If you’ve found yourself fretting over the volatility of the stock market or the unpredictable future of the US dollar, you’re not alone. This economic uncertainty has many investors searching for a financial safe haven – for thousands of years, that asset has been gold.

Gold, an asset with a history as old as civilization itself, has a unique investment appeal. Long considered a hedge against inflation, the yellow metal is the only form of money that has no counterparty risk. It’s convertible into any currency, at any time, anywhere in the world. Not to mention, it’s a proven store of value as the metal never degrades or corrodes.

But for investors who are interested in owning gold, there’s a crucial decision to make: do you buy physical gold or paper gold?

If you’re simply looking to bet on the price action of gold, short term trading is best left to paper gold products. But if you’re looking to put your money in the world’s most popular safe haven asset, there is no substitute for owning physical gold and having it in your possession.

Fortunately for you, there’s also a hybrid option. Thanks to IRS code 408, you can now use money inside your retirement accounts – like your IRA or 401k – to invest directly in physical gold. It’s commonly called a Gold IRA.

Now before you go trading your dollars for doubloons, you should carefully analyze whether this option is worth it for you given the IRS rules and regulations around gold investing plus the relatively high custodian fees involved in adding gold to your IRA.

In this article, we’ll sift through the key factors you should consider when investing in gold, be it physically or through a Gold IRA. We’ll highlight the pros and cons, detail the tax benefits and regulations, and explain what goes into purchasing and managing both physical gold and Gold IRAs.

Key Takeaways:

- Physical Gold: Buying gold in its tangible forms (e.g. coins, gold bars, pure nuggets, jewelry). The scarcity and practical utility of gold has made it a store of value for centuries.

- Gold IRA: A self-directed IRA that allows investors to invest in gold and other precious metals (e.g. silver, platinum, palladium).

- Gold IRA costs: A Gold IRA may come with higher fees than a traditional IRA, which may reduce your potential returns.

- Gold IRA rules: The IRS has a number of rules governing the type of gold you can invest in, the process of setting up your Gold IRA as well as required minimum distributions.

Physical Gold Investing

Investing in physical gold is a strategy where you acquire gold in its tangible forms, which can range from pure nuggets to jewelry, and from collectible coins to gold bars. In fact, for those seriously considering this investment route, gold bars or bullions typically provide the best opportunity to maximize your return. This is due to their high purity, ease of storage, and the relative ease of finding a buyer when it’s time to sell.

However, before you dive into this investment, there are a handful of things you need to be aware of.

Why is Gold Valuable?

For thousands of years, gold has captured the imagination of humans across the globe… and ruled the monetary affairs of modern civilizations.

Before the 20th century it was “the governor” of trade, prices and humanity’s most valued monetary asset. Today, purely digital money reigns supreme. Major currencies like the dollar and euro are increasingly abstract; the vast majority of “our money” exists as purely digital information on commercial bank server farms.

But the speed and agility of “digital money” brings unseen danger: long term instability and the threat of systemic collapse.

While we won’t speculate on a near-term collapse of the modern monetary system, gold’s undying and near-universal appeal is for one reason; Because gold is essentially indestructible by conventional means, it has historically been the best way to store value across generations.

As a result, humans have believed – for thousands of years – that other humans will predictably and reliably value gold over other, less durable assets.

This persistent belief in gold is, in essence, no different than a religion. And if the Lindy Effect – which states that the older something is, the more likely it will be around in the future – is any indication… gold will continue to remain a reliable store of value.

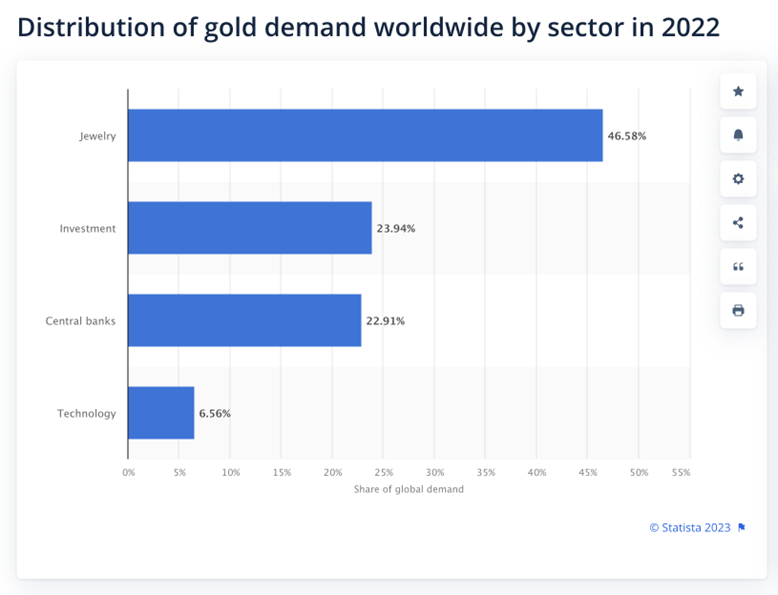

Gold’s brilliant luster, unmatched durability, and resistance to tarnishing also make it ideal for jewelry and ornamentation. Given these unique properties, it’s unsurprising that almost 50% of gold is used in the manufacture of jewelry. But the yellow metal is also used in various other industries, including Technology (~7%) and Investment ~24%).

Not to mention, Central banks worldwide (particularly the US and Germany) are the largest holders of gold bullion in the world. They are stocking up on gold to lessen their dependence on U.S. dollars as a reserve asset, and this trend is likely to continue—positively impacting the demand for gold.

Gold demand worldwide by sector in 2022. Source: Statista

How Physical Gold Investing Works

Investing in physical gold typically involves purchasing gold in either coin or bar form. The price you pay consists of the per-ounce price of gold plus a slight markup by the seller. Bars, for instance, range from one gram to 400 ounces, and because they aren’t minted, they have a lower markup. Affluent investors often prefer larger bars as it’s more convenient than holding numerous coins.

On the other hand, gold coins are both easily recognizable and portable, which can make them simpler to sell privately. Popular bullion coins include the American Eagle, Canadian Maple Leaf, and South African Krugerrand. Sizes typically range from one-tenth to one-ounce coins, with the smaller denominations costing more on a per-ounce basis. You can purchase these coins from local shops or national dealers like Bullion By Post and APMEX.

Bullion coins are one category, their value derived solely from their metal content. Then there are numismatic coins, which are collectible and derive their value primarily from their rarity. For instance, pre-1933 U.S. gold coins have become rare due to government recall and melting—significantly increasing their numismatic value. Certain rare gold coins can even be worth hundreds of times more than their gold bullion value.

While jewelry is another way to own gold, especially in developing countries, it’s important to remember that it doesn’t usually offer real investment value. A majority of U.S.-made jewelry is 14 karat, meaning it’s about 60% gold and the rest is alloys. Plus, the fabrication costs are high. For example, a piece of jewelry might be priced at $1,000 but only contains $100 worth of gold.

Gold Investing Benefits

Gold has a number of unique benefits that can make it a compelling investment choice, particularly during uncertain times.

For many investors, there is simply “no gold like gold.”

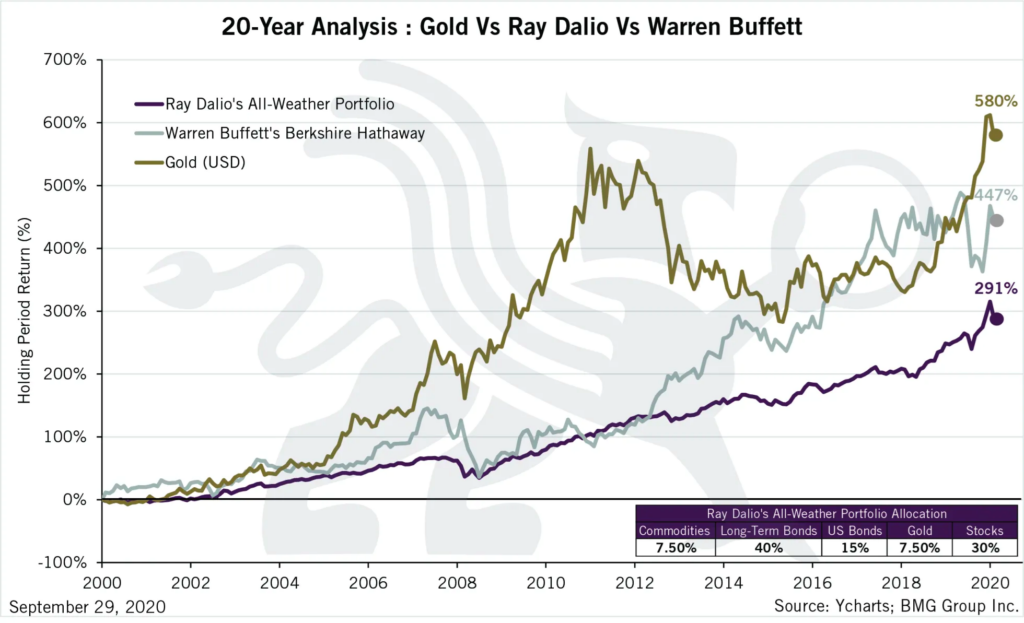

Even Warren Buffet – after decades of bashing gold – trimmed several of his banking positions in 2021 in favor of gold mining company, Barrick Gold Corp.

Perhaps it had something to do with gold outperforming Berkshire Hathaway – and Ray Dalio’s famous “all weather portfolio” – for the previous 20 years…

Maybe it has something to do with the fact that central banks – and the world’s wealthiest families – have been quietly stockpiling gold since the 08/09 financial crisis.

Long-term growth potential:

For starters, it’s an asset that has demonstrated a significant potential for growth over time. In fact, since 2000, gold’s price has outperformed both Warren Buffet’s Berkshire Hathaway and Ray Dalio’s All-Weather Portfolio by 133% and 289% respectively.

20-year analysis of gold vs Ray Dalio vs Warren Buffet

Resilience during crises:

While it’s worth noting gold doesn’t necessarily move inversely to stock market fluctuations, gold has historically acted as a resilient investment during periods of economic distress.

Back when the Great Financial Crisis was in full swing, gold collapsed by 33% in a matter of months.

The fall of Gold prices during the 2007 financial crisis.

Why did gold prices drop? In our opinion, it was a side effect of the stock market collapsing.

As liquidity dried up and margin calls intensified, investors were forced to raise capital by selling gold. This, in turn, created downward pressure as more people looked to exit and cover their losses.

Then, as the Federal Reserve launches quantitative easing – and American sentiment turns negative – gold prices exploded from $700 to a new all-time-high of $1,923.

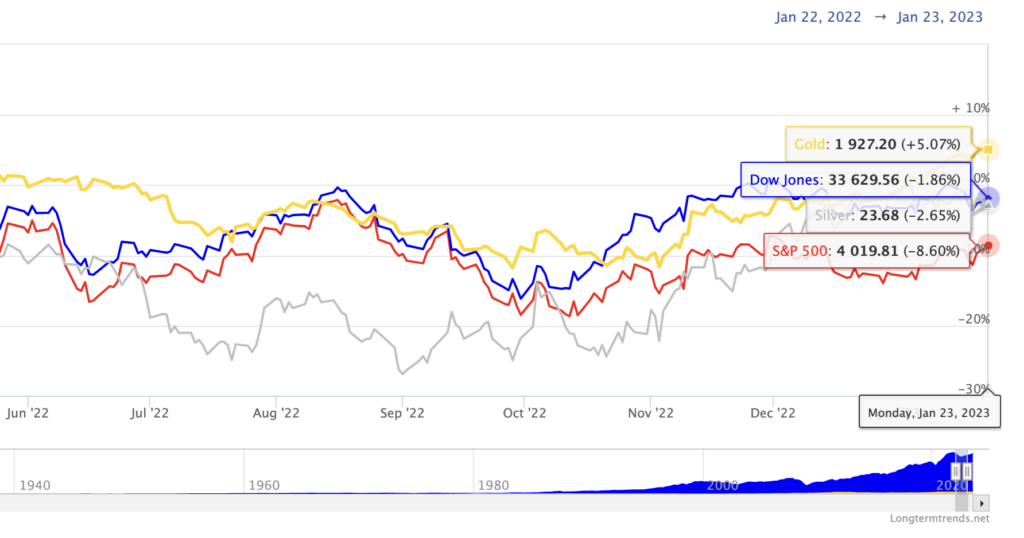

Take, as another example, the recent stock market decline from 2022 to 2023. The stock market lost over 8% of its value, while gold prices experienced an increase of about 5%.

Performance of gold vs S&P 500 between 2022 and 2023. Source: longtermtrends.net

Physical ownership:

Physical gold offers another distinct advantage—the security of possession. Unlike investing in paper assets like stocks and bonds where a third party is involved, owning physical gold gives you complete control over your investment, adding to your peace of mind.

What is the Downside of Investing in Physical Gold?

Investing in physical gold can seem attractive, especially as a tangible asset or a potential hedge against economic uncertainty. However, before going down that path, it’s essential to understand the challenges associated with this type of investment.

Storage costs:

Unless you own a robust safe at home or rent a safe deposit box at a bank, keeping your gold secure from theft or damage could be a major hurdle. Some investors opt for pooled accounts, which store the gold in a vault and assign you either a specific coin or bar (allocated) or simply a record of a gold sum (unallocated).

While allocated accounts provide direct ownership, they come with storage and insurance fees. Unallocated accounts can help save on fees, but if the company holding your gold goes bankrupt, creditors may lay claim to your asset.

Utility during economic collapse:

While gold has historically been viewed as “pure money”, its utility during times of systemic breakdown is questionable. Would people be willing to trade essential survival items for a piece of gold? The answer might not be as straightforward as you’d think.

Price mark ups:

The market price of gold is often marked up at the point of sale, meaning you’re paying a premium to own the physical asset. This could amplify your losses if the value of gold falls.

Lack of tax benefits:

According to the Internal Revenue Service, physical holdings in gold, along with other precious metals like silver, platinum, palladium, and titanium, are considered capital assets—specifically collectibles.

So when you sell physical gold in any form – be it bullion coins, bars, rare coins, or even ingots, the IRS may tax it at a rate of 28%, which is higher than the standard capital gains rate applied to gold stocks.

IRS reporting rules:

The IRS has detailed reporting rules for precious metals sales. Compliance with these rules is your responsibility as an investor, and there might be immediate reporting requirements for specific types of gold upon sale.

What is a Gold IRA?

While traditional IRAs mainly allow you to invest in stocks, bonds, or mutual funds, a Gold IRA operates as a self-directed IRA. This essentially means that you, as the investor, have more control and a wider choice when it comes to the types of investments held within the account.

These investments can include gold, but also silver, platinum, and palladium, further diversifying your retirement savings.

How a Gold IRA Works

A Gold IRA operates quite similarly to your traditional or Roth IRA, but instead of investing in stocks and bonds, you’re investing in gold or other precious metals like silver, platinum, and palladium.

To start investing with a Gold IRA, you first need to open a self-directed IRA with a Gold IRA custodian. These entities are approved by federal and/or state agencies to provide asset custody services to investors.

This custodian’s role is to hold and administer your self-directed IRA funds, but they won’t provide financial advice or choose the metal broker on your behalf (this choice is solely yours). However, your custodian may have relationships with several hundred Gold IRA companies countrywide and might be willing to share that list.

Now, here’s where it gets interesting. Because all transactions must be made from the IRA itself – meaning, you can’t buy gold with your personal accounts and then “deposit” that gold into your Gold IRA – usually you are required to submit your gold orders through the custodian’s investment platform (or broker network). This transaction is almost certainly subject to various transaction fees and commissions.

Generally speaking, the Gold IRA company will also be responsible for vaulting and storing the physical gold on your behalf. Vaulting also is subject to certain fees, either a flat fee or a percentage of the total value of the metals.

The Gold IRA company you choose will buy the gold on your behalf, and your Gold IRA custodian will create and administer the account that holds your gold bullion.

Selecting the best Gold IRA company for you involves a variety of factors, including reputation, compliance, fee structures, storage options, and customer support. Keep in mind that conducting thorough due diligence is a critical step in protecting your retirement assets and ensuring a successful Gold IRA investing experience.

Investor Profile

The first step involves determining your investment goals, factoring in elements such as your retirement timeline, risk tolerance, and how much of your portfolio you plan to dedicate to precious metals. Since every investor has unique needs and goals, it’s crucial to choose a Gold IRA company that will cater to you personally rather than applying a one-size-fits-all approach.

How much gold should you have in your portfolio?

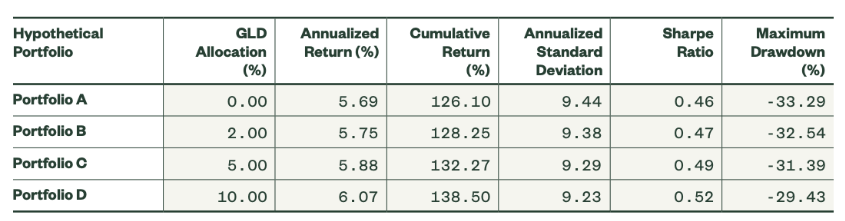

The question of “how much gold should I own” is really more of a question of portfolio construction than anything else. Historically speaking, we can see clear evidence that in previous financial crises, having a 2% to 10% allocation to gold would mean the portfolio had higher annualized returns and lower maximum drawdowns than a portfolio without any exposure to gold.

Hypothetical portfolio performances between January 1, 2005 and September 30, 2019. Source: SSGA

Qualifications:

Make sure the Gold IRA companies you’re looking into are compliant with IRS regulations regarding self-directed IRAs. Check if they are accredited by industry organizations, possess all the required licenses, registrations, insurance, and bonds to protect your retirement funds, and if they work with trustworthy custodians and storage facilities to ensure the security of your precious metals.

Track Record:

It’s also crucial to research each Gold IRA company’s reputation and track record. Prioritize companies that have a history of customer satisfaction, transparent practices, and a steady market presence. For example, you could refer to customer reviews on platforms like the Better Business Bureau or Trustpilot to gain insight into other clients’ experiences and whether there were any complaints filed against the Gold IRA company.

Storage:

You should evaluate the storage options each Gold IRA company offers, such as segregated storage or depository choices, and see if they meet your security standards.

Fees and Costs:

The fees and costs involved in setting up and maintaining a Gold IRA account can vary between companies, so you should compare them carefully. Aim to find a company with transparent fees and avoid those with high or hidden charges that could diminish your returns.

Investor Education & Support:

Evaluate the educational resources and customer support that the company provides. Gold IRA companies should offer comprehensive resources, like guides or webinars, that will help you make informed decisions about your investment. Their customer support should also be responsive and capable of providing assistance when required.

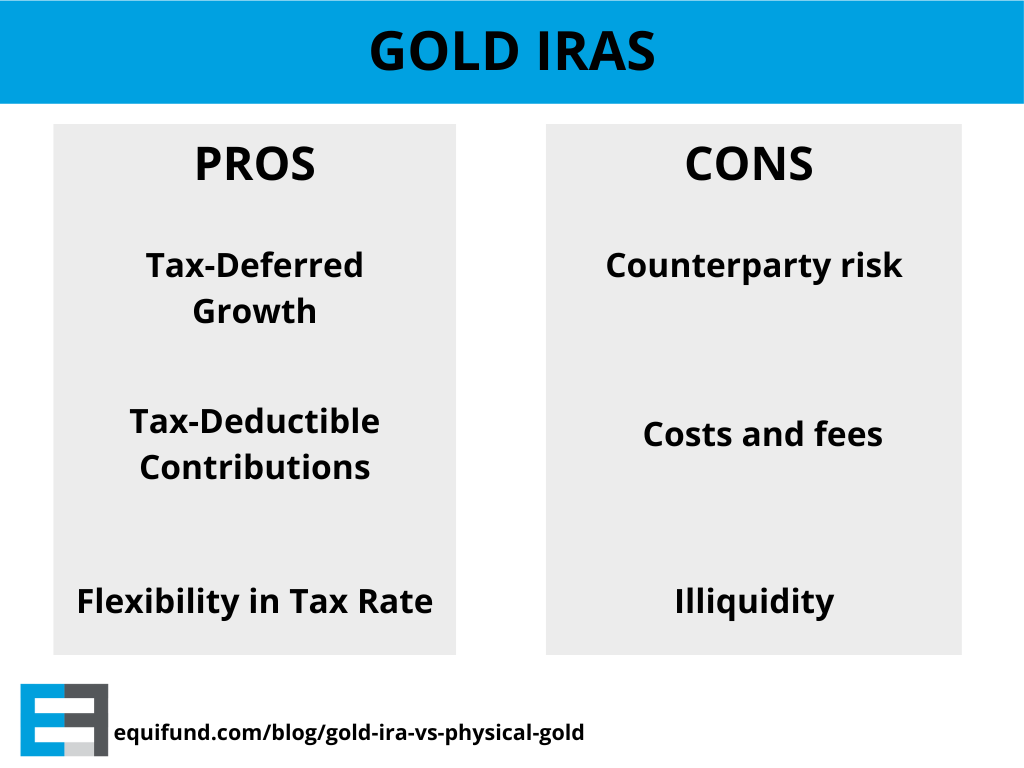

Gold IRA Benefits

There are several reasons why holding gold in your IRA can be advantageous from a tax perspective.

Tax-Deferred Growth:

Simply put, any growth or appreciation of the gold assets in your IRA won’t be taxed as long as it stays within the IRA. This can result in substantial tax savings over the long term.

Let’s take an example here. Suppose you purchase $5,000 worth of gold in your IRA and you end up selling it for $7,000 in a few years. If this were in a regular account, you’d have to pay capital gains tax on the $2,000 gain when you sell it. However, in an IRA, you don’t have to pay this tax until you start withdrawing funds.

Tax-Deductible Contributions:

Traditional IRAs often allow for tax-deductible contributions. If you meet certain income requirements, you can deduct the amount you contribute to your IRA on your income taxes for the year. This reduces your overall taxable income, thereby potentially reducing the amount of income tax you have to pay.

To illustrate, let’s say you’re in the 24% tax bracket and you contribute $6,000 to your traditional IRA. That contribution could reduce your tax bill by $1,440 ($6,000 x 24%).

Flexibility in Tax Rate:

With a traditional IRA, you pay taxes upon withdrawal, typically in retirement. If you anticipate being in a lower tax bracket when you retire compared to your current tax bracket, this could provide further tax savings.

So for instance, if you’re in the 32% tax bracket now and expect to be in a 22% bracket during retirement, you could save 10% in taxes on the withdrawn amounts.

What is the Downside of a Gold IRA?

While a Gold IRA may seem like an attractive option for diversifying your retirement portfolio, potential investors need to understand the numerous complexities and added costs that come with it.

Counterparty risk:

Unlike holding gold directly, which you can use at any time, with a Gold IRA, the gold is in the possession of a custodian. So, if an emergency situation arises where you need to utilize your gold, there is a process to go through with the custodian to access your own asset.

Opening a self-directed IRA:

Moreover, you can’t use standard custodians like Fidelity, Schwab or TD Ameritrade for a Gold IRA. You must establish a self-directed IRA and then find a custodian that specializes in self-directed Gold IRAs. American Bullion and APMEX are two known entities, but you’ll need to perform due diligence to find the right custodian for you.

IRS rules:

Then there’s the tax code stipulation against holding collectibles in an IRA. While certain types of gold coins and bullion are acceptable, others fall into the collectible category and hence violate the rules. It can be challenging for an investor to navigate these rules, as the IRS doesn’t maintain an explicit list of permitted and non-permitted gold types.

Costs and fees:

Setting up and maintaining a Gold IRA involves costs at each step – from purchasing to storing and finally selling the gold. None of these services are free, and these additional expenses raise the break-even point on your gold investment. Fees vary from one custodian to another, some charging a flat fee while others have a rate depending on the invested value.

It’s important to remember that Gold IRAs often have higher maintenance costs than other IRAs due to the physical nature of gold. On top of the usual IRA fees, there may be brokerage fees, shipping costs, storage fees, insurance costs, sales markups, and Gold IRA account closure fees.

Lack of tax advantages:

From a tax perspective, a Gold IRA isn’t as beneficial as other traditional IRAs. While assets like stocks or ETFs generate income and provide tax benefits, physical gold in an IRA doesn’t generate dividends, interest, or capital gains distributions, making no tax savings.

Illiquidity:

Given gold’s nature, finding a buyer without discounting the price can be a challenge, particularly for large sales. Additionally, gold is prone to volatility, with prices that can rise or fall swiftly. When IRA owners reach the mandatory distribution age of 73, they might be compelled to sell gold at a less favorable price.

Gold IRA Rules

The IRS has a number of rules governing the type of gold you can invest in as well as the process of setting up your Gold IRA.

The first rule to consider is related to the type of gold you can include in your IRA. It must meet certain purity standards – specifically, it must be at least 99.5% pure, or .995 fine. This ensures that you’re investing in high-quality gold.

The IRS also mandates that the gold must be recognized as legal tender, either in coin or bar form. In simple terms, this means that the gold must have been minted by a government and carries a designated face value. For instance, the American Gold Eagles and Canadian Gold Maple Leafs are both eligible.

However, it’s critical to remember that not all precious metal assets can be included. Collectible coins, regardless of their precious metal content, are usually ineligible for inclusion in a Gold IRA.

On the unfortunate event of the account holder’s death, the assets in the Gold IRA are typically transferred to their designated beneficiaries or heirs. These recipients have two choices: they can either take possession of the physical gold or opt to sell it for cash. It’s worth noting, though, that there could be potential tax implications tied to this inheritance (that is, unless the account holder implemented a Buy, Borrow, Die strategy).

If you currently hold an IRA or 401(k), either regular or Roth, you can opt to roll over some or all of its funds into a Gold IRA. The process for this Gold IRA rollover is identical to that of any other retirement fund. You fill out an account application and usually, the account is established within 24 to 48 hours of the completion and receipt of the application.

After the transfer request is received by all parties, the two custodians will coordinate to move the funds to the new custodian and create a new Gold IRA. Once the funds are accessible in the new IRA account, you can review the available precious metal options and choose the type you want to purchase.

The #1 Mistake Investors Make With Gold IRA’s

The number one mistake people make when investing in Gold IRAs is underestimating the true cost of owning, storing, and selling the physical gold. They forget that a Gold IRA, unlike a traditional IRA, involves physical goods, and hence comes with additional fees that can really add up.

Firstly, you have the seller’s markup, a one-time fee that depends on the type of gold you purchase— whether it’s bullion, coins, proofs, or others. The markup varies by vendor, making the going rate for gold just the starting point of your costs.

Next, there’s the retirement account setup fee, a one-time charge for establishing your new IRA account. As not all financial services firms handle Gold IRAs, this fee can be higher than the usual setup fee for standard IRAs.

Then, there’s the annual custodian fee. This fee, which can include asset or transaction fees, may be higher for Gold IRAs since the investment needs to be stored and managed by a certified custodian. It’s essential to note that this is not a one-and-done cost; it’s a yearly expenditure that’ll persist for as long as you own the Gold IRA.

Storage fees are another cost to keep in mind. Your gold has to be stored by a qualified storage facility, which means you’ll be paying regular fees for the secure storage of your investment.

Lastly, there are cash-out costs. When you decide to close your Gold IRA, you’ll typically sell your gold to a third-party dealer. Unfortunately, these dealers usually want to pay less than the market price, which could result in you losing some of your investment unless the price of gold has risen significantly.

To avoid this mistake, you need to be aware of these costs when considering a Gold IRA. Factor them into your calculations and compare them to potential returns. Moreover, you might be better off with a checkbook IRA.

This type of self-directed IRA does not require custodian management, hence potentially saving you from custodian fees. However, setting up a checkbook IRA is a complex process that requires forming a limited liability company (LLC), among other requirements.

Gold IRA vs Physical Gold: What’s the Difference?

To sum everything up, let’s define the key differences between investing in physical gold versus a Gold IRA.

Liquidity:

In terms of liquidity, physical gold has the upper hand. It’s possible to sell physical gold at any given moment as the market for gold is generally active. In contrast, a Gold IRA may impose certain conditions or restrictions, potentially creating a delay when you want to access your funds. For instance, there might be a penalty for withdrawing before a certain age.

Storage:

If you opt for physical gold, remember that safe storage will be your responsibility. You might choose to store your gold at home in a safe or use a bank’s safe deposit box. Conversely, a Gold IRA removes the storage headache, as a custodian holds the assets for you.

Fees:

When it comes to fees, the two forms of gold investment diverge significantly. Physical gold often only requires a one-off purchase fee. On the other hand, Gold IRAs tend to carry fees associated with account setup and ongoing management. This is a crucial point to keep in mind while deciding.

Taxes:

The tax implications are also markedly different. Gold IRAs come with some tax benefits. In contrast, physical gold does not enjoy any tax benefits and is subject to a capital gains tax which could be as high as 28%.

Control:

With physical gold, you have full control and a wider array of options concerning what specific types of gold you invest in. A Gold IRA, however, has a limited set of investment options.

The pros and cons of investing in a Gold IRA

Gold IRA vs Physical Gold: Which is the Better Investment Option?

In our opinion, it’s neither. From a perspective of simplicity and cost-effectiveness, the best way to invest in gold might be through Exchange-Traded Funds (ETFs) or mutual funds that focus on precious metals, rather than holding physical gold in an Individual Retirement Account (IRA). Let’s take two notable examples into consideration here.

First up, we have the SPDR Gold Shares ETF (GLD). This ETF serves as a pass-through for the physical ownership of gold, allowing investors to gain exposure to the asset class without the hassle of physically holding it. What makes GLD appealing is its daily liquidity—something that’s not readily available when you own physical gold.

The expense ratio for GLD is fairly reasonable at 0.40%. However, it’s crucial to be aware of the insurance situation: the intermediaries involved with this ETF aren’t obligated to fully insure the gold. As a result, ETF shareholders may not be completely protected against losses unrelated to custodial negligence.

Next, let’s talk about the Vanguard Precious Metals and Mining Fund (VGPMX). This low-cost mutual fund invests in companies that mine and explore gold and other precious metals. It’s not a pure gold fund, meaning it diversifies its investments across various precious metals and related companies.

While this fund’s results do tend to mirror the price movements of gold and related metals, they don’t always move in perfect unison due to the diversified nature of its investments.

So, if you’re looking to add gold and other precious metals to your investment portfolio, consider these two options. They offer accessibility, liquidity, and exposure to the asset class, while eliminating the need to physically hold the metal in an IRA. Just remember, like any other investments, they come with their own set of risks that need to be understood before diving in.

Want to learn more about investing in gold and private market deals?

Here at Equifund, we help investors access early-stage opportunities not found anywhere else. To view our current listings, go here now.

P.S. Equifund just launched its latest Regulation A+ offering for an already-publicly-traded gold royalty and streaming company.

Frequently Asked Questions about Gold IRA vs physical gold

How is gold taxed in an IRA?

When it comes to taxes, investing in a Gold IRA and physical gold have some differences. With physical gold investments, any profits made from selling the asset are typically subject to capital gains tax at a rate of up to 28%.

However, with a Gold IRA, as long as you follow the rules regarding contributions and withdrawals, your account is considered tax-deferred or even tax-free. When you withdraw funds from your account after age 59 ½, they will be taxed as regular income.

It’s important to note that if you withdraw funds before age 59 ½, you may be subject to an early withdrawal penalty and taxes on the amount withdrawn. So while both options offer potential benefits for investors seeking exposure to gold, it’s important to consider the tax implications before making a decision.

Does a Gold IRA make money?

Gold essentially profits from two primary drivers: long-term inflation and uncertainty risk. Let’s break this down.

- Long-term Inflation: Over time, the value of money tends to decrease due to inflation. On the other hand, gold and silver have historically maintained their purchasing power. So if you have gold in your IRA, its value could potentially rise in sync with inflation.

- Uncertainty Risk: The value of gold and silver also often increases during times of geopolitical or economic uncertainty. For instance, if there are concerns about the solvency of foreign nations or the potential outbreak of war, investors typically turn to gold and silver as “safe-haven” assets. In these scenarios, the demand for these precious metals increases, which could boost the value of a Gold IRA.

A Gold IRA may make money by capitalizing on inflation and uncertainty, potentially serving as a hedge against financial turbulence. Rather than paying out dividends or income, it aims to preserve and potentially grow wealth in the face of adverse conditions.

Gold IRA transfer process

First, you’ll need to establish a self-directed IRA account with a custodian that offers the option of investing in precious metals.

Next, you’ll buy the gold and arrange to have it delivered directly to an IRS-approved depository. This is a key point, as the IRS mandates that all precious metals in an IRA must be held in such a facility.

Once the gold is safely housed in the depository, it becomes part of your investment portfolio, just like any stocks or bonds you might own within your IRA. Please keep in mind there could be costs linked to storing and managing the gold in your IRA. So, it’s worth shopping around and comparing different custodians’ fee structures before making your final decision.