Of all the wealth-building strategies and tactics employed by the super-rich—e.g. self-directed IRA LLCs and blind trusts—the Buy, Borrow, Die approach stands apart.

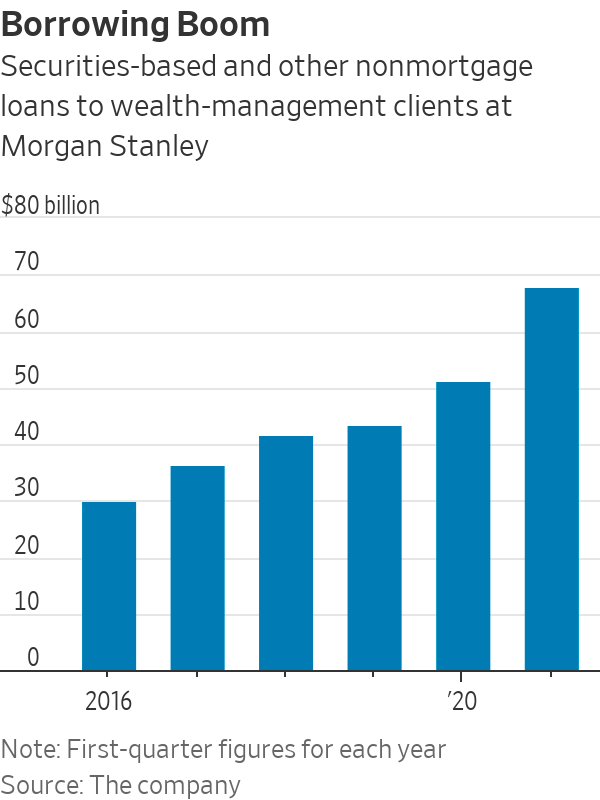

Morgan Stanley reports that their wealth management clients have amassed a colossal $68.1 billion in non-mortgage, security-based loans—a figure that’s doubled since 2016. This might prompt the question, “Why are the wealthy borrowing money?”

After all, if they’re already awash in wealth, why the need for loans? The answer lies in an ingenious tax planning strategy that has allowed the wealthy to retain and even grow their fortunes without having to sell their assets. This is the secret sauce in creating generational wealth and it’s the driving force behind many of America’s wealthiest families.

Please keep in mind that we are not tax professionals nor Estate Planning attorneys. If you believe information in this article may pertain to your situation, we recommend you discuss it with your tax advisors.

The strategy is called ‘Buy, Borrow, Die’. This approach involves buying appreciating assets like stocks, collectibles, and particularly real estate; borrowing against these assets at less than their appreciation rate; and eventually passing the assets down to heirs, often with little or no capital gains tax liability.

Even billionaires like Warren Buffet and Elon Musk are known for leveraging such strategies, often resulting in them paying less in capital gains taxes than many would expect. While it may seem that such a strategy is reserved for the super-wealthy, the principles can be applied at various levels of wealth.

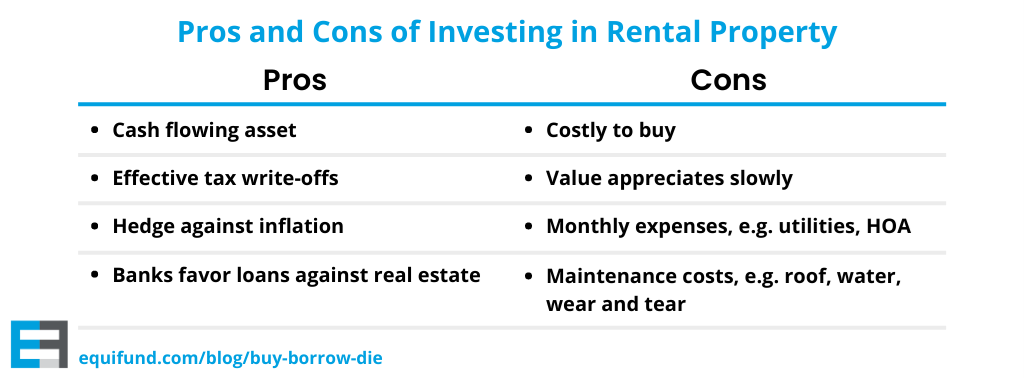

Owning rental real estate provides a prime example of this. It’s an asset that not only appreciates over time (generally speaking), but it’s also somewhat insulated from stock market volatility (ie. non-correlated).

Moreover, it provides a way to reduce taxable income through depreciation and it allows for cash extraction without needing to sell the asset.

Understanding the tax implications of the Buy, Borrow, Die strategy can go a long way in retaining your wealth and minimizing your tax burden. In this article, we’ll delve deeper into the intricacies of the Buy, Borrow, Die strategy and explore how you can leverage it to build generational wealth.

Key Takeaways:

- Appreciating Assets: Wealthy individuals often store most of their wealth in assets like stocks, real estate, and operating businesses.

- Buy, Borrow, Die: This approach involves buying appreciating assets; borrowing against them at low interest-rates; and eventually passing the assets down to heirs—with little or no tax liability.

- Step-up in Basis: Heirs can then sell their inherited assets tax-free due to the step-up in basis rules.

- Rental Real Estate: Rental real estate is one of the best assets to use in the Buy, Borrow, Die strategy due to monthly income and expenses being relatively predictable.

How Do the Rich Avoid Taxes?

First, it’s important to note that the super-rich don’t typically receive their wealth in the form of weekly paychecks or regular salaries.

Rather, very high-net-worth individuals (HWNI), worth at least $5 million to $20 million, often store most of their wealth in assets like stocks, real estate, and operating businesses. This type of wealth allows investors to avoid paying capital gains taxes, because it’s not considered income until it’s sold or “realized”.

Now, this is where legal tax avoidance comes into play. Wealthy individuals can borrow money against these assets at relatively low interest rates. This borrowed money is not considered income and therefore is not subject to income tax. It’s a little like taking out a mortgage against a house, but on a significantly larger scale.

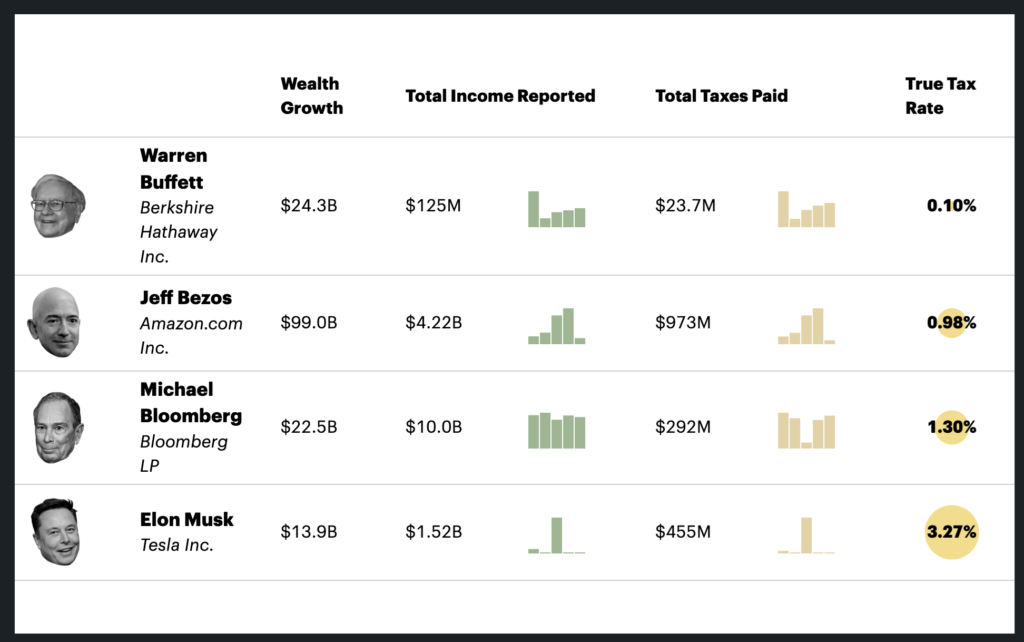

This is how, according to ProPublica’s analysis, the 25 richest Americans were able to pay a true tax rate of only 3.4% between 2014 to 2018.

Estimated taxes paid by the four richest Americans from 2014 to 2018. Source: ProPublica

Why do rich people borrow money?

One of the things most people wonder about wealthy people is this: if they have so much money already, why do they need to borrow more?

The rich tend to borrow money for three key reasons:

- Liquidity: Just because someone has a billion dollar net worth doesn’t mean they have $1 billion in cash. Using their assets as collateral allows the wealthy to get access to capital without selling the asset.

- Wealth Building: Borrowing against assets allows the wealthy to invest in more growth opportunities without depleting their original asset base, thus amplifying their wealth creation capabilities.

- Tax Reduction: Borrowing doesn’t trigger capital gains tax like selling assets would. Moreover, the interest on loans can often be deducted, thus further minimizing their tax liabilities.

Let’s say you’re a wealthy individual looking for more capital, perhaps to finance a new venture.

In this situation, you can cash out some of your investments. But this also means you’ll have to pay capital gains taxes. On the other hand, instead of selling, you can take a loan using your assets as collateral. In this case, you get access to capital while your investment continues to earn dividends and appreciate in value.

And unlike income generated from selling assets, the money from your loans isn’t considered taxable income.

What is the Buy, Borrow, Die strategy?

“Buy, Borrow, Die” is a phrase conceived by Edward McCaffery, a tax law professor at the University of Southern California Law School. This approach refers to a tax planning strategy used by the wealthy to maximize their wealth without having to pay taxes.

Here’s how it works:

First, the affluent individual or family “buys” an asset with potential to grow over time. Next, rather than selling these assets when they need funds (which would require them to pay capital gains taxes), they “borrow” against them using the asset as collateral.

The final piece of the puzzle comes in with “die”. When the original asset holder passes away, their heirs or beneficiaries receive these assets. These heirs can then sell the assets (after paying off the loan-balance, that is) and still avoid capital gains taxes due to the step-up in basis rules, which we’ll explain in detail below.

To give you some perspective on the increasing popularity of the Buy, Borrow, Die strategy, just look at the recent surge in securities-based loans at major financial institutions. Bank of America’s wealth and investment management arm saw a 50% rise in such loans from 2019 to 2022.

Similarly, securities-based loans at Morgan Stanley doubled during the same period.

Growth of securities-based loans at Morgan Stanley from 2016 to 2020. Source: Morgan Stanley

How Does Buy, Borrow, Die Work?

At its core, Buy, Borrow, Die is about capitalizing on what we call interest-rate arbitrage. Simply put, it’s the practice of borrowing money at one interest rate and using it to generate returns at a higher rate.

Here’s how the Buy, Borrow, Die strategy works step-by-step:

Step 1. Buy Assets

This step, broadly known as the accumulation phase, is about acquiring or creating valuable assets. It’s the most critical step taken by wealthy individuals to secure their wealth.

Billionaires, for instance, often created startups that eventually turned into massive corporations. The asset here is the company they’ve established.

However, this isn’t the only way to accumulate assets. For professionals like doctors and lawyers, this phase involves securing a high-paying job and buying assets that have the potential to appreciate over time—like stocks, real estate, and private capital.

Once an individual reaches a substantial level of wealth, they can leverage these assets in interesting ways using the next step of this strategy.

Step 2. Borrow Against Your Assets

This where the assets you’ve acquired are used as collateral to borrow money—all without triggering a taxable event.

Suppose you’ve got a robust stock portfolio. You can then take out a Securities Backed Line of Credit (SBLOC). This kind of loan lets you tap into the value of your portfolio without having to sell off any assets and subsequently paying capital gains taxes. What makes SBLOCs attractive to lenders is the relative ease with which the securities can be seized and sold, making them a low-risk lending option.

The ceiling for such a loan is usually around 50% of your portfolio’s value. However, wealth managers often caution against borrowing more than 25% of your account balance, especially for long-term loans. This will provide a cushion against stock market volatility, much like what we experienced in 2022 and 2023.

Borrowing against assets isn’t limited to stock portfolios either. Let’s say you own a home and have built up a certain amount of equity in it. You could opt for a Home Equity Line of Credit (HELOC), using your home as collateral. Banks tend to favor real estate-backed loans due to their stability compared to the fluctuating value of stocks.

Step 3. Die and Pass Your Wealth On

The final step in the strategy is where the proverbial tax baton is handed off to the next generation.

Under the existing tax code, when you pass away, your heirs receive a “stepped-up basis” on the assets they inherit from you. This means that their cost basis—the original amount paid for an asset—is stepped up to the market value of the asset at the time of your death. Meaning once you have passed away, your heirs would be able to sell the assets without having to pay taxes on the capital gain.

Imagine you had purchased a building 20 years ago for $1 million and over the years, the value of that building increased to $2.5 million. If you were to pass away at this point, your heirs would inherit the building with the stepped-up cost basis of $2.5 million. This implies that if they decide to sell the property at this valuation, they wouldn’t owe any capital gains tax. This is because for tax purposes, their gain is calculated from the $2.5 million, not the original $1 million.

By utilizing this loophole, families can pass on their wealth without incurring a hefty tax bill. This is why many wealthy families set up trusts – it’s a way to manage and pass on their wealth at a stepped-up cost basis.

Buy, Borrow, Die Strategy Examples

Now let’s talk about all the different assets we can buy and what they can do for us.

Real Estate

Many wealthy people are able to potentially fund all their lifestyle expenses simply by borrowing against their real estate. Additionally, rental real estate is one of the best assets to use in the Buy, Borrow, Die strategy due to monthly income and expenses being relatively predictable.

To illustrate this with an example, let’s imagine you’re a property investor and you’ve purchased an apartment building for $10 million. Over time, thanks to growth in the real estate market, this building’s value appreciates to $20 million. Now, rather than selling the building and having to pay 15% to 20% on the capital gain, you can use this increased value to maximize your loan to value ratio, or LTV.

LTV is a measure of how much you’re borrowing compared to the value of the asset you’re using as collateral. If you have a LTV of 70%, for example, you’re borrowing 70% of the asset’s value. So, if your $20 million building has a LTV of 70%, you’d be able to borrow $14 million against it.

Here’s where it gets interesting. When you borrow this money, you’re not incurring any immediate tax liabilities because loans are not considered income by tax authorities. This means you’ve just accessed $14 million tax-free. Meanwhile, your building is still producing a positive cash flow from the rents your tenants are paying.

Now you’re free to live off the loaned money. The goal is to only spend the cash flow and leave the loan principal untouched. When managed carefully, the cash flow can cover the loan interest and any operational costs of the building, which includes maintenance, utilities, and the like.

Stocks

Imagine you borrow $1 million at an interest rate of 3%. Over the course of a year, you’d owe $30,000 in interest. But what if you could use that $1 million to invest in stocks or other assets that yield a return of, say, 7% per year? That means you’d gain $70,000 from your investment. When you deduct the $30,000 you owe in interest, you’d still be left with $40,000.

In the realm of high-tech billionaires, Oracle founder Larry Ellison has pledged over $4 billion of his company shares to fund his other ventures. Elon Musk, on the other hand, was originally planning to fund his Twitter purchase with $44 billion of Tesla shares.

While the Buy, Borrow, Die strategy seems lucrative initially, it’s far from risk-free. During unexpected market downturns like the one experienced after the Russian-Ukraine war, the value of your portfolio can be cut in half. And if your portfolio value dips below the margin minimum, you could end up losing everything. Bill Hwang of Archegos Capital Management, for example, lost $20 billion in March 2021 due to over-leverage.

Wealth Building Like the Rich

The uber-wealthy don’t just borrow against their assets to fund their lifestyle expenses—they use that capital to invest in more growth opportunities.

Here at Equifund, we help investors access early-stage opportunities not found anywhere else. To view our current listings, go here now.