With gold continuing to shine at a current spot price of around ~$2,000 an ounce, the worldwide gold industry is worth an estimated approximately $14.7 trillion.

This towering figure is supported by the extraction of about 208,874 tonnes of the precious metal throughout human history, much of it mined in the recent decades.

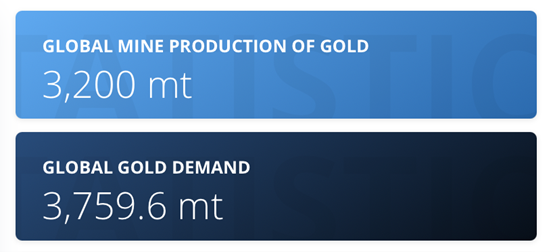

However, the economic equation of physical gold is rapidly changing; demand is outpacing supply, leaving an annual shortfall of 500 metric tons. This is one of the top reasons to invest in gold—as this dynamic points towards a potential increase in gold prices in the foreseeable future.

An annual 500 metric-ton shortfall is unsustainable, and will likely put upward pressure on gold prices for the foreseeable future. Source: Statista

Given these market conditions, you might be wondering what the best gold to buy is (from owning physical gold to investing in gold ETFs). In our view, gold mining stocks present as an intriguing opportunity for investors seeking exposure to the upside potential of gold.

These stocks, particularly those from junior gold miners, could potentially provide extraordinary gains if the yellow metal prices go on a bull run. However, they come with their own set of risks. The volatility of many gold stocks is higher than most investors can stomach.

In this article, we delve into the workings of the gold mining industry, the intricacies of valuing gold mining stocks, and present four of the best gold stocks.

Key Takeaways:

- Gold mining industry: Gold mining is a global $392 billion business with the single largest gold mine in the world located in the State of Nevada.

- The Lassonde Curve: A model of the life of a mining company – from exploration to production – and helps investors gauge market value through each stage of the process.

- Investing in Gold mining stocks: One of the main reasons investors are buying gold stocks is the chance to get higher leverage on the price movements of gold. Assuming the mine is producing, it typically offers a steady stream of cash flow.

- Gold mining stock valuation: Gold mining stocks are mainly valued by their Price to Net Asset Value (P/NAV). Net Asset Value (NAV) is a financial term used to measure the value of a company’s assets minus its liabilities.

- Undervalued gold mining stocks: Gold mining stocks typically trade at half the valuation levels of other industrial companies, despite having a superior return on invested capital (ROIC).

The Global Gold Mining Industry

Gold mining is a global $392 billion business with operations on every continent, except Antarctica. The yellow metal is extracted from mines of widely varying types and scale.

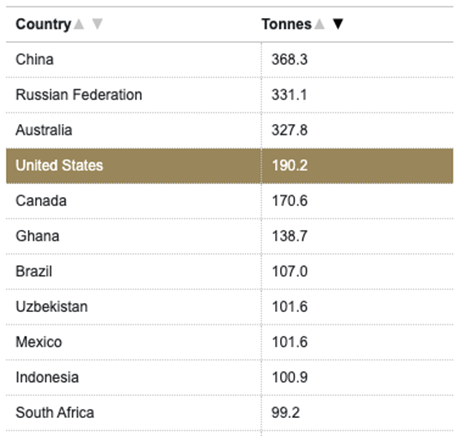

At a country level, China was the largest producer in the world in 2020 accounting for around 11% of total global production.

Global mine production by country. Source: Gold.org

With growing geopolitical tensions with the Russia/Ukraine conflict – along with China’s near monopoly on rare earth minerals – it’s a growing possibility that global supply chains for metals goes through a period of instability.

For this reason, we could potentially see new trading arrangements in the North American continent; combined, the United States, Canada, and Mexico produced ~461 tons in 2020, making it the largest single block of gold producers in the world.

At the time of publishing, the single largest gold mine in the world is located in the State of Nevada.

The world’s biggest gold mines by country. Source: Statista

Mergers and Acquisitions in the Gold Mining Industry

Major gold producers look to grow and expand in different ways.

While many favor organic growth by financing exploration endeavors, this can be a risky and expensive venture; in practice, this means junior mining companies take the extraordinary risks to prove out new mineral deposits and then sell the asset to a producer.

In the same way large tech companies seek to purchase innovative startups instead of funding innovation in-house, Majors often rely on mergers and acquisitions (M&A) to expand their asset base.

Additionally, there are cases where M&A also leads to metal diversification, as the acquired/merged mines contain mineral by-products.

Ultimately, the goal of M&A is to add value by increasing revenue and extend a portfolio’s mine-life – particularly in high price environments.

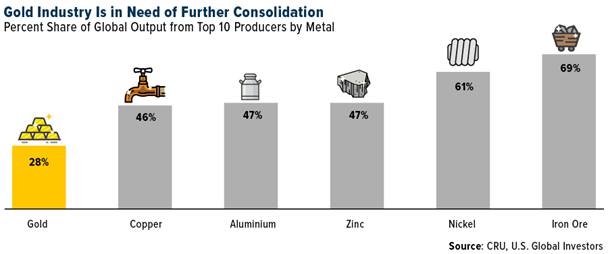

Today, gold is one of the most fragmented mining industries and is ripe for continued consolidation.

The chart below, courtesy of metals and mining consultancy firm CRU Group, shows the global share of output from each metal’s top 10 producers.

The gold industry could be in need of further consolidation. Source: CRU, US Global Investors

Gold is at the bottom, with its top 10 producers responsible for only 28% of global output – of which the top 4 producers account for nearly 20% of global output.

By comparison, the top 10 iron ore producers generate nearly 70% of the world’s supply.

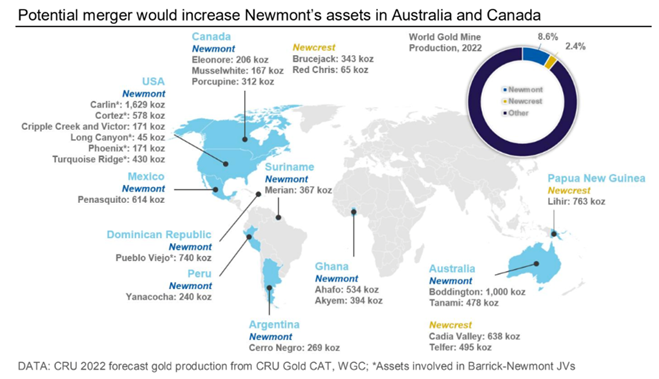

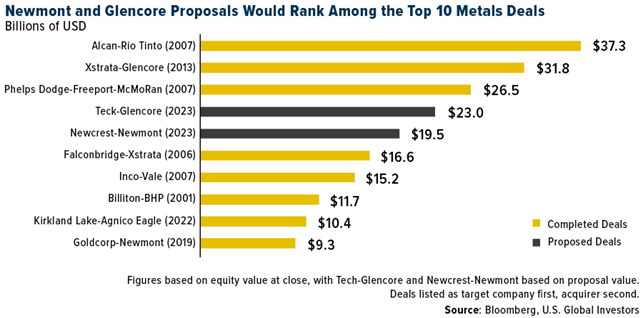

In 2019, many analysts and market participants heralded Newmont and Goldcorp’s $9.3bn merger as the beginning of a new era of gold consolidation.

This sentiment has been amplified with the pending $17bn Newmont-Newcrest deal that would create a gold mining company with global reach that includes 23 mines in 10 countries.

If successful, it would represent one of the top 10 metals deals ever completed, and could serve as a catalyst for continuing consolidation.

We see a market poised for further consolidation ahead as elevated gold prices serve as a backstop for dealmaking activity.

How Gold Mining Works

There are core differences between gold mining and other resource extraction industries.

Oil, in particular, is a high risk/high reward, often binary process: An oil driller either hits a gusher or they don’t.

Mining metals – like gold – is a more iterative process, averaging 10 to 20 years before potential mines start producing refinable ore.

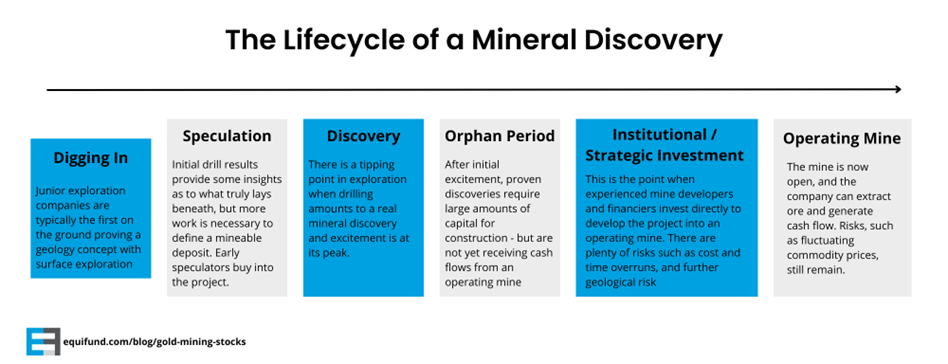

Thirty years ago, Pierre Lassonde – a founder of Franco-Nevada, the first gold royalty company – created his famed Lassonde Curve.

The Lassonde Curve models the life of a mining company – from exploration to production – and helps investors gauge market value through each stage of the process. This helps speculative investors understand the mining process and how value is created.

The lifecycle of a mineral discovery

Beyond precious metals, the Lassonde Curve has become a staple across the mining industry, where mining tends to follow the same 7-step process.

1) Concept:

At this point, the deposit isn’t much more than theory. Geologists work to test the theory, locating the deposit – if any. The area is surveyed, using geochemical and sampling technology. When confident the area might be mined profitably, they move to the next step.

2) Pre-Discovery:

Here, speculative excitement can begin. Geologists coordinate test drilling to establish mineral potentials in the deposit area. The key method is taking below-ground cross-sections (drill core), and having them analyzed for mineral content. Drill cores with good mineral content can lead to further exploration, aimed at the discovery of a mineable deposit.

3) Discovery:

When exploration reveals “enough” mineable minerals, new studies are produced to indicate if mining could be profitable. This changes the business model creating new challenges, such as profitability, construction, and financing.

4) Feasibility:

Having demonstrated the deposit’s potential, investors then evaluate whether to advance the project. Speculators often pile in invest during this “orphan period” while uncertainties about the project remain, keeping more conservative investors away.

5) Development:

A rare outcome, as most mineral deposits never make it this far. The next step is a production plan for the mine, including raising capital and building a team. Many risks still remain in the form of construction, budget, and timelines.

6) Startup/Production:

An even rarer outcome for a mineral discovery. The company begins processing ore and generating revenue. Analysts continue to re-rate the deposit, seeking additional funds from institutional investors and the general public. Existing investors can choose to exit here or wait for potential increases in revenues and dividends.

7) Depletion:

While a rare few last centuries, most mines are depleted in a matter of decades. As grade levels decline, operations wind down, and the remaining investors seek exits.

As projects are pushed slowly up the value chain through ongoing iterations, this means that:

- Valuations of projects and companies can increase incrementally before actually building working mines.

- Miners can make realistic exploration and drilling budgets, without having to take on too much debt.

Each one of these moments is an opportunity for investors to enter into one of these projects and attempt to capture returns.

Why Invest In Gold Mining Stocks

If you’re wondering why investors buy gold mining stocks specifically (which some of them place inside a gold IRA), it’s because miners offer the chance to get higher leverage on the price movements of gold. Assuming the mine is producing, it typically offers a steady stream of cash flow.

Mining stocks are truly two distinct groups: majors and juniors.

The majors are well-capitalized companies with decades of history, world-spanning operations, and slow and steady cash flow. Major mining companies are no different from large oil companies, and many of the same metrics apply with a mining twist.

Both have proven and probable reserves, except mining companies break down profit and cost on a given deposit by the ton, instead of the barrel. In short, a mining major is easy to evaluate and easy to invest in.

The junior mining stocks are very nearly the exact opposite of mining majors. They tend to have little capital, short histories, and high hopes for huge returns in the future. A junior company is essentially a smaller or newer company that is developing or seeking to develop a natural resource deposit or field.

Although majors and juniors are very different, they are united by the one fact that makes all mining stocks unique: their business model is based on using up all the assets they have in the ground.

However, most majors like to let the junior mining companies take all the risk of finding new deposits. Then, once the juniors have struck gold, they’ll buy the reserves and develop the mine. When new deposits are being found, the “growth through acquisitions” model works well.

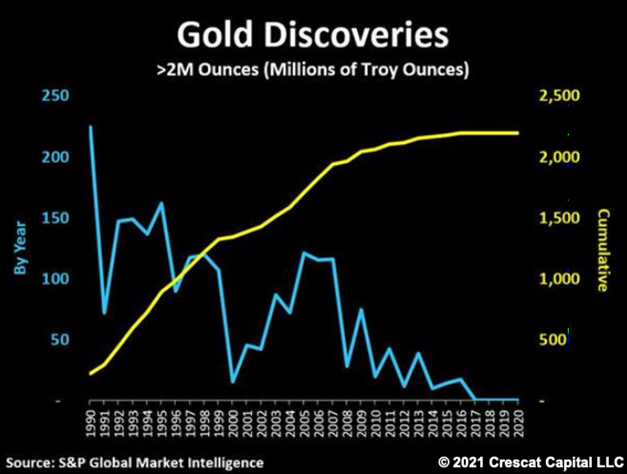

However, for the past 20 years, explorers have failed to find a single deposit above 30 million troy ounces. Over the previous three years, there have been zero gold discoveries above 2 million troy ounces.

Gold discoveries above 2M ounces by year. Source: Crescat Capital

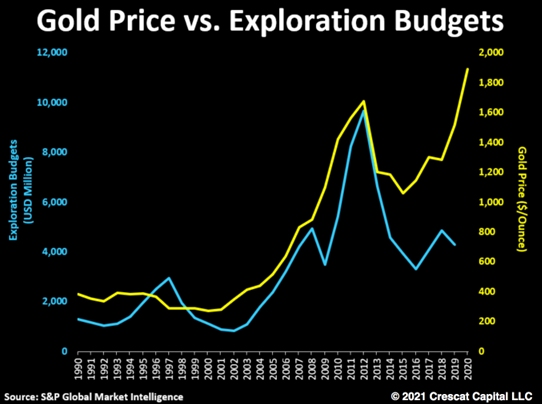

And the markets are noticing; The price of gold has climbed from its January, 2016 low of $1,064/oz to a new all time high of $2,035 in August 2020. After some volatility through 2021/2022, gold has now climbed towards a new ATH and current spot prices are ~$2,000/oz at the time of publishing.

However, despite this increase in gold prices, exploration budgets have been steadily decreasing since 2012.

Gold price versus exploration budgets by year. Source: Crescat Capital

Why? After crashing from 2011 highs to a 2013 low of $1,180, it was too expensive to explore for new deposits. Instead, they focused on mining their existing deposits.

Many gold mining companies – who were overleveraged with bloated cost structures – were forced into dramatic cost-cutting, paying down debt, and often the firing of exploration teams.

As gold prices started to soar in 2020, major gold producers accelerated production of existing resources to take advantage of the higher prices. Today, gold miners are seeing record cash flows and cash reserves.

“Precious metals producers are printing money at a fever pace. You can see that for a decade straight, the industry was a black hole for capital. Now, the sector has strung together multiple massive quarters and bolstered battered balance sheets.” – Marin Katusa

The tradeoff? Miners are exhausting their existing reserves and resources.

The small number of mines that can generate more than 10 million troy ounces – known as world-class deposits – are running dry. And because of this large imbalance of “gold demand” vs “gold supply,” experts and analysts are sounding the alarm…

The world is running out of new gold!

After a decade of disappointing price action in the gold markets, investors are starting to pile back into the yellow metal and prices are starting to rise.

According to S&P Global Market Intelligence (S&P), global exploration budgets rose 16% in 2022, following a 34% rebound in 2021. S&P added that while allocations for most commodities increased in 2022, budgets for gold and copper posted the largest dollar increases, while energy transition efforts saw lithium increase to its highest total ever.

Risks of Gold Mining Stocks

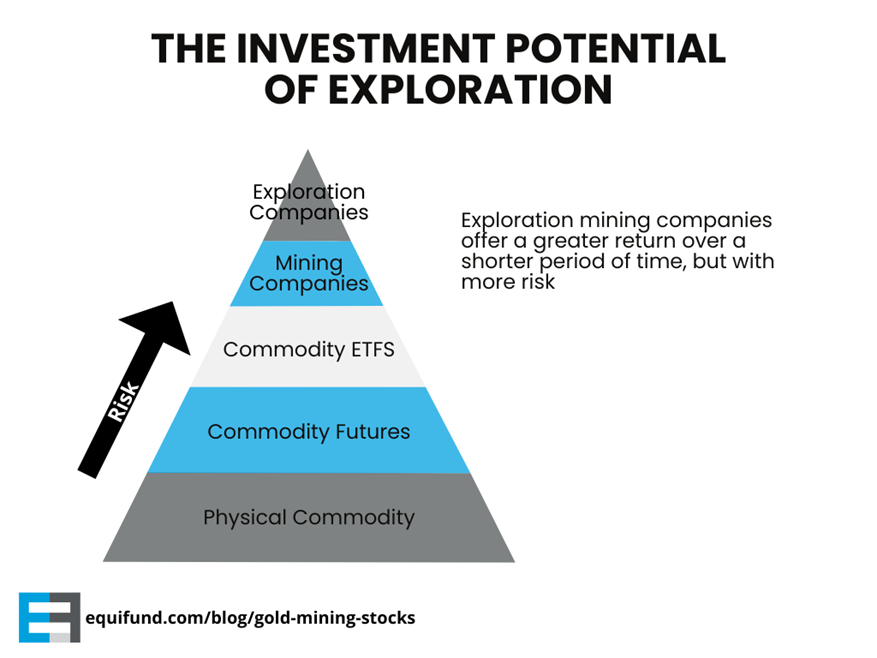

For investors looking to capture huge potential gains from the gold markets, junior gold mining companies provide arguably the highest potential rewards.

However, they also come with extraordinary operational risk. Not only do they have to bear the upfront cost of finding a workable mineral asset, they then have to extract those minerals before they can generate revenue (let alone profit).

Exploration companies are the most high risk play in gold investing.

How Gold Mining Stocks Are Valued

Our curated list of the best gold mining stocks is based on the main valuation method used in the mining industry: Price to Net Asset Value (P/NAV).

Net Asset Value (NAV) is a financial term used to measure the value of a company’s assets minus its liabilities. The NAV represents the amount you would receive if a company liquidated all its assets after paying off all its liabilities.

According to the Corporate Finance Institute:

P/NAV is the most important mining valuation metric, period.

“Net asset value” is the net present value (NPV) or discounted cash flow (DCF) value of all the future cash flow of the mining asset, [minus] any debt plus any cash.

The model can be forecast to the end of the mine life and discounted back today because the technical reports have a very detailed Life of Mine plan (LOM).

The formula is as follows: P/NAV = Market Capitalization / [NPV of all Mining Assets – Net Debt]) ]

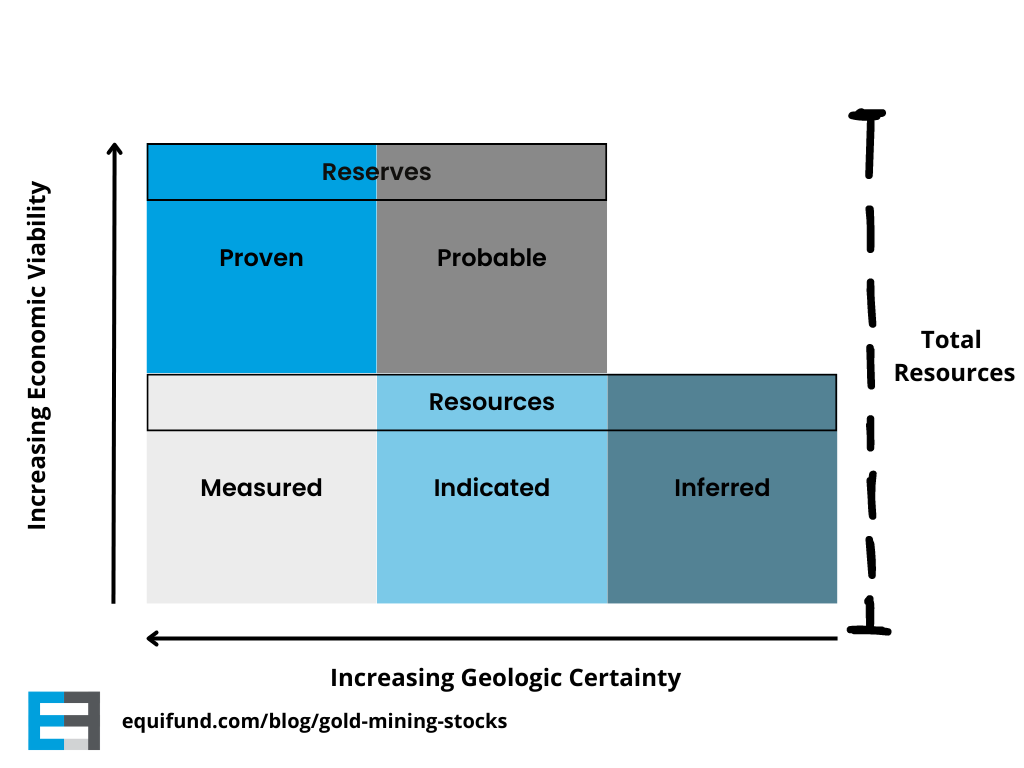

This means that the value of any mining company or gold stock is based on the total P/NAV of all the assets it controls. This means as Reserves and Resources are depleted, the value of the asset – along with its potential for future cash flows – decreases.

How the economic viability of gold mines are determined. Source: Corporate Finance Institute

However, if the Reserves and Resources can be increased – either because more mineral deposits are discovered, or advances in technology/mineral prices make previously unrecoverable minerals feasible to mine – the value of the asset increases.

For investors, this presents an interesting opportunity to potentially acquire mining assets that are typically undervalued, relative to their peers in the industrial sector.

Why Gold Mining Stocks Could Be Undervalued

For years now, the stock market hasn’t been kind to value investors in search of a discount…

With one notable exception: mining stocks.

Gold mining stocks compared to gold prices. Source Incrementum.

Investing in the stocks of companies that trade below their book value—the accounting value of assets such as factories, inventory, and real estate, minus liabilities—is a strategy first popularized by Ben Graham in the 1930s.

But few companies of any significant size trade below book value today.

Consequently, Barbee’s stocks are often the smallest, most overlooked ones that big institutional investors ignore.

The bulk of his portfolio is currently in mining, energy, and timber stocks—companies with plenty of hard assets.

Barbee likes miners with “hidden assets” … as they can have what he calls asymmetric returns relative to the price of gold bullion—more upside and hopefully less down as the market eventually recognizes the hidden value.

For reference, we at Equifund first started studying the mining industry back in ~2021 when we launched a Regulation Crowdfunding offering for Durango Gold – which, based on our knowledge, was the very first junior mining company to do so.

Prior to this, we most certainly were not gold bulls, nor fans of junior mining deals. But once we started to get past the dense technical jargon about mineral deposits, the economic case for “why mining” in general, became pretty clear.

According to a 2020 interview with Chris Berkouwer, equity analyst for Robeco:

No miner is the same, but even those that have little coal exposure are greatly unloved by investors: they trade at half the valuation levels of other industrial companies, despite having a superior return on invested capital (ROIC), 35% higher dividends and generate one and a half times more free cash flow.

Even though the big global miners outperform the general market on just about every financial metric, the MSCI Metals and Mining Index has significantly underperformed for many years. It seems like there is always a stick to beat a miner with.

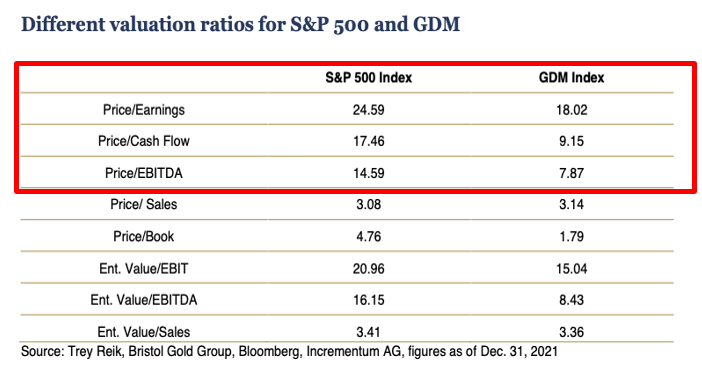

While we initially dismissed this as investors simply preferring tech stocks hype – and at the time, valuing growth more than cash flow – we found more confirmation of this pricing anomaly (chart below shows data as of Dec 31, 2021).

We’re seeing different valuation ratios for S&P and GDM stocks.

According to a 2022 interview with Mitchell Krebs, President & CEO of Coeur Mining…

“There is currently a disconnect between where metals prices are and how mining company share prices are trading, and I believe there are a few explanations.

First, the broader economy has seen such a bull market that investors continue to chase returns elsewhere.

Second, there is a lack of conviction among investors in the sustainability of these prices.

Third, there is a larger question of relevance from the perspective of investors seeking exposure to precious metals.”

At the time, we believed that if our macroeconomic thesis regarding the importance of domestic mineral production was correct, we could see these historically undervalued assets appreciate in the coming years ahead.

Chart shows the performance of mining stocks (XAU) relative to equity markets (S&P 500). Source: incrementum, In Gold We Trust: 2022

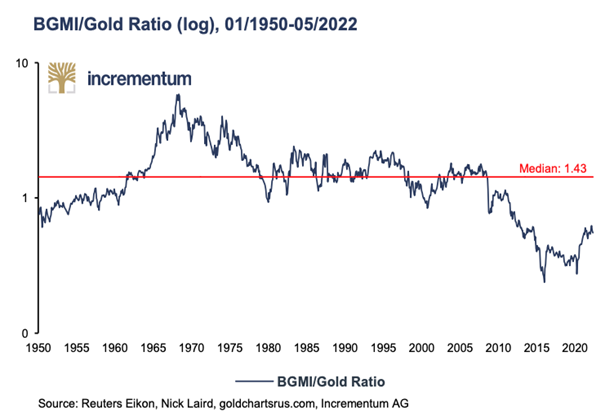

This underperformance of mining stocks becomes particularly clear if we make an even longer-term comparison. The oldest available gold mining index, the Barron’s Gold Mining Index (BGMI); at the time, it was trading at 0.50x, miles below the long-term median of 1.43x.

Price performance of BGMI. Source Incrementum.

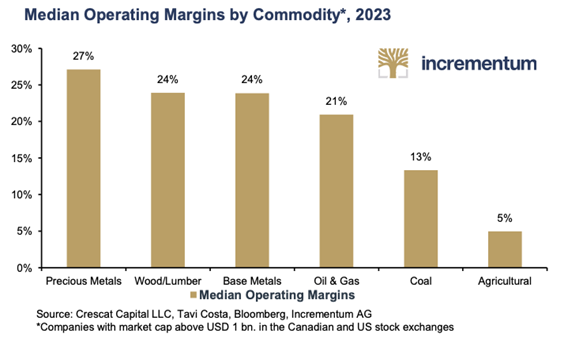

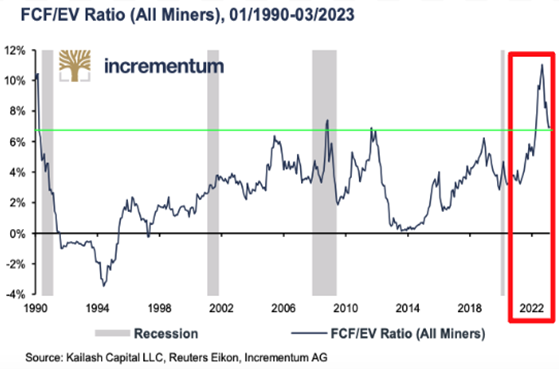

Furthermore, in an economic environment where cash flow is king – and commodities are booming – there’s simply no ignoring the facts; within the commodities sector, no other subsector is currently showing higher margins than precious metals producers.

Median operating margins by commodity. Source Incrementum.

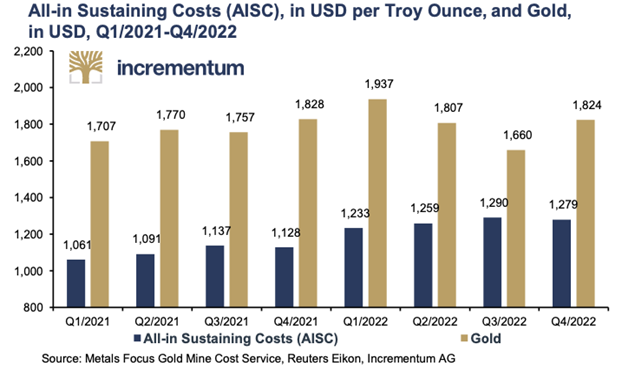

The global all-in-sustaining costs (AISC) of gold producers increased in the previous year, in line with general inflation.

According to the World Gold Council, AISC was $1,007 in Q4/2020, and a year later they were at $1,129, an increase of 12.2%. In 2022, AISC reached a new high of $1,276 per ounce, an 18% increase.

All-in sustaining costs in USD per troy ounce. Source Incrementum.

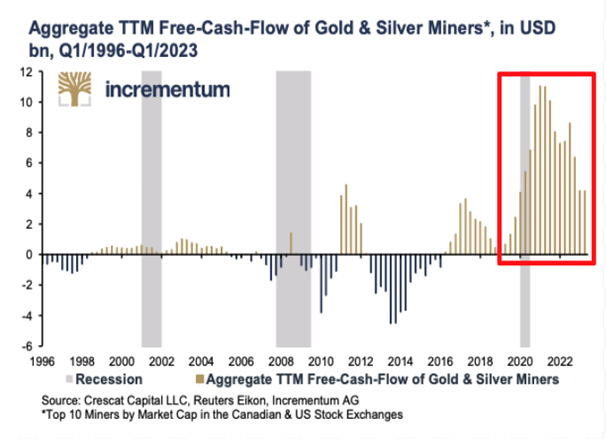

The Commodity sector as a whole generated negative free cash flows in 2012–2016. Even after that, free cash flow was marginal, and limited to low-cost companies; but by spring 2021 at the latest, gold and silver miners became true cash flow monsters.

In 2022, profitability suffered from high inflation, yet total free cash flow was around $24 billion.

Free Cash Flow of Gold & Silver Miners. Source Incrementum.

We’ve said this before and we’ll say it again. The secret to outperformance is to be both contrarian and right.

But eventually, if you want to sell your position for a profit, the market needs to agree with you and value it accordingly.

Even though we had a brief window of enthusiasm for miners, it doesn’t seem the market believes the bull market thesis and continues to discount miners.

Free Cash Flow of Gold & Silver Miners. Source Incrementum.

But what makes this even more interesting is the clear trend towards increased M&A activity and industry consolidation.

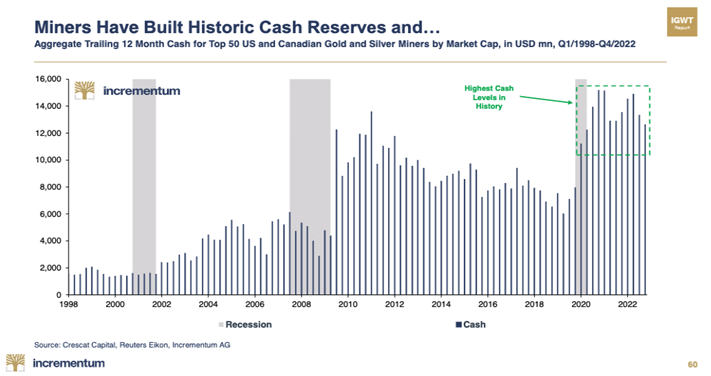

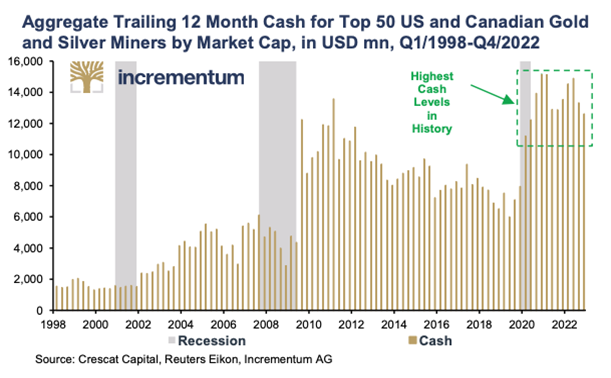

Although the gold price has been trading close to new all-time highs, and miners have the highest cash levels in history…

Cash reserves of the top 50 US and Canadian gold and silver miners. Source Incrementum.

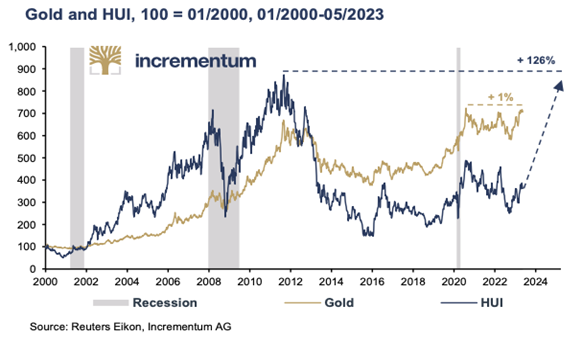

The HUI Gold Index – a modified equal dollar-weighted index of gold mining companies – is trading more than 50% below its all-time high of 635 in September 2011.

Gold and HUI. Source Incrementum.

No promises, but this could potentially represent an asymmetric payoff profile if investors decide to “reprice” mining stocks.

More specifically, these prices could appear if the M&A cycle heats up.

“We expect that producers’ bubbling cash flows will lead them to replenish their shrinking reserves through acquisitions and mergers.

The biggest beneficiaries of this development will be junior producers, fully funded developers, and explorers with world-class discoveries in Tier 1 regions.”

Investors in exploration companies should realize that a major mining company, considering the buyout of a junior, is much less likely to be interested if the land package is an unconsolidated mix of patented and unpatented mining claims.

That also means that some of the more interesting projects today have been underexplored due to fragmented claim status and a lack of historical data.

“Consolidation is the key to unlocking shareholder value in a mineral land package.

[Majors] seem to lose interest fairly quickly because if the ground is not consolidated, then they’re limited on where they can explore.

The bigger companies especially don’t like to spend a lot of time and money negotiating deals with people and consolidating it themselves.

And the consolidation of the historic data is also a key to increasing the value of a project”

Depending on where the claims are, differing ownership can become troublesome for exploration companies wanting to develop consolidated land packages; especially when the goal is to sell the complete package to a major mining company following value-added exploration on the properties.

And to this end, we see enormous opportunity in the State of Nevada.

Want to learn more about investing in gold and private market deals?

Here at Equifund, we help investors access early-stage opportunities not found anywhere else. To view our current listings, go here now.

P.S. Equifund just launched its latest Regulation A+ offering for an already-publicly-traded gold royalty and streaming company.