Despite President Franklin Roosevelt’s famous quote, “Taxes are dues we pay for the privileges of membership in an organized society”, it appears that one common thread in our politically polarized society is our hatred of taxes.

That’s why many Americans are looking for every opportunity they can to reduce the amount of taxes they pay each year.

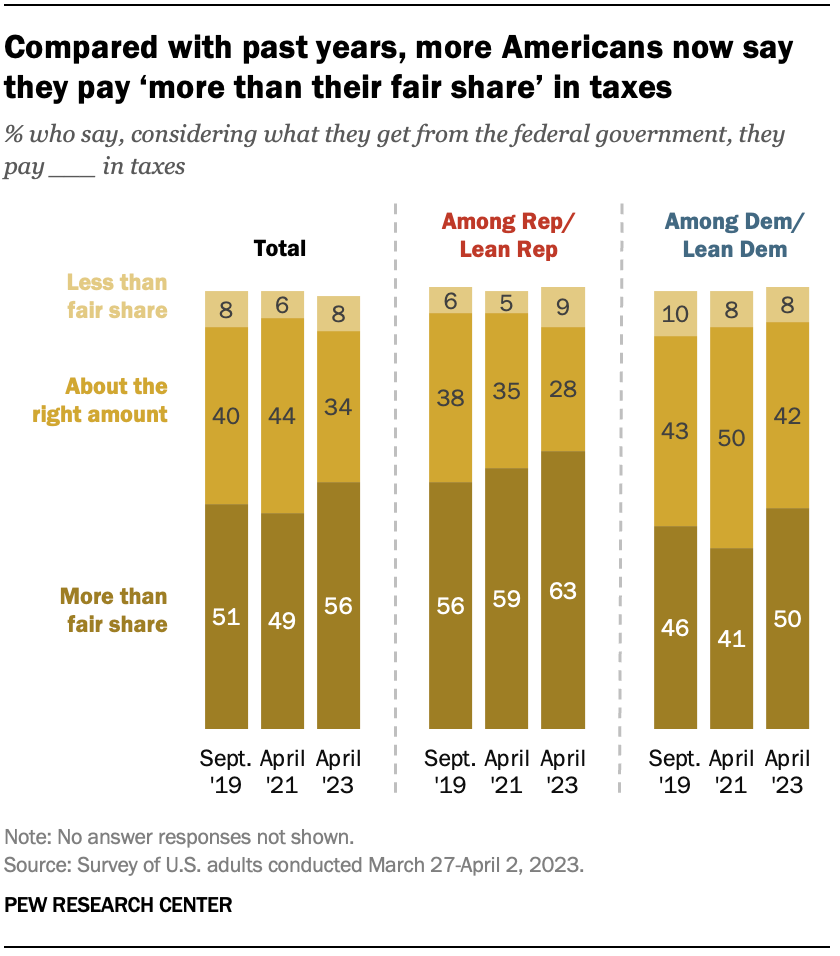

Percentage of Americans who believe they pay more than their fair share of taxes.

Unfortunately, the tax code is long, complex, and difficult for the average person to understand.

As per Public Law 117-154, dated June 23, 2022, the U.S. Tax Code is a whopping 6,871 pages long. This doesn’t even take into account federal tax regulations and official tax guidance – another ~70,000 pages!

So if you feel overwhelmed at the thought of understanding tax liability, just know that you’re not alone. This blog post will break down the essentials of tax liability, how your personal (and corporate) tax liability is calculated, and what you can do to legally pay as little as possible.

Key Takeaways:

Tax Complexity: The U.S. Tax Code is complex and lengthy, spanning over 6,871 pages with additional federal tax regulations and guidance.

Understanding Tax Liability: Tax liability, the total amount of taxes owed, is determined by your modified adjusted gross income (MAGI).

Active vs Passive Income: Active income is taxed at higher rates than passive income. Shifting income to passive sources may reduce tax liability.

Qualified Business Expenses: Business owners can take advantage of additional tax reduction strategies by understanding what they can (and cannot) consider a qualified business expense. This, in effect, allows you to spend “pre-tax” dollars instead of “after tax” dollars.

Tax Credits and Deductions: Understanding how to apply tax credits and deductions can also significantly reduce your taxable income.

The Ever-Growing Tax Compliance Burden

Did you know that a single update to the tax code can span up to 174 pages? It’s mind-boggling to think that the U.S. tax code has been revised over 4,000 times in the last decade.

When it comes to the length of the tax code, it’s crucial to distinguish between the actual US Tax Code – which is a product of the U.S. Congress, enshrined in Title 26 of the United States Code, and stretches over 6,871 pages – and the ever-growing tax regulations, interpretations, and official tax guidance that balloon the total to an astonishing ~75,000 pages.

The U.S. Tax Code currently stands at a staggering 6,871 pages long.

These Treasury regulations, sometimes referred to as Federal Tax Regulations, pick up where the Internal Revenue Code leaves off, offering the U.S. Department of Treasury’s official interpretation of the code.

While these aren’t tax laws per se, they’re vital for understanding how to apply the tax laws to minimize or reduce your tax liability here. But that’s not all; on top of the sprawling federal tax code, there are an additional 13,000 state, county, and local tax jurisdictions to consider.

Now let us explore how these increasingly complicated tax laws affect your bottom line.

Understanding Tax Liability

Tax liability is the total amount of taxes owed by individuals (or corporations) to the government. The amount of taxes owed and tax payments is determined by something called your modified adjusted gross income (MAGI) – which is defined as your household’s adjusted gross income (AGI) after any tax-exempt interest income and after factoring in certain tax deductions.

The Internal Revenue Service (IRS) uses MAGI to establish whether you qualify for certain tax benefits, like:

Whether your income does not exceed the level that qualifies you to contribute to a Roth individual retirement account (IRA).

Whether you can deduct your traditional IRA contributions if you and/or your spouse have retirement plans, such as a 401(k) at work.

Whether you’re eligible for the premium tax credit, which lowers your health insurance costs if you buy a plan through a state or federal Health Insurance Marketplace.

While many experts would agree that you shouldn’t simply take an action because of the taxable benefits, it’s important to understand how the tax code is designed to incentivize certain behaviors the federal government wants you to take.

For example, the child tax credit is designed to provide relief to households who are producing our nation’s future tax payers. The home mortgage interest deduction is designed to encourage home ownership. And the tax incentives for contributing to retirement accounts are designed promote saving for retirement.

But here’s what most taxpayers don’t understand about how to significantly reduce their tax liabilities: If you don’t earn income, you don’t pay income tax.

For example, debt does not count as income, and is not taxed. If you have a cashflowing asset that generates more income than the interest payments on the debt, instead of paying the tax on the income the asset produces, you can simply borrow against it tax free.

If you don’t have a way to “not” earn income, the next thing you will need to understand is this: how you earn your income will determine how much you pay in taxes. This means understanding the difference between Active Income and Passive Income.

Active Income accounts for all income earned through wages, salary, and short-term capital gains. This is taxed at both the federal and state levels, as defined by the tax code.

Passive Income accounts for all income earned through self-charged interest, rental properties, and businesses in which the person receiving income does not materially participate. This income is taxed at a lower rate than Active Income.

The single easiest way to lower your taxable income is to shift income out of the “Active” tax brackets into “Passive” tax brackets.

Last but not least, the final way to reduce your tax liability is to understand how credits, deductions, and exemptions work… and how – with forward looking planning – you can structure your income and expenses in a way that qualify for desirable credits, deductions, and exemptions.

However, it’s important to note that you can only deduce Active credits and deductions from Active income, and Passive credits and deductions from Passive income.

Tax Liability Formula and Calculation

Calculating tax liability varies depending on whether you’re an individual or a business taxpayer.

The general process of calculating your tax liability involves determining gross income, applying deductions and exemptions, and using tax rates and brackets to calculate the final amount owed.

Let’s dive deeper into the key components of this calculation.

Gross Income

Gross income refers to the total income earned by an individual or business before deductions and exemptions are applied. For individuals, this includes:

Salary

Wages

Tips

Other sources of income.

Businesses, on the other hand, need to consider their total revenue, minus the cost of goods sold, to determine gross income.

Tax Deductions and Exemptions

Mortgage interest can be claimed as a tax deduction.

Tax deductions and exemptions are expenses that can be subtracted from gross income to reduce taxable income, which in turn reduces your tax liability.

The standard deduction varies based on your filing status, such as single, head of household, or married filing jointly. Examples include business expenses, mortgage interest, rental property depreciation and charitable donations.

Tax Credits and Their Impact on Tax Liability

Tax credits are financial incentives that directly reduce the amount of taxes owed. Being aware of the tax credits you may be eligible for and claiming them on your tax return is key to maximizing your tax savings.

Tax credits can be claimed for various reasons, such as having children, pursuing higher education, or adopting energy-efficient measures in your home. Business, on the other hand, can claim credits for spending money on research and development (R&D) or employee retirement plans.

Tax Rates and Brackets

Tax brackets are ranges of income subject to specific tax rates. The U.S. tax system is progressive, meaning that as your income increases, you’ll move into higher tax rate brackets and pay a higher percentage in taxes on the portion of your income that falls within those brackets.

Frequently Asked Questions?

What is a person’s tax liability?

Tax liability is the total amount of tax debt owed by an individual to a taxing authority like the IRS, based on their earnings and filing status. This tax bill amount includes income tax, capital gains tax, self-employment tax, penalties, interest and any past-due taxes from previous years.

What are tax liabilities examples?

Common examples of tax liabilities include income taxes, sales tax, and the capital gains tax liability. Liabilities may be imposed by federal, state, and local governments.

How do I know if I have tax liabilities?

To calculate tax liability and determine if you have any tax liabilities, look at line 37 of your Form 1040 for the current tax year. This will tell you your federal tax liability based on your taxable income after taking deductions and claiming credits.

Is tax liability the same as a refund?

No, tax liability is not the same as a refund. It is the amount that you owe to the government after your withholdings and payments are taken into account. Your total tax liability is specified on Form 1040 (line 24).

Want to learn more about investing in private market deals?

Here at Equifund, we help investors access early-stage opportunities not found anywhere else.