Imagine being able to cram up to an additional $3.4 million into your traditional IRA over the next 10 years. No, this isn’t financial wizardry; it’s a little known retirement savings strategy known as a Cash Balance Plan – an aggressive, yet perfectly legal, method to stuff hundreds of thousands of dollars per year into a tax-advantaged retirement account.

Think of a Cash Balance Plan as the hybrid luxury car of retirement plans. It has the features of a traditional pension plan with the modern aesthetics of a 401(k)/profit-sharing plan.

For business owners looking for a retirement plan that can provide accelerated tax savings, reliable benefits and flexibility, cash balance plans could be the answer. In this article, we will take an in-depth look at what cash balance plans offer compared to other types of retirement plans—and how to leverage it to accelerate your path to financial freedom.

Key Takeaways:

Cash balance plans are a hybrid retirement plan offering a guaranteed lump sum at the time of retirement along with with tax deferral and accelerated savings.

Cash balance plans differ from traditional pension plans and 401(k)s in their individual accounts, contributions, payout options, investment risks & more.

Types of Retirement Accounts

To understand cash balance plans, we first need to understand how insiders and elites use retirement accounts to build tax-advantaged fortunes.

Quick recap: There are two types of retirement plans – Defined Benefit plans (DB plans) and Defined Contribution plans (DC plans). Defined Benefit plans offer employees a guaranteed income for life upon retirement. The amount you’ll receive is determined by factors like your salary and years of service with the company.

On the other hand, Defined Contribution plans don’t promise a set amount upon retirement. Instead, you’ll get whatever balance is in your account, which is influenced by your own contributions as well as how well your investments perform, less any fees and taxes.

As for the types of Defined Contribution plans, the most common ones include:

401(k) Plans: These are employer-sponsored retirement accounts, typically offered by private sector companies. Employees can contribute a portion of their pre-tax salary, and employers often match a certain percentage of those contributions.

403(b) Plans: Similar to 401(k) plans, 403(b) plans are geared toward employees in public education and some nonprofit sectors. Contributions are usually made with pre-tax dollars.

Traditional IRA: This is an Individual Retirement Account that allows you to make contributions with pre-tax dollars. You pay taxes on withdrawals during retirement.

Roth IRA: Unlike a Traditional IRA, contributions to a Roth IRA are made with post-tax dollars. However, qualified withdrawals during retirement are tax-free.

SIMPLE IRA: Standing for “Savings Incentive Match Plan for Employees,” this plan is intended for small businesses. Both employees and employers can contribute.

SEP-IRA: The Simplified Employee Pension Individual Retirement Account is designed for self-employed individuals and small business owners. Contributions are tax-deductible, and you pay taxes upon withdrawal.

Let’s dive further into the retirement accounts the majority of people have access to – Defined Contribution Plans.

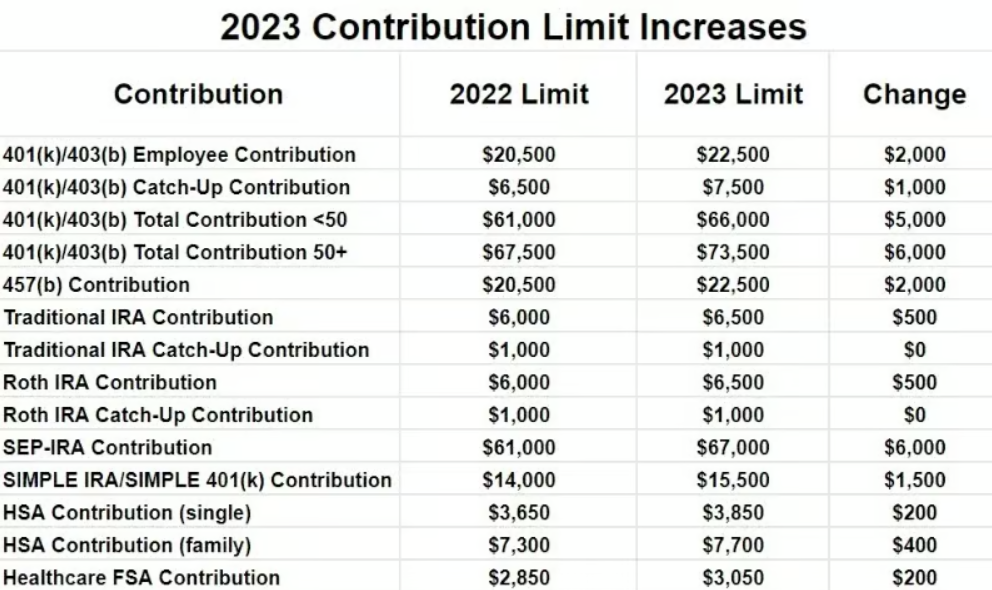

Defined contribution plan limits for 2023

Turning to Individual Retirement Accounts (IRAs), both Traditional and Roth, the annual contribution limit is $6,500. Remember, this annual contribution limit is cumulative across all IRA accounts you have, not per account. Married couples can each contribute the maximum to an IRA, given their combined income is sufficient. For minors with Roth IRAs, the contribution limit is the lesser of the child’s taxable compensation for the year or $6,500.

It’s crucial to be mindful of income limitations. If you have a high modified adjusted gross income (MAGI), your ability to contribute to a Roth IRA starts to phase out. Similarly, for those already participating in workplace retirement plans like a 401(k), certain MAGI ranges can affect your eligibility to make deductible contributions to a Traditional IRA.

In summary, DC plans offer a variety of options for retirement savings, each with its own set of rules, limits, and tax implications. The best tax breaks, however, tend to be reserved for business owners and the self-employed.

SEP IRA, SIMPLE IRA and Solo 401(k) Plans

Self-employed individuals have a variety of retirement account options to choose from, each with its unique benefits. These include SEP IRAs, SIMPLE IRAs, and Solo 401(k)s.

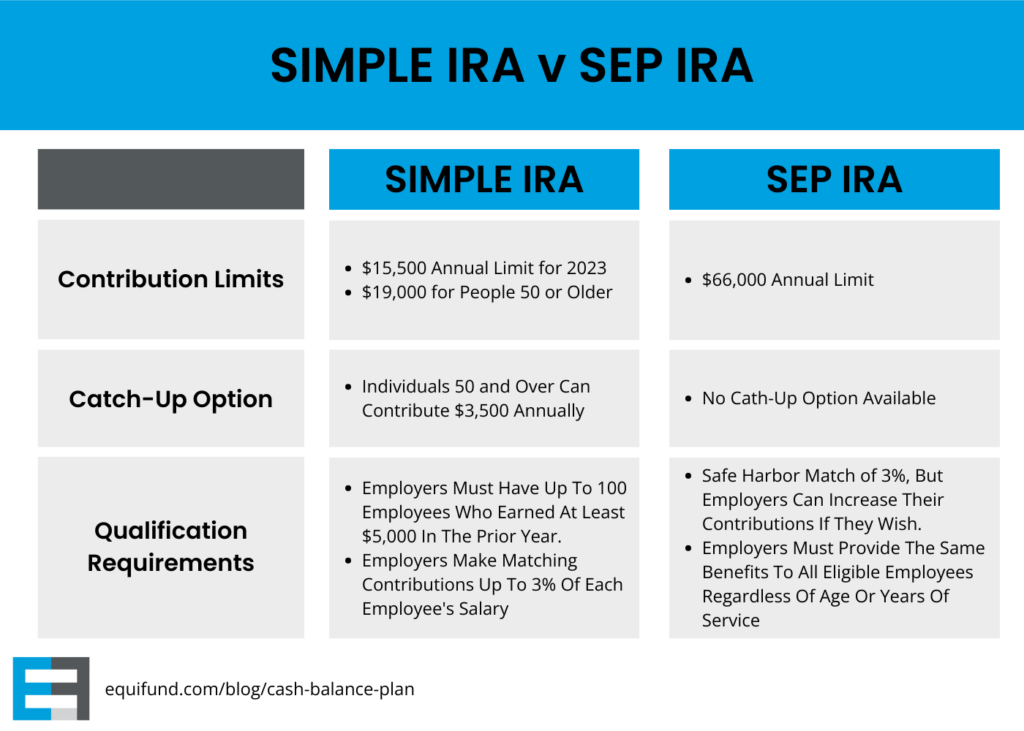

A SEP IRA allows the employer, not the employee, to make contributions directly. The maximum contribution limit for 2023 is 25% of an employee’s salary or $66,000, whichever is less.

SIMPLE IRAs, on the other hand, allow both the employee and the employer to make contributions. The 2023 limit for contributions is $15,500, with a catch-up contribution of $3,500 for those over 50, totaling up to $19,000.

Differences between SIMPLE IRA and SEP IRA. Source: Finance Strategists

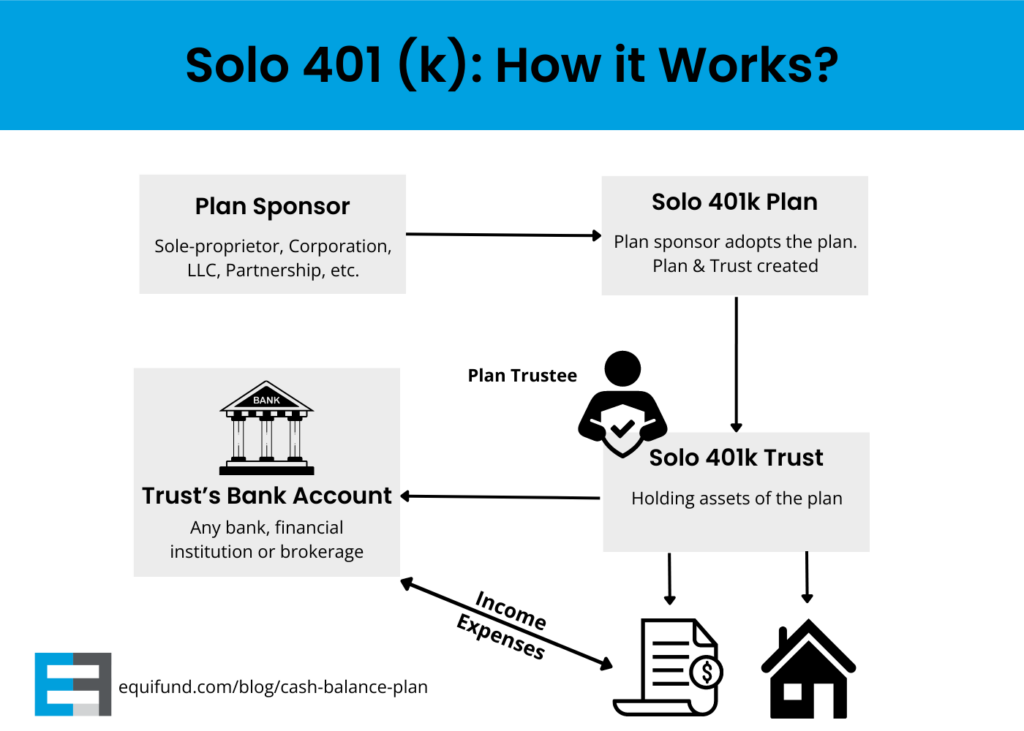

The Solo 401(k) is designed for business owners with no employees, although spouses can be included. You can contribute up to 25% of your compensation, capped at $66,000 for the year 2023. Additionally, you have the flexibility to choose between Traditional (pre-tax) or Roth (post-tax) contributions.

How a Solo 401(k) works. Source: Sense Financial

The important thing to know is that every single one of these can be turned into a Self-Directed IRA version of that plan – effectively “unlocking” your retirement funds for investments in the alternative assets you may be interested in.

The Peter Thiel Roth IRA strategy, for example, involves using your Roth IRA to accumulate tax-free gains through high-risk, high-reward investments.

An interesting advantage for business owners is the possibility of combining a Defined Contribution (DC) plan with a Defined Benefit (DB) plan into a cash balance plan. This allows you to save up to an additional $341,000 per year, with the potential to accumulate a maximum balance of $3.4 million in tax-advantaged retirement savings.

Understanding Cash Balance Plans

Cash balance plans held more than $800 billion in assets in 2012, and their popularity has surged by 70% between 2008 and 2012. So what is it, exactly?

Cash balance plans are a unique type of hybrid retirement plan combining the best of both worlds: the reliability of a defined benefit plan and the flexibility of a defined contribution plan like a 401(k). This kind of program offers a unique and highly effective approach to retirement savings, particularly if you’re a professional with a high annual salary in fields like medicine, law, or accounting.

How Cash Balance Plans Work

Cash balance plans provide a secure retirement benefit for employees—with the employer assuming all investment risks. A pay credit is calculated as a percent of the employee’s salary and added to the individual’s account balance, while interest credits are typically set at 4%. This contrasts with traditional defined benefit plans in which employers commit to granting specific benefits upon retirement without bearing any risk.

Let’s say you retire at 65 with an account balance of $100,000. You could opt for an annuity that gives you around $8,500 per year for life, or you could take a lump sum of $100,000. This lump sum can even be rolled over into an IRA or another employer’s plan that accepts rollovers.

The Pension Benefit Guaranty Corporation guarantees that cash balance holders receive all benefits due even if the Plan Sponsor runs into financial distress or insolvency situations thus securing participants’ investments, which would otherwise be lost under more standard types like defined contributions where only tax sheltering provisions exist against any losses incurred during market downturns.

Maximizing Contributions

Age-related limits in terms of contributions allow those who are more mature to give larger amounts to cash balance plans, which will mean not only sizable deductions but also greater savings potentials.

Advantages for Employers

Cash balance plans offer a range of advantages for employers, such as tax postponement, increased savings rates, plus customizable design options that can meet the exact requirements of any business owner. These plans can be integrated with other retirement planning frameworks like 401(k)s to elevate saving potential and provide greater levels of adaptability.

Who is a Good Candidate for Cash Balance Plan?

These types of cash balance plans (and their associated tax benefits) are most commonly used by physicians, accountants, lawyers, and other professionals with higher education, mainly because they reach their peak savings years later on in life, and benefit from an accelerate retirement catchup strategy.

Boosting Your Cash Balance Plan with a Life Insurance Policy

To boost the benefits of your Cash Balance Plan, consider embedding a life insurance policy within it. Here’s why it’s advantageous:

Improved Cash Flow

By housing your life insurance inside your Cash Balance Plan, you relieve the burden of using post-tax dollars for premium payments. Your company pays the premiums using pre-tax dollars, making it more cash-efficient for you.

Tax Efficiency

The premiums are tax-deductible for the company, and if your health condition increases the cost of the policy, the plan’s tax efficiency improves. According to McHenry Advisors, paying premiums outside of the plan can cost up to 79% more.

Policy Administration

You won’t have to worry about the administrative tasks related to your insurance policy. The trustee of the Cash Balance Plan takes care of it.

Beneficiary Designation

You still have the liberty to name beneficiaries, such as your spouse or children, who will receive the death benefit if something happens to you.

There are tax implications to consider, though. Because the premiums are paid with pre-tax dollars, you’ll have to recognize any economic benefits received as taxable income.

Upon retirement or plan termination, you can move the accumulated cash value to an irrevocable life insurance trust. This way, the death benefit can be structured to be free from income and estate taxes.

Comparing Cash Balance Plans to Other Retirement Plans

Differences between cash balance plans and traditional pension plans. Source: Finance Strategists

When comparing cash balance plans to other retirement options such as traditional pensions and 401(k)s, it becomes easier to recognize their advantages. Each plan has distinct features in terms of contributions, benefits structures, and investment risks that require examination for greater understanding.

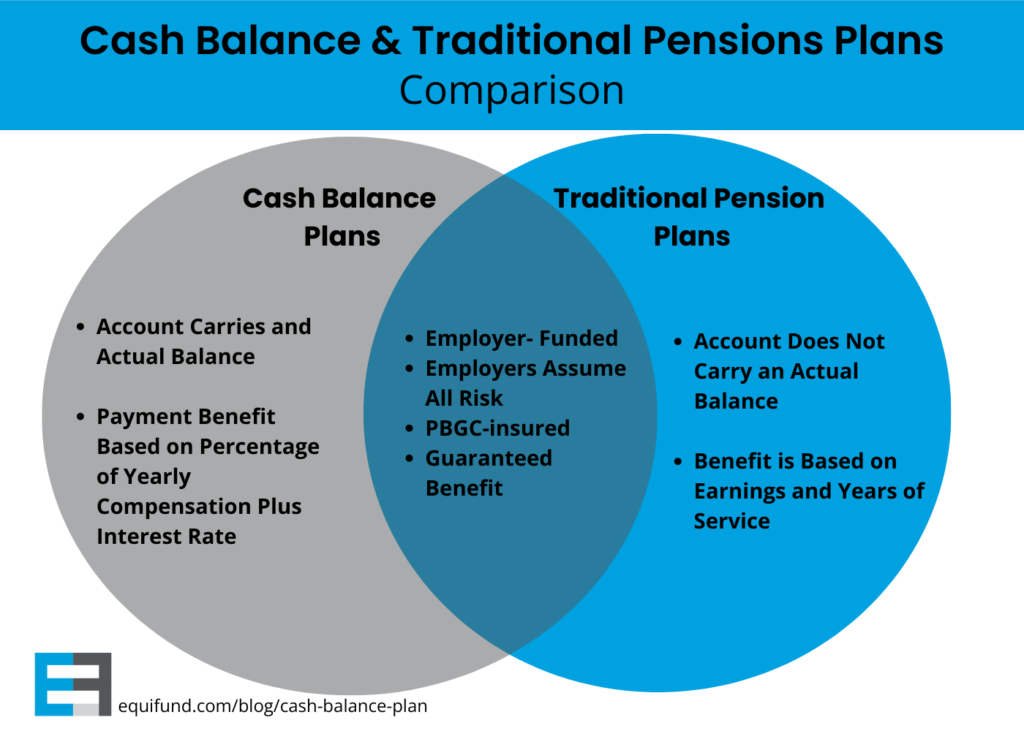

Cash Balance vs. Traditional Pension Plans

Cash balance plans and traditionally defined benefit plans are both forms of defined benefits, but they have some substantial differences. In a cash balance plan, there is an individual account that accumulates funds from contributions plus interest credits whereas the payout for a conventional pension takes into consideration elements like salary and tenure.

The payout options also differ. While one can get their money out all at once through a lump sum when dealing with a cash balance plan, retirement income is only available via monthly payments if you’re enrolled in a traditional pension plan.

Cash Balance vs. 401(k) Plans

With 401(k)’s, investment risks tend to be higher because employees usually manage it themselves, investing in stocks or mutual funds. On the other hand, cash balanced accounts offer lower levels of risk through typically conservative investments like bonds and money market funds.

Managing the Investments Inside of the Cash Balance Plan

While cash balance retirement plans offers rather significant benefits in terms of accelerated savings, because this plan will likely need to be custom created, the employer bears the burden of managing the plan’s investments inside the plan will now fall to you, the plan administrator.

While you can certainly invest these funds into low-cost publicly traded stocks, bonds, mutual funds, and ETFs… you may consider adding private market investment strategies – like private equity, private credit, and real estate – to the portfolio allocation model.

For more information on investing your retirement accounts in private markets, please go here to get our free guide.

Legal Framework and Regulations

This method revolves around capitalizing on non-publicly traded shares, typically available to a select few, usually founders, early employees, or initial investors of a company.

Understandably, to protect workers’ interests and obey the applicable laws, it’s paramount to be familiar with the legal framework and rules in relation to cash balance plans.

Fiduciary Responsibilities and Plan Management

Fiduciary and plan management responsibilities are vast, such as making sure the Employee Retirement Income Security Act (ERISA), Age Discrimination in Employment Act (ADEA) and Internal Revenue Code (IRC) requirements are followed. They include selecting service providers to assist with administering the plan properly, managing contributions into it effectively, and assuring that its assets continue to be adequately funded.

To ease up on these duties, some employers turn to third-party administrators who then manage everyday operations of their retirement plans while also ensuring compliance with federal pension laws so employee benefits remain secure.

Conversion Requirements and Restrictions

When changing to a cash balance plan, employers must alert the associated plan participants if their future benefits are going to be substantially less than they expected. Plus, any conversion of this type should not show preference based on age and all necessary funds need to remain in place for honoring each promised benefit.

Minimizing Tax Burdens with a Cash Balance Plan

Cash balance plans are a unique and advantageous savings instrument that provides the benefits of both traditional pension plans and 401(k)s, with their promise of set returns, tax-advantaged growth potential, as well as customizable designs.

Investors looking to reduce their lifetime tax burden and build generational wealth may want to consider adopting a long-term financial strategy, like a cash balance plan. This approach shifts your focus from immediate gains to sustained, compound growth over time.

However, you might also want to weigh the cost implications and administrative burden of setting up a cash balance plan by constructing a financial model. This will help you evaluate if the expected returns justify the added complexities.

Although it’s crucial to consult with a qualified financial advisor and estate planning attorney, Equifund’s high-risk early-stage offerings could be a part of a diversified portfolio within a cash balance plan—targeting potentially higher returns.

Frequently Asked Questions?

How does a cash balance plan work?

Cash balance plans are a kind of defined benefit plan that works with an individual’s hypothetically existing account, credited each year by both the employer and its interest credit rate. This account is given value through the company contribution as well as applicable interest credits which come along too.

Is a cash balance plan the same as a 401k?

A cash balance plan is a type of defined benefit plan, different from the popular 401k, which is a defined contribution scheme. Both plans may be offered by an employer to their staff. There are distinct differences between them. Cash balance reply on the accumulation of funds while 401ks rely on investment gains for accrual of value over time.

Is a cash balance plan a good idea?

When it comes to retirement savings, a cash balance plan can be an effective tool. Before jumping into this type of plan, individuals should look closely at the requirements and expenses associated with them, such as contribution limits, vesting rules and any fees that may apply. Understanding these details is key in order for someone to make the most out of their cash balance account.

Can I cash out my cash balance plan?

You can start withdrawing from the cash balance plan when you reach retirement age, or 59 1/2.

However, if you take an early withdrawal before then you’ll have to pay taxes plus a 10% early withdrawal penalty. It’s usually advised to roll the funds over into an IRA and then follow the IRA rules.

How does a cash balance plan differ from a traditional pension plan?

A cash balance plan is a type of retirement program that combines the advantages of defined contribution plans and traditional pension schemes. It promises participants an guaranteed lump sum distribution at their time of retirement. Regular pension arrangements, on the other hand, pay out monthly salaries based on length of service.

Want to learn more about investing in private market deals?

Here at Equifund, we help investors access early-stage opportunities not found anywhere else.