Have you ever wondered how the wealthy rake in millions annually while avoiding taxes? It all boils down to one principle: property depreciation. Misinterpret deprecation and you might face harsh clawback provisions that nullify your tax deductions.

So, if you’re a landlord or considering buying a rental property to decrease your taxable income, this article will teach you on how depreciation works. You’ll also learn how to utilize cash flow producing assets – like real estate – to generate income that’s 100% tax-free.

Key Takeaways:

Tax Benefits of Depreciation: Rental property depreciation is a tax deduction that allows investors to save on taxes and increase profits. Understanding this can greatly enhance the financial benefits of real estate investment.

Eligibility Criteria: To be eligible for property depreciation, certain conditions must be met, including ownership, use for business or income-producing activity, and a determinable, useful life.

Methods of Calculation: Various methods are available for calculating depreciation, including straight-line, double declining balance, units of production, and sum-of-the-years digits. The chosen method can significantly impact tax deductions.

Additional Tax Breaks: Besides depreciation, real estate investors can also deduct business expenses, losses against active income, and loan interest payments. These deductions can further reduce tax burdens and increase profits.

Depreciation Recapture and 1031 Exchange: When selling a property, depreciation recapture taxes may apply, but a 1031 Exchange can delay these taxes. This strategic move allows for the replacement of a property with a similar kind without immediate tax implications.

Understanding How the Rich Avoid Taxes

To understand rental property depreciation, it helps to first understand how the rich use debt to build wealth and avoid taxes.

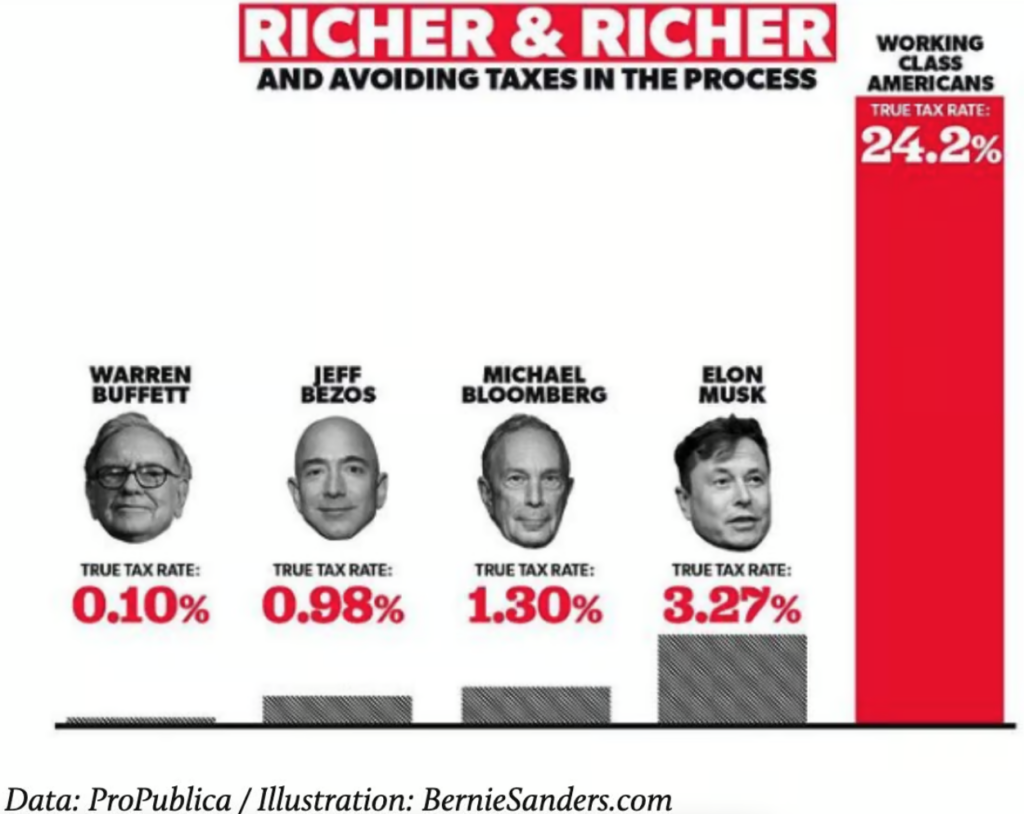

The true tax rates of several of the world’s wealthiest billionaires.

In the article mentioned earlier, it is explained that when acquiring a target company, Leveraged Buyouts (LBOs) provide a safety net to Private Equity (PE) firms in the event of bankruptcy. This raises the question: why is the PE firm allowed to claim a tax write-off for a canceled debt they weren’t responsible for?

Here are the key elements that tie everything together:

Canceled Debt

When the company bought out goes bankrupt, it’s able to dissolve or dismiss the debts that were part of the Leveraged Buyout (LBO).

Thanks to tax code exceptions for bankrupt companies, this cancelled debt doesn’t count as taxable income. As the main shareholder, the Private Equity (PE) firm can merge the financials of the bought-out company, and also enjoy this tax write-off on its own tax returns.

Net Operating Loss (NOL) Carryforward

The dismissed debt creates a Net Operating Loss (NOL) for accounting purposes by decreasing net income. The PE firm can carry this NOL forward to offset income and profits from other investments, thereby slashing its tax bills. Occasionally, the NOL can also be bought directly from the bankrupt company during bankruptcy proceedings.

Depreciation

After acquiring the company, the PE firm can speed up the depreciation of the company’s assets. This decreases taxable income and provides another beneficial deduction. The tax savings from depreciation then pile up to the PE investor.

This sets the perfect stage for our discussion on how residential rental property depreciation works.

Understanding Rental Property Depreciation

In short, the main reason all real estate investors should be intimately familiar with property depreciation is that it allows them to generate more profit on their passive real estate investments. Now let’s dive deeper into what depreciation is and how it could benefit you.

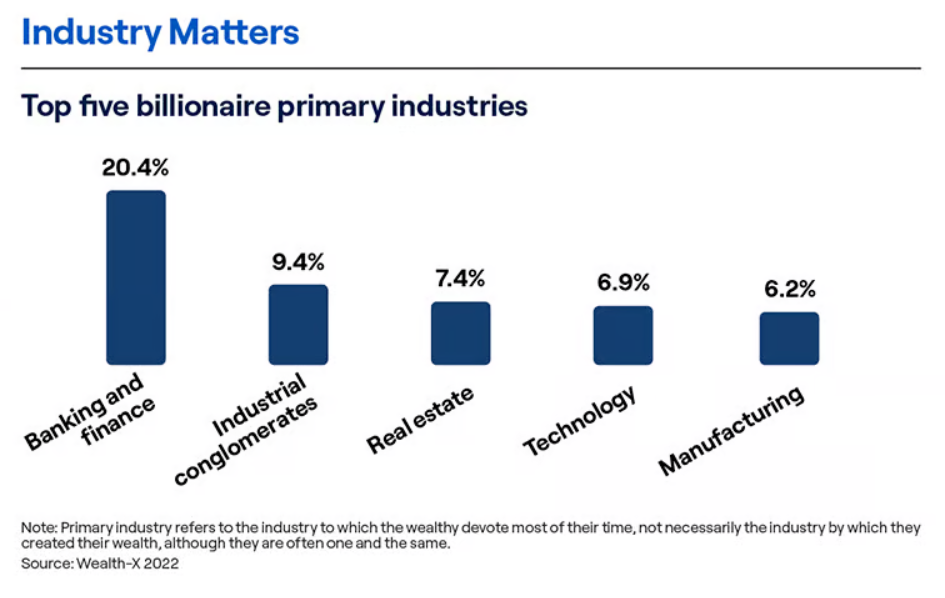

The top five primary industries billionaires operate in. Source: Wealth-X

What Is Depreciation?

Real estate has long been touted as a reliable route to amass wealth for generations. While it’s true that a large portion of today’s billionaires have amassed their fortunes through banking, real estate has held a significant role in the global financial system for millennia.

Why is this the case? Simply put, real estate – whether it’s used for mining, oil extraction, agriculture, forestry, housing, commercial activities, or other industrial purposes – is a capital asset that generates income, typically through rent or royalties.

The magic that transforms real estate into a potential tax-free source of income is a little thing known as depreciation. This is an annual income tax deduction that lets you recover the cost (or other basis) of a certain property throughout the period you use the property.

Why the Depreciation Deduction Exists

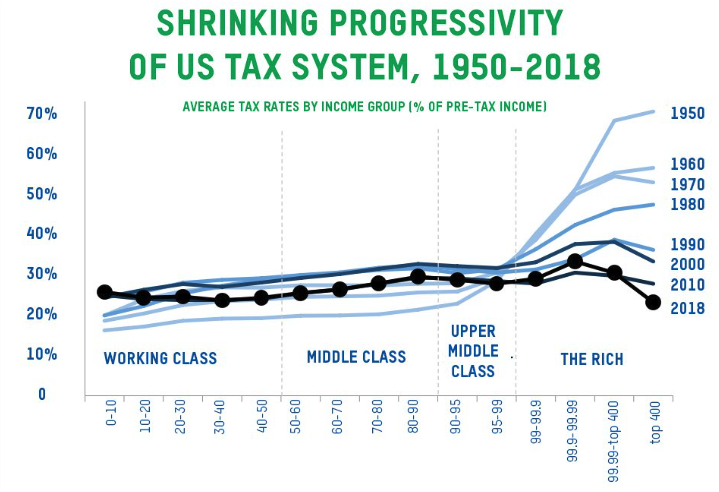

In the current political landscape, the phrase “Tax the Rich” and the resulting animosity towards the wealthy is, I believe, quite justified when you compare historical tax rates to current ones.

This graph illustrates how the tax rate has become dramatically less progressive over the past 70 years. Credit: “The Triumph of Injustice: How the Rich Dodge Taxes and How to Make Them Pay,” by Emmanuel Saez and Gabriel Zucman.

However, to have a meaningful discussion about what’s “fair” and what’s not, it’s crucial to understand the role tax deductions play: they serve as an incentive system to guide the actions of corporations and individuals.

Primarily, governments are interested in stimulating the economy, fostering job creation, and promoting activities that are socially beneficial. These tax incentives offered to the private sector are supposed to result in a net-positive activity in the form of desired outcomes and future tax receipts.

Let’s delve into why real estate, particularly residential and commercial properties, receive such substantial tax benefits from the government.

Housing Supply: The government incentivizes real estate development to increase the housing supply, particularly affordable ones. These tax benefits make it more appealing for developers to construct residential properties, which also boosts employment in the construction sector.

Business Infrastructure: Commercial real estate forms the backbone of business operations and expansion. Tax deductions make it more feasible for investors to develop infrastructure like office buildings, industrial facilities, retail spaces, and more. This, in turn, supports business activities and job creation.

Economic Growth: A thriving real estate industry triggers a domino effect across the entire economy, stimulating sectors like construction, finance, and more. Tax benefits in real estate keep investments flowing and encourage broader economic growth.

Wealth Creation: For many middle-class investors, real estate is a tangible way to build wealth and financial stability. Tax deductions provide a level playing field against larger corporations.

Property Taxes: Increased real estate development boosts property values, leading to more tax revenue from property taxes for local governments.

Viewing the situation from the perspective of the entrepreneurs and investors who fund these projects, we must consider that they are undertaking a certain degree of risk to construct buildings, create jobs, and ultimately contribute to taxable revenue through their downstream impact.

In many respects, the positive impact they generate in the economy could be seen as their way of “paying their fair share,” and an acceptable reason for why they are taxed at a lower rate.

However, this does not mean that all tax deductions lead to fair and equitable results, or that the tax code, influenced by lobbying, isn’t biased in favor of the elite (for instance, the Buy, Borrow, Die strategy).

But here at Equifund, rather than complain about life’s injustices, we find it more beneficial to understand how the system truly operates, and how we can take part in these incentive programs that reduce our tax load by providing valuable goods and services to others.

For many individuals, this means stepping into the role of a real estate investor and/or entrepreneur.

How Rental Property Depreciation Works

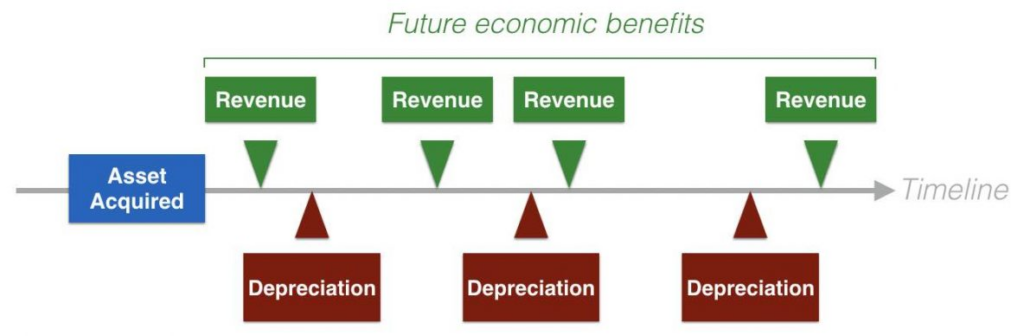

A graph illustrating how depreciation works over time.

Now that you understand what real estate depreciation is, let’s discuss the eligibility criteria for rental property depreciation, its lifespan and recovery periods, as well as using tactics like a cost segregation study that can help reduce real estate taxes, by accelerating deprecation rates.

Rental Property Depreciation Eligibility Criteria

To be eligible for property depreciation, there are certain conditions you must meet. The kinds of property that you can depreciate include machinery, equipment, buildings, vehicles, and furniture.

According to the IRS, you may depreciate property that meets all the following requirements:

It must be property you own.

It must be used in a business or income-producing activity.

It must have a determinable, useful life.

It must be expected to last more than one year.

It must not be excepted property, which includes certain intangible property, certain term interests, equipment used to build capital improvements, and property placed in service and disposed of in the same year.

Property Lifespan and Recovery Periods

Typically, you can’t deduct the full cost of your commercial or residential rental properties in the year you purchase, construct, or improve them (though there are exceptions, which we’ll touch on later).

Instead, you spread out the deduction (known as depreciation) over a certain period of time (the useful life of the asset). This accounts for the natural wear and tear of the asset, as well as any upkeep and enhancements made to it.

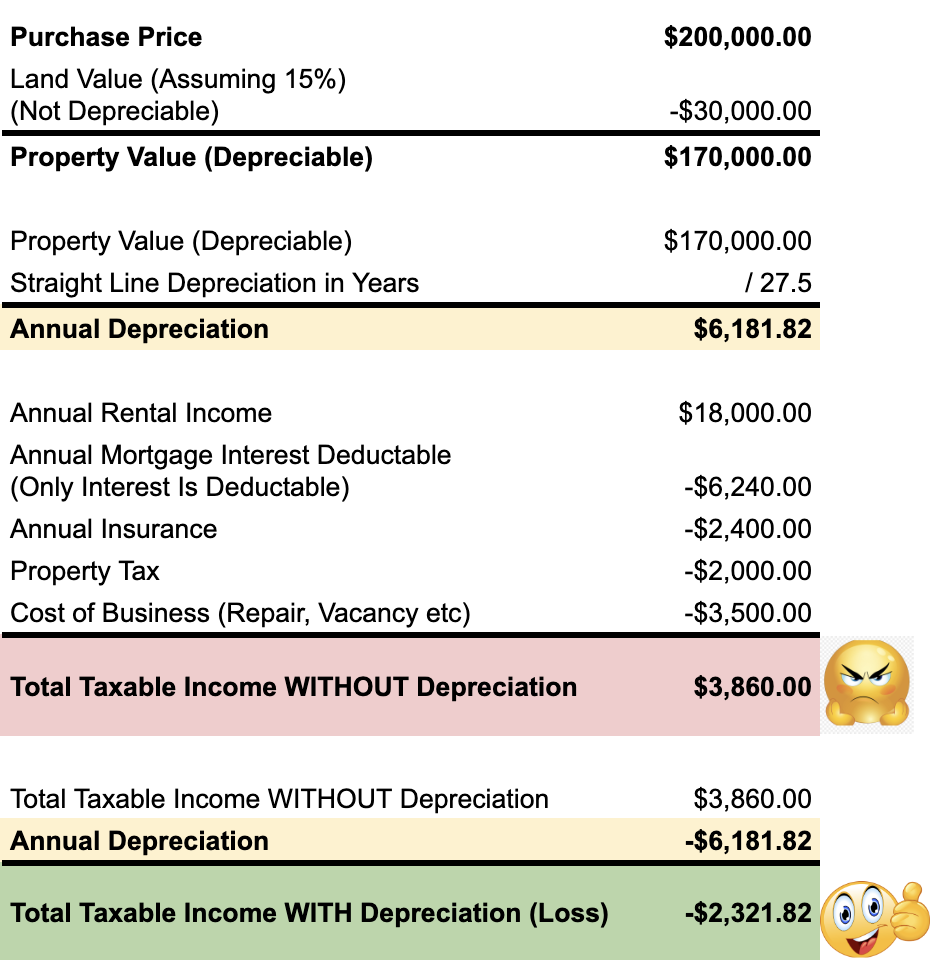

This recovery period is then applied to the cost of the property (i.e., your cost basis). This cost becomes an expense that can be used to counterbalance the income generated by the property. This could even result in a LOSS on paper, meaning you could pay zero taxes on that income!

An example of how to calculate depreciation. Source: EZ FI university

So, the question arises, over how many years should the depreciation be spread? This largely depends on the type of asset being depreciated and the depreciation method you opt for. According to the Modified Accelerated Cost Recovery System, the IRS offers two primary methods:

General Depreciation System (GDS) – This is the IRS’s main depreciation system, with recovery periods ranging from 3 to 25 years. It enables quicker depreciation through declining balance methods.

Alternative Depreciation System (ADS) – This system requires longer recovery periods of 10 to 40 years and only allows for straight-line depreciation. It is mandated in certain situations to prevent excessively rapid write-offs.

These two systems depreciate property in varying ways, such as by method, recovery period, and bonus depreciation.

Calculating the Deprecation of Your Rental Property

If you’re looking to claim depreciation on your rental property, knowing how to calculate how much you’ll be able to write off will allow you to maximize the cost savings of real estate depreciation come tax season.

Calculating the Cost Basis

The cost basis of your rental property is essential in determining its depreciation and can be calculated by taking the purchase price, subtracting any land value, as well as accounting for closing costs and improvements. Capital expenses such as legal fees, abstracts charges or recording bills must also be factored into this equation.

Methods for Calculating Depreciation

Generally, the General Depreciation System (GDS) is the most frequently applied method of depreciation, and it provides four different techniques for depreciation calculation:

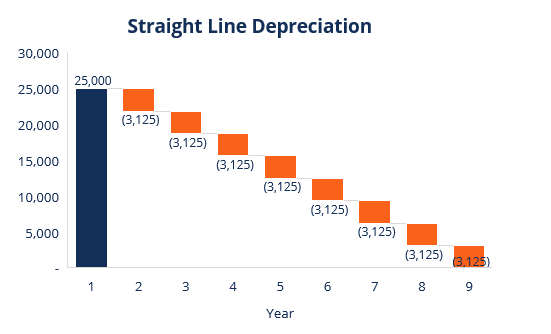

Straight line method – This method allows you to deduct an equal amount each year, spreading out the depreciation evenly over the asset’s useful life. This results in smaller depreciation expenses in the initial years.

Graph illustrating Straight Line Depreciation. Source: Corporate Finance Institute

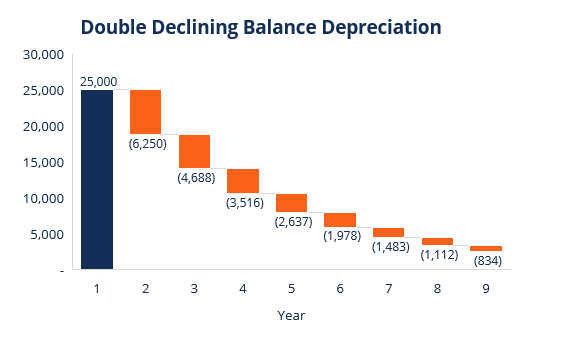

Double declining balance method – This accelerated depreciation method lets you deduct twice the straight-line rate in the first year.

This method acknowledges that assets are usually more productive in their early years and that any asset (like a car, for example) loses a larger portion of its value in the first few years of its use.

Graph illustrating Double Declining Depreciation. Source: Corporate Finance Institute

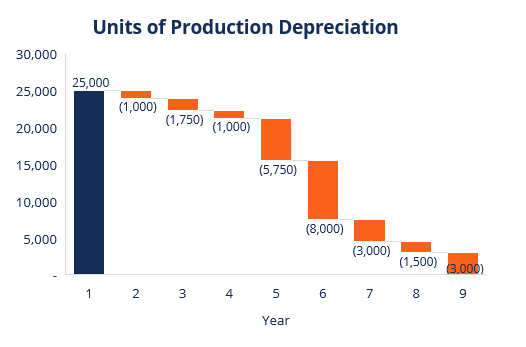

Units of Production Depreciation Method – This method depreciates assets based on the total number of hours used, or the total number of units to be produced by using the asset over its useful life.

Graph illustrating Units of Production Depreciation. Source: Corporate Finance Institute

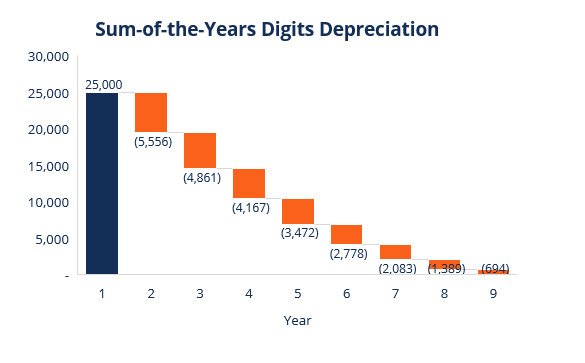

Sum-of-the-Years-Digits Depreciation Method – This is one of the accelerated depreciation methods. A larger expense is incurred in the early years and a smaller expense in the later years of the asset’s useful life.

In the sum-of-the-years digits depreciation method, the remaining life of an asset is divided by the sum of the years, and then multiplied by the depreciating base to determine the annual depreciation expense.

Here is a graph showing the book value of an asset over time with each different method:

Graph illustrating Sum-of-the-Years Digits Depreciation. Source: Corporate Finance Institute

Under GDS, each property type has a different recovery period. For example:

Automobiles: 5 years

Computer equipment: 5 years

Office furniture: 7 years

Residential rental property: 27.5 years

Non-residential real property: 39 years.

Why should you care about this? Because you can accelerate your depreciation schedule if you implement what’s called a Cost Segregation Study.

Accelerating Depreciation with a Cost Segregation Study

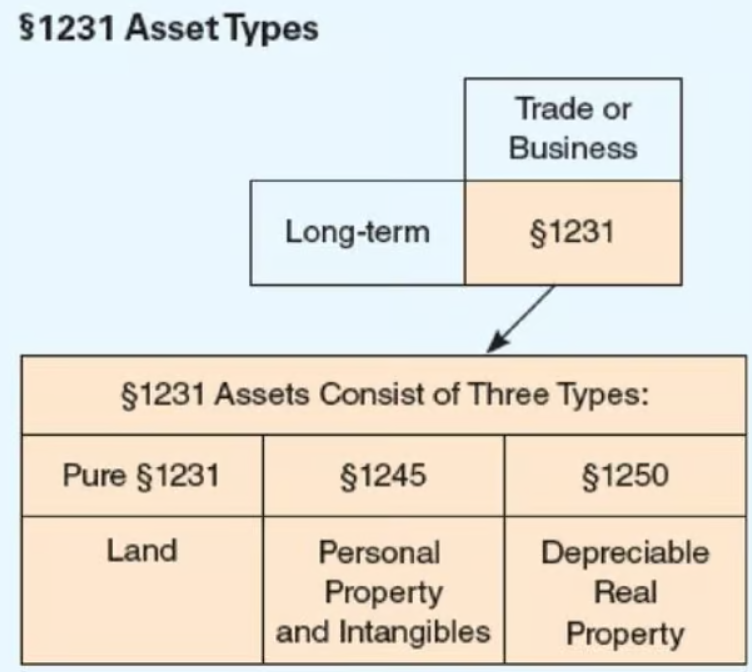

A Cost Segregation study empowers a taxpayer who owns real estate to reclassify certain assets as Section 1245 property. This classification has shorter useful lives for depreciation purposes, compared to the useful life for Section 1250 property.

A breakdown of 1231 Asset Types.

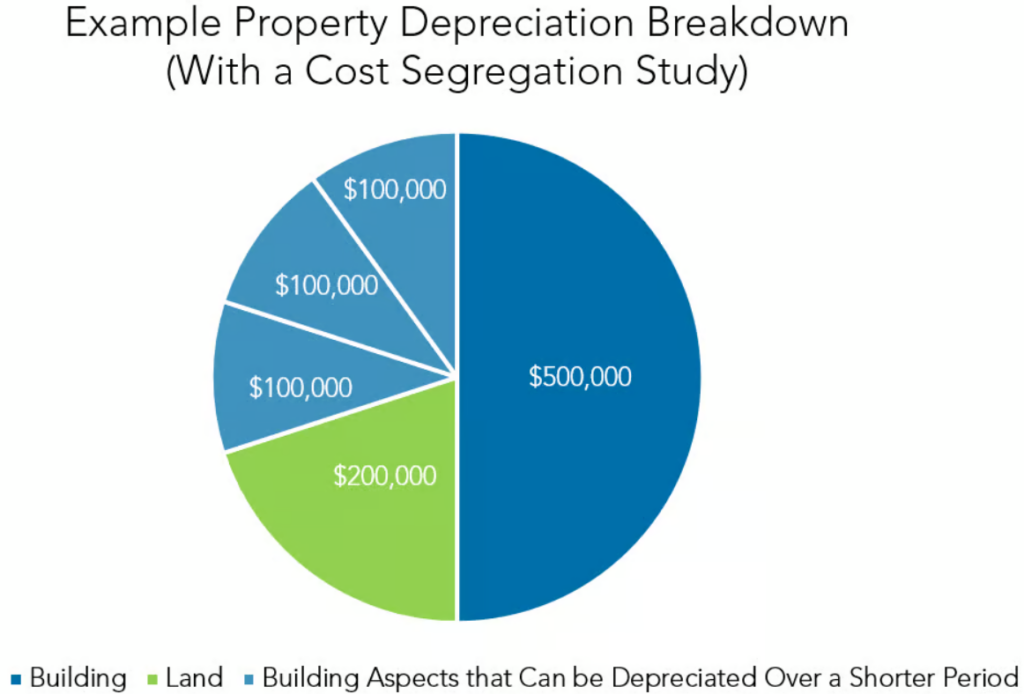

Four structural components are considered during cost segregation:

Personal property, such as furniture and carpeting, is depreciated over the next five to seven years.

Land improvements like landscaping, paving, or sidewalks are depreciated over a 15-year period .

Structures and buildings are depreciated over 27.5 or 39 years, depending on the specific type of property being dealt with .

Land assets are not depreciated at all (as land is considered to have an infinite use of life)

Cost Segregation Study example.

The primary objective of a cost-segregation study is to identify all construction-related costs – like lighting fixtures, electrical wiring, HVAC, flooring, and exterior improvement – that can be depreciated over a shorter tax life (typically 5, 7 and 15 years) than the building (either 27.5 or 39 years).

Claiming a Bonus Depreciation

In addition to accelerated and depreciation deductions, there’s an additional perk you can claim known as bonus depreciation – a governmental incentive scheme that allows for a larger depreciation deduction in the first year. The goal of this scheme is to provide new businesses with some financial relief.

To qualify for bonus depreciation, businesses need to meet specific criteria.

-

The asset must be put to use by the business. This implies that the bonus depreciation can’t be claimed until the asset is actually being used, regardless of when it was purchased.

-

The asset must be new to the taxpayer (though it doesn’t necessarily have to be brand new). For instance, if you decide to use your personal vehicle for business purposes, it wouldn’t qualify for bonus depreciation since you already owned the asset before it was used for business.

-

The asset must be owned by you. You can’t depreciate assets that you’re leasing or renting, because you don’t have a cost basis to depreciate.

Before the Tax Cuts and Jobs Act of 2017 (TCJA) was enacted, only half of the improvements made to a property could be deducted. But the game changed post-2017, with the deduction skyrocketing to 100% until 2022. Starting from 2023, this deduction will start reducing by 20% each year, eventually phasing out entirely by 2027.

Here’s a fun fact: under the TCJA, you could depreciate the entire value of gas stations and car washes in the first year itself!

As mentioned by B+E broker, Jim Ceresnak:

In many cases, car washes are eligible for the 100% Bonus Depreciation deduction in year one of ownership.

Depreciation-motivated purchasers of car washes generally seek to offset significant capital gains or other passive income on their tax bills with the generous Bonus Depreciation deduction that car wash ownership affords them.

Additional Real Estate Tax Breaks

Deductions aren’t the only incredible tax break you can get with real estate.

Deducting Business Expenses

As a real estate entrepreneur/investor, you have more than just a piece of land or a building. You also operate a real estate management company (usually an LLC filing as an S-Corp).

This means that you can write off business expenditures tied to the upkeep and management of the property, such as:

Property tax payments

Insurance fees

Costs of property management

Maintenance expenses

Utility bills

Repair costs

You’re also eligible to deduct any business-related expenditures, which might encompass things like advertising, legal and accounting services, and any necessary equipment for running the business.

Deducting Losses Against Active Income

Moreover, if you hold the Real Estate Professional Status, you can enjoy some extra perks. Most importantly, you can use deductions to reduce not just your passive real estate income (which includes rent), but you can also use it to deduct up to $25,000 of losses per year from your active income as well!

Deducting Loan Interest Payments and Debt Servicing Costs

Furthermore, the interest payments on your borrowed money are deductible. This includes interest paid on unsecured loans or credit cards used for real estate-related expenses (you should definitely consult your CPA about this).

The icing on the cake is that if you continue to enhance the investment property value, you can borrow even more money against that asset, and the cost of servicing the debt is tax-deductible. This is why real estate is such an attractive asset for the Buy, Borrow, Die strategy.

Factoring In Depreciation Recapture

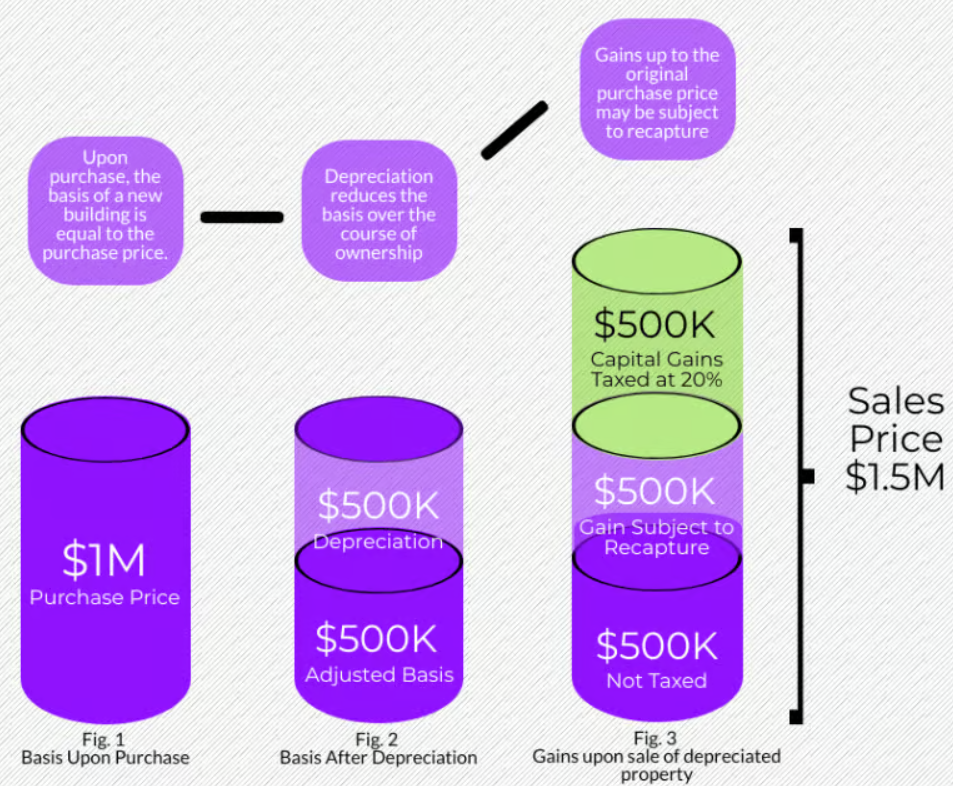

Suppose you decide that it’s time to sell your property. What are the implications?

One crucial factor to be aware of is a concept known as depreciation recapture. This comes into play when the sale price of an asset is higher than its tax basis or adjusted cost basis. The difference is then “recaptured” and reported as ordinary income for tax purposes, rather than at the more favorable long-term capital gains rate.

Illustration of depreciation recapture. Source: Lumpkin Agency

However, there’s no need to panic. The tax code provides a solution known as a 1031 Exchange, named after Section 1031 of the IRS’s tax code.

Benefits of a 1031 Exchange

A 1031 exchange gives you the opportunity to delay taxes when you sell any real estate, as long as it’s replaced with a property of a similar kind.

The 8 Steps of a 1031 Exchange. Source: Jason Kardos

If you haven’t carried out any depreciation or cost segregation, a 1031 exchange is a fairly simple process. However, the tax code doesn’t allow you to claim depreciation twice, so you’ll need to depreciate the new property to avoid depreciation recapture.

It’s highly recommended to consult with a tax expert about this, as there are many aspects to consider, and numerous potential pitfalls.

Conclusion: Tax Knowledge Is Power

Rental property owners must understand and utilize deductions related to depreciation in order for them to save substantially on taxes. With this knowledge, they can reduce their tax burden while increasing income generated from rentals. These strategies include: taking advantage of bonus depreciation, utilizing recapture deductions when it comes to deprecating a rental asset, as well as performing 1031 exchanges which allow one party to exchange like-kind properties without incurring any capital gains tax on the sale of that real estate investment.

We’ve emphasized it before and we’ll do it again: minimizing the “fee drag” is the simplest strategy to enhance your investment returns. In the majority of cases, taxes are the highest “fee” you pay on all your earnings.

Instead of pursuing high-risk opportunities with the hope of extraordinary returns, we believe it’s much easier to invest in assets that yield “regular” returns but come with some tax benefits. Keep in mind: the best investments you can make are often in your acquaintances and the knowledge you gain.

It may seem like you’re investing a significant amount of time and money upfront to assemble the right team of advisors, establish the appropriate corporate structures and tax strategies, and boost your Financial IQ.

However, if your goal is to build wealth that will last for generations, as the Insiders and Elites do, all you need to do is overcome the initial learning curve and take the first step.

As you become more confident in the asset class – and more familiar with how debt, depreciation, and tax deductions operate – you can begin to expand your investment strategy.

Frequently Asked Questions?

What is the purpose of rental property depreciation?

Property owners are able to use a tax deduction, known as rental property depreciation, to reduce their taxable income and save on taxes. Allowing them the ability to recoup costs of an income-producing asset over time.

How many years can you depreciate a rental property?

Claiming depreciation on your tax return can be done for rental property owned in the U.S. over anywhere from 3-40 years.

How is depreciation calculated on rental property?

The depreciation on a rental property can be calculated by taking the property’s cost basis and dividing it by its projected useful life. For example, if you have an initial price of $206,000 with an expected lifespan of 27.5 years, then your annual amount deducted would equate to around 3.6% or approximately $7,490 from your taxable income each year, helping reduce tax burden significantly!

Which depreciation method is best for rental property?

Straight-line depreciation is the most common approach for depreciating rental property, having been specified by the IRS. This technique of evaluating assets over time provides an easy and reliable way to calculate long-term costs associated with owning a piece of real estate.

Will 100 bonus depreciation be extended in 2023?

Though the Bonus Depreciation program has an expiration date in 2026, its first-year allowance of 80% of a purchase price is set to decrease by 2023. This cutback will remain in effect until the end of this tax incentive system’s duration.

Want to learn more about investing in private market deals?

Here at Equifund, we help investors access early-stage opportunities not found anywhere else.