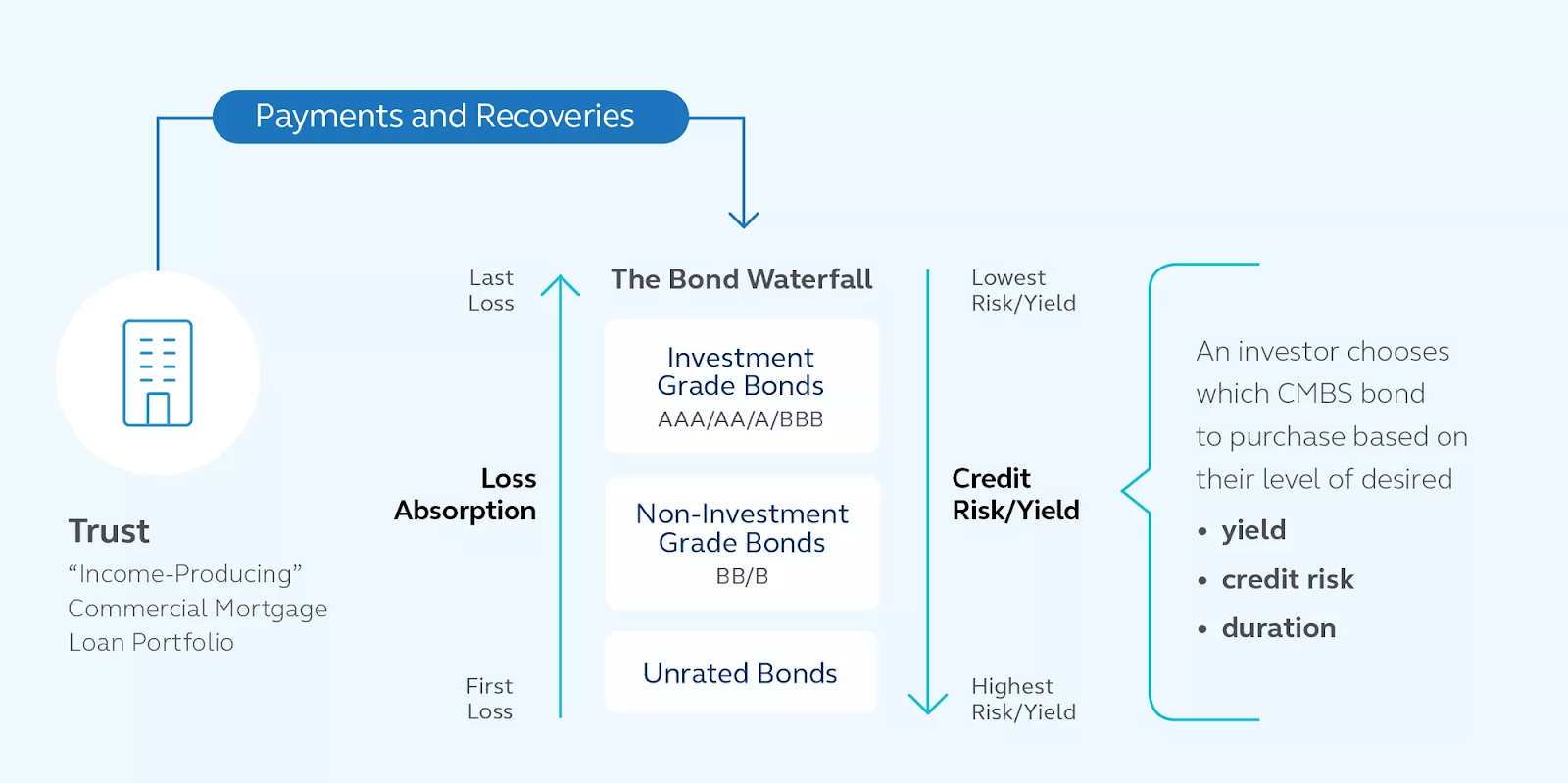

Gray was early to embrace commercial mortgage-backed securities (CMBS), which would allow Blackstone to do larger deals at a lower cost.

CMBS are fixed-income investment products that are backed by commercial mortgage loans on items such as retail properties, office properties, industrial properties, multi-family housing, and hotels.

Unlike residential mortgage loans, commercial mortgage loans often have strong protections (“lock out periods”) against prepayments for up to ten years.

Similar to collateralized debt obligations and collateralized mortgage obligations, CMBS are issued as bonds.

The mortgage loans that form a single, commercial mortgage-backed security, act as the collateral in the event of default, with principal and interest passed on to investors.

The emergence of CMBS in the early 1990s changed the market for commercial mortgages fundamentally—for lenders, borrowers, and investors.

Lenders no longer had to keep the mortgages they issued on their books for the duration of the loan. Instead, they could sell the stream of interest and principal payments to investors, freeing up their capital for more lending or other business activities.

Borrowers, meanwhile, benefited from improved loan availability and competitive rates.

Gray also saw that Blackstone could buy publicly traded real estate companies – many whose owners had acquired properties over several years – for less than the sum of their individual holdings.

With most of the firm’s profits coming from the $115 billion real estate business Gray built, Schwarzman named him president and chief operating officer in 2018, succeeding another Blackstone-minted billionaire, former vice chairman Tony James.

Now, Gray is leading Blackstone’s international expansion… and the quest for the estimated $80T of global wealth held by individual investors.

Interestingly enough, Jonathan Gray was the “founder” of perpetual funds at Blackstone – which is now set up to be the major driver of AUM growth for the firm, going forward.

In early 2017, Gray launched the firm’s first perpetual vehicle aimed at individual investors, the Blackstone Real Estate Trust (BREIT)– a mutual fund-like product for brokers, which had $2,500 minimums, and charged a 1.25% advisory fee, a 12.5% performance fee, and a hurdle rate of five percent.

The product was an immediate success in the broker channel, who often tacked on an additional sales charge.

According to Schwarzman,

We’ll have a series of these new products all the time. The distributors have, like, 2% in alternatives, and they want to get their customer base to 10% to 15%. So it’s another one of these explosive potential growth areas where we’re positioned as the number one firm in the world.

The success of BREIT would lead to the 2021 launch of the Blackstone Private Credit Fund.

Not to suggest all the kinks have been worked out in this new, retail-facing product line (i.e., the redemption issues with BREIT)…

But the very existence of these products is a watershed moment for two reasons…

- It dramatically expands retail access to private capital strategies (both for better and worse)

- The perpetual capital structure allows Blackstone to change from the traditional “buy-to-sell” model, to a longer term “buy-and-build”

While we won’t suggest the corporate-raiding leveraged buyouts that made private equity infamous are dead and dusted…

We will suggest that this could mark the beginning of a new era in private equity ownership – for better, or for worse.

Blackstone’s “Virtuous Cycle” Thesis

To reiterate the point made earlier, Blackstone does not appear to publish the traditional market outlooks and analyst reports other firms do.

From the firm’s website, we know they are all about the energy transition, life sciences, and artificial intelligence (especially AI data centers).

However, we have to piece together some of the details surrounding these ideas, based on a patchwork of sources.

We’ll start with what appears to be a new publication from Blackstone called “The Connection,” published on January 30th, 2024.

Let’s start with their “Virtuous Cycle” macro outlook:

Past the economy’s landing and the last of the COVID-19 distortions, towards the end of 2024 we expect an economy that is structurally different, having fully recovered from the post-GFC challenges.

And we think there will be a lot for policymakers and investors to like:

Labor markets that are tighter on average over the cycle; investment demand from undersupplied sectors such as housing and energy; investment demand for new areas such as onshoring, the energy transition, and the AI-driven digital economy; and a financial sector bolstered by the structural adjustments required after the financial crisis.

This combination is likely to lead to a much more accelerated recovery from any slowdown in economic growth than the tepid pace experienced after the GFC.

The next cycle is also likely to come with higher interest rates and inflation on average. We expect inflation over the next cycle to run higher than the previous cycle’s average of 1.7%.

While this environment might be less conducive to multiple expansion than the last cycle, it should be a good environment for nominal growth supporting nominal wages and profits.

This growth should drive more durable returns than when multiple expansion simply frontloads future returns, like in the last cycle.

In the real economy, higher investment should support longer term productivity growth, making wage gains more durable as well.

Add it all up, and we believe that the economy could be entering a virtuous cycle where high levels of labor participation, investment and productivity growth sustain each other.

That is exactly the opposite of where we were in the early 2010s and reflects 15 years of improving household balance sheets, a re-regulated financial system, years of underinvestment now driving a catch-up CapEx cycle, and a changed technological landscape.

The implications of these shifts will be the characteristics of the next cycle: massive investment across key industries, higher and more volatile inflation as the global economy fragments, and greater power for workers.

These are characteristics of a more normal, healthier economy that features the type of investment spending that is required to generate wealth over the longer term.

In this scenario, we would expect the real economy to outperform the financial economy.

I’ll unpack all of this in just a moment, but before I do, there are two points I’d like to make first:

- When you’re a firm as large as Blackstone, in many ways, you are “the market,” and represent the consensus view

- Logically speaking, asset managers are going to “talk their book,” and put forward viewpoints that support their way of doing business.

For this reason, it should come as no surprise to hear active managers explaining why passive investing is “dead,” and why you should pay for active managers…

Or that the world’s largest alternative asset managers think it’s a great time to invest in alternatives.

With that said, I think the overall thesis regarding the “real economy” diverging from the “financial economy,” is an important one.

If you really think about it, over the last 10-15 years, “asset light” tech firms were all the rage.

But as we covered briefly in the most recent Weekend Edition… it appears investors might be growing tired of the AI-narrative pushing the Magnificent Seven stocks to new highs, and otherwise driving the broader market.

Why? Because there’s simply no ignoring the sheer amount of infrastructure that needs to be built over the next 10-20 years to support the 4th Industrial Revolution narrative.

And now that the Era of Easy Money is over (for now at least), we’re seeing a return to something that resembles “normal” finance – a focus on cash flows and profit growth.

According to Blackstone,

Private assets are well suited for this type of environment.

We believe that private assets are best incorporated as a permanent part of a strategic asset allocation rather than as a tool for more tactical asset allocation. Liquidity for private assets is lower, which makes it harder to shift weights tactically.

Also, cyclical price shifts tend to be more extreme in public markets, and thus are better captured with changes to public market exposures.

Where private markets excel is gradual accumulation and growth of cash flows, a feature best harvested through a strategic allocation.

For this reason, the firm is focused on “high-quality businesses that are growing faster than inflation or GDP, which supports the earnings growth that is critical to driving attractive returns in this environment.”

And of course, Blackstone – like everyone else – is taking potshots at the 60/40 portfolio, touting the benefits of “Just Add Alts!”

We’ve talked plenty about Private Equity and Private Real Estate in previous issues of Private Capital Insider.

But we haven’t talked much about the current “it girl” asset class – Private Credit.

According to Blackstone’s November 16th article, “Private Credit, Meet ‘Higher for Longer,’”

Market forces of supply and demand are aligning for private credit. Tighter lending conditions and the aftermath of Silicon Valley Bank’s (SVB) collapse caused traditional lenders to step back.

With slower bank and leveraged loan growth, demand for partners in private credit is high.

Private credit provided 65% of loans for the leveraged buyout (LBO) market in 2021 and 86% for the market as of year to date 2023.

The private market offers transaction speed and certainty, allowing lenders to provide liquidity at the most senior portion of the capital structure with favorable covenants for investors.

In addition to the tailwind provided by today’s market environment is the increase in diversification that has historically resulted from adding private credit to a 60/40 portfolio.

From 2015 to 2023, a portfolio that added a 20% allocation to private credit reduced volatility, increased annualized returns, and added 140 basis points of income.

I promised an unpacking, so let’s get started.

The first thing we need to address is how the problems we’re seeing unfold in the banking sector – namely, rising interest rates causing lending to tighten – are pushing borrowers into the vastly less regulated private, non-bank lending sector.

We can debate whether or not this is a good thing, but it’s pretty obvious it’s happening.

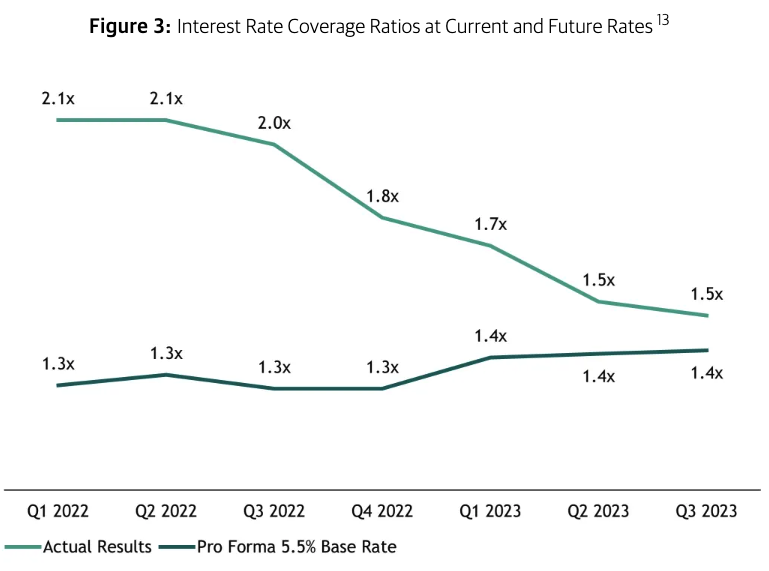

The second thing we need to discuss is a corporation’s ability to service debt – called the Interest Coverage Ratio (ICR).

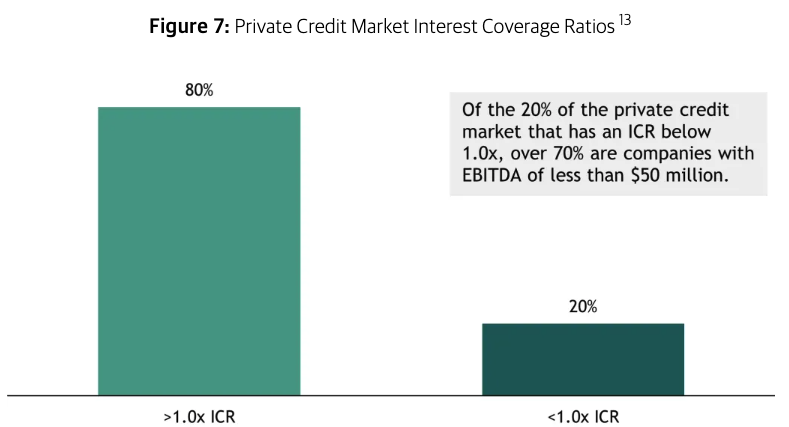

Today, the private credit market operates at a current average ICR of 1.5x, although 17% of companies operate at an ICR below 1.0x when assuming current base rates.

While higher interest rates offer investors the prospect of higher yields, they also put pressure on the borrowers.

As the higher-for-longer rate environment continues, this means we will likely see an increase in defaults down the line.

- Today, nearly 20% of the private credit market has an ICR below 1.0x at 5.5% forward base rates, which implies that nearly 20% of the private credit market does not have sufficient cash flow to cover their debt.

- Of that 20%, over 70% are companies with $50 million in EBITDA or less. As the pressure of higher rates does build, it will likely be felt first and most acutely by smaller businesses.

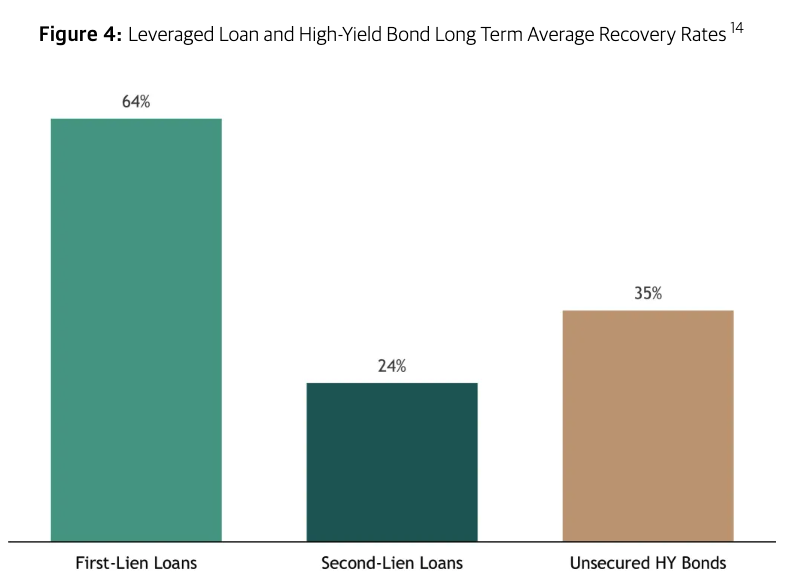

And this brings us to the third thing we need to address, which is the key talking point regarding private credit across the industry – the favorable (senior) position on the capital stack.

Why? Because if a company defaults – or otherwise is forced into liquidation – there is an order to who gets paid first, and how much.

When investments underperform, the most senior capital sees materially higher recoveries than capital lower in the stack.

This is evident in the liquid credit markets, where first-lien loans exhibited a 64% recovery rate vs. 24% for second-lien loans, and 35% for unsecured high yield bonds.

Final Thoughts: A New Era of Alternatives

While I do my best to stay away from making predictions, this ongoing deep dive into the largest alternative asset managers continues to reinforce my assumptions…

Retail Investors are the final frontier of capital.

This means we’re likely going to see more asset managers launch more perpetual vehicles…

And if you’re working with a financial advisor, you’re probably going to start hearing more about why the 60/40 Rule is dead, and instead, the “Just Add Alts!” narrative.

However, just because you now have access to a wider selection of alternative investments, doesn’t mean you will necessarily see meaningful after fee/tax performance in your portfolio.

Before you let your advisor talk you into a fully loaded product with all kinds of fees, be sure to ask questions about the impact of those fees on your potential returns.