Ever wondered how retirement savings accounts, originally meant for middle class earners, turned into a financial powerhouse for the ultra-wealthy?

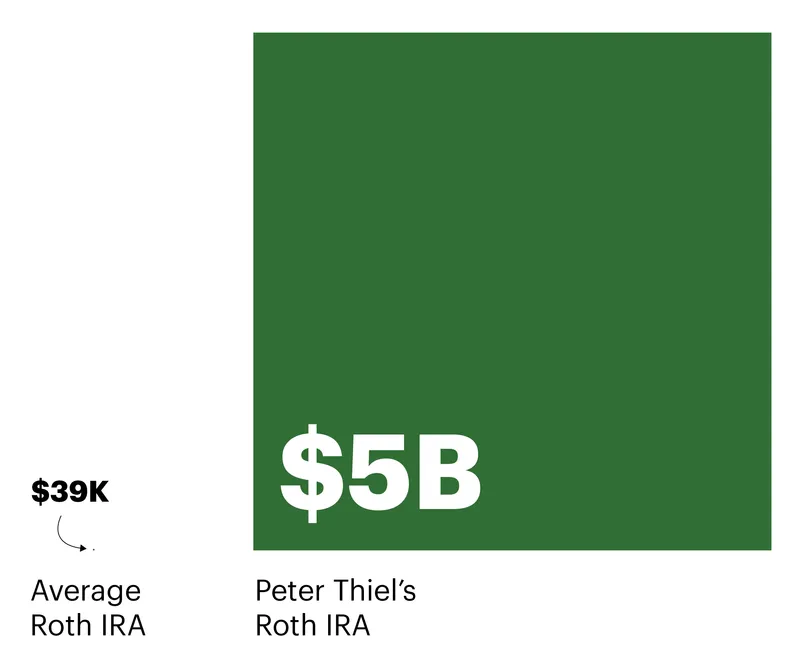

The most notable example of this is co-founder of PayPal and venture capitalist icon Peter Thiel—who managed to grow his Roth IRA from a mere $2,000 in 1999 to a staggering $5 billion tax-free fortune today.

And he’s not alone. The U.S. Government Accountability Office, using 2011 tax data, identified close to 8,000 taxpayers with Roth account balances exceeding $5 million. Fast forward to 2019, and this number skyrockets to over 28,000.

Dive deeper, and you’ll find 497 of these individuals holding a jaw-dropping average of $150 million in their IRAs. The secret? Tapping into private market investments that aren’t typically accessible through a standard IRA or 401k. In this article, we’ll explore the three strategies for building your own Mega IRA like Peter Thiel.

Key Takeaways:

-

Peter Thiel Roth IRA: This strategy is all about investing in high-growth companies through a tax-advantaged account. In 1999, Thiel scooped up 1.7 million PayPal shares for $1,700. By 2002, Thiel’s shares were worth $55.5 million.

-

Investment Vehicles: Non-publicly traded shares and partnership interests are two commonly used investment vehicles for building Mega IRAs.

-

Tax-Efficient Wealth Creation: Another ingenious way Insiders and Elites accumulate wealth in a tax-efficient manner is the Buy, Borrow, Die strategy. This essentially involves buying appreciating assets like stocks or real estate, borrowing against them, and then leaving these assets to heirs, often avoiding capital gains taxes.

A Brief History of the Roth IRA Account

When the Employee Retirement Income Security Act (ERISA) was passed in 1974, it transformed the way private-sector retirement plans were regulated. Aimed at enhancing protections for employee pensions, ERISA brought about the inception of the IRA, among other retirement vehicles. Yet, even with its broad-reaching influence, the traditional IRAs that emerged in the 1970s were restrictive in terms of investment choices, generally limited to stocks, bonds, and mutual funds.

However, as investors looked beyond the stock market for diversification and higher returns, they began eyeing alternative assets like real estate, private equity, and even artwork.

“I have seen a lot of interesting strategies that investors have used to create enormous gains inside their IRA. In my experience, the most successful strategies involve the investor investing in an asset they know well.

Whether it’s a horse, a house, or private company stock, if the investor is an expert in that asset, they [may] have a sizable advantage over other investors in the market.”

Although traditional IRAs couldn’t readily accommodate these alternative investments, the demand for them became undeniable. A pivotal shift came in the 1980s when independent firms pursued non-bank trustee status, enabling them to hold IRA accounts that could invest in these alternative assets.

Yet, it was the introduction of the Roth IRA through The Taxpayer Relief Act of 1997 that truly laid the groundwork for the concept of self-directed IRAs (SDIRAs). Unlike its traditional counterpart, Roth IRAs offered after-tax contributions with the appealing advantage of tax-free qualified distributions. More than that, they paved the way for investments in a wider array of assets.

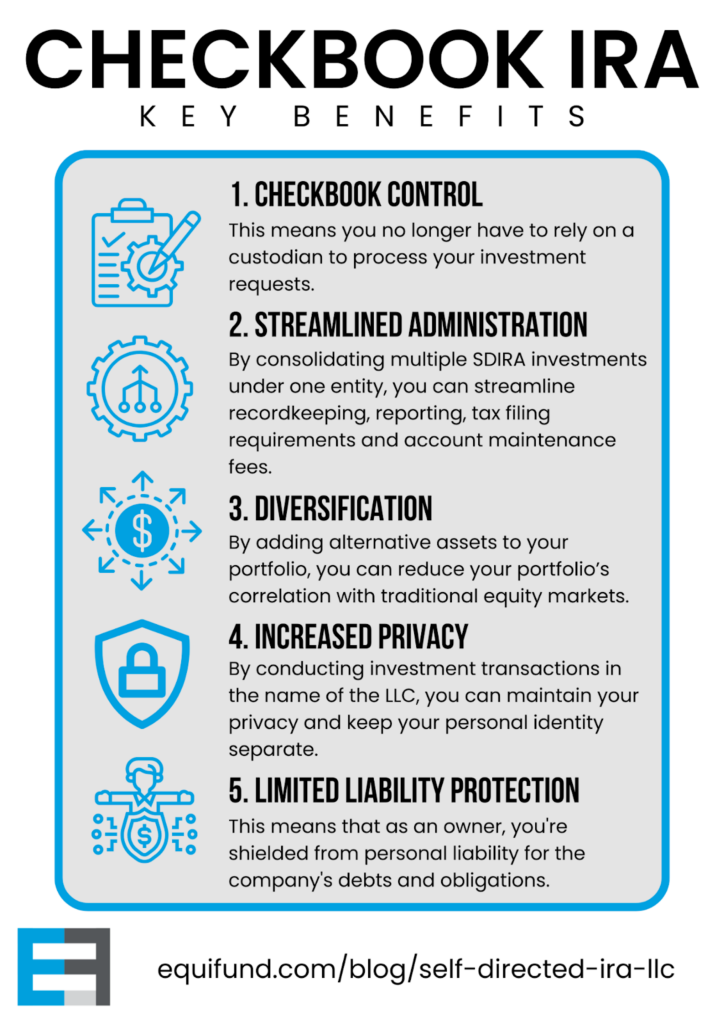

The most groundbreaking development for SDIRAs was the advent of the Self-Directed IRA LLC, popularly known as the “Checkbook IRA”. Instead of navigating layers of bureaucracy and waiting on custodians for every transaction, this structure provided investors with direct access to their funds. Essentially, if you owned one, you could cut a check or execute electronic transactions straight from the LLC’s bank account, streamlining the investment process.

Key benefits of a Checkbook IRA.

A landmark case, Swanson v. Commissioner in 1996, further solidified the standing of SDIRAs. It underscored the legality of using an LLC owned by an IRA for real estate investments, offering clarity on the IRS’s stance.

In the grand tapestry of retirement investments, SDIRAs emerged as a powerful tool for savvy investors, weaving together the flexibility of alternative assets and the tax advantages of IRAs. And as the case of Peter Thiel’s Roth IRA will show, when maneuvered skillfully, these vehicles can drive significant wealth accumulation.

The Peter Thiel Roth IRA Strategy

Peter Thiel Roth IRA compared to average Roth IRA. Source: ProPublica

Peter Thiel’s Roth IRA strategy, is all about investing in high-growth companies through a tax-advantaged account. In 1999, Thiel scooped up 1.7 million shares at the par value of just $0.001 per share. That’s a modest investment of $1,700. When eBay acquired PayPal in 2002 for a whopping $1.5 billion, Thiel’s shares translated to an impressive $55.5 million return.

But Thiel didn’t stop there. He reinvested, putting $500,000 into a then-little known company named Facebook. That investment ballooned to approximately $1 billion (and now stands at an estimated 5 billion dollars), all neatly tucked away in a tax-free Roth IRA.

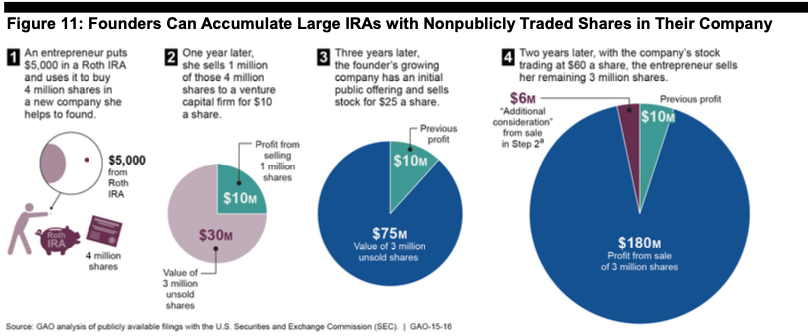

Founders can accumulate large IRAs with nonpublicly traded shares in their company. Source

This extraordinary 5 billion tax free gain underscores the importance of holding investments like these within a Roth setup—where you pay taxes up-front rather than on withdrawal later down the line when values could have increased significantly.

Achieving a Mega IRA Like Peter Thiel

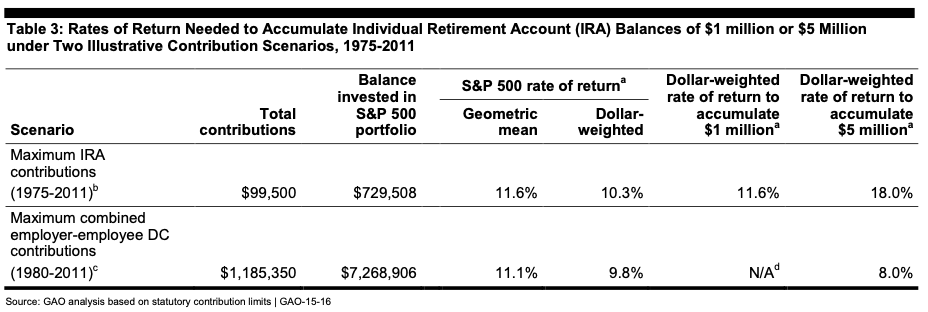

To grasp how someone might amass a Mega IRA worth more than $5 million, we first need to understand the basic math behind reaching a $1m to $5m retirement account. Let’s dive into the numbers:

The math behind $1m to $5m IRAs. Source

Annual Contribution Limits

For 2011, individuals could contribute a combined maximum of $54,500 to their retirement accounts. This is the sum of both the employer’s and the employee’s contributions. For those aged 50 and older, they could play catch-up and contribute an additional amount, bringing the individual’s contribution limit to $22,000.

Maxing out Contributions

The assumptions made so far are quite aggressive. The truth is, very few individuals max out their IRA or Defined Contribution (DC) plan in any given year. Even rarer is the individual who does this for three decades straight.

Return on Investment

Even if someone were to make only IRA contributions and max them out, the report from the GAO points out they would need returns in the double digits—more than the S&P 500 average—to even hit the $1 million mark.

The DC Plan Scenario

If one were to make the maximum possible combined contributions (from both employer and employee) and refrained from making any withdrawals, and did this for over three decades, they could, in theory, accumulate a balance surpassing $5 million. However, as we’ve seen, such consistent contributions over such a long period are rare.

Investment Vehicles

Such a massive accumulation looks even bigger when you compare it to typical rollovers from employer Defined Benefit (DB) plans.

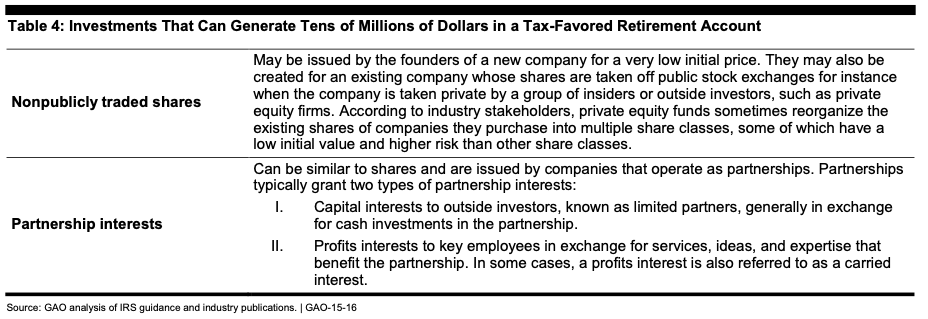

You might wonder, “Given these obstacles, how then does one amass a Mega IRA?” This is where the strategies employed by insiders and elites come into play. The answer lies in investing in non-publicly traded shares and partnership interests. Let’s explore how they work.

Investments that can generate tens of millions of dollars in individual retirement accounts. Source

Investing in Non-Publicly Traded Shares Like Peter Thiel

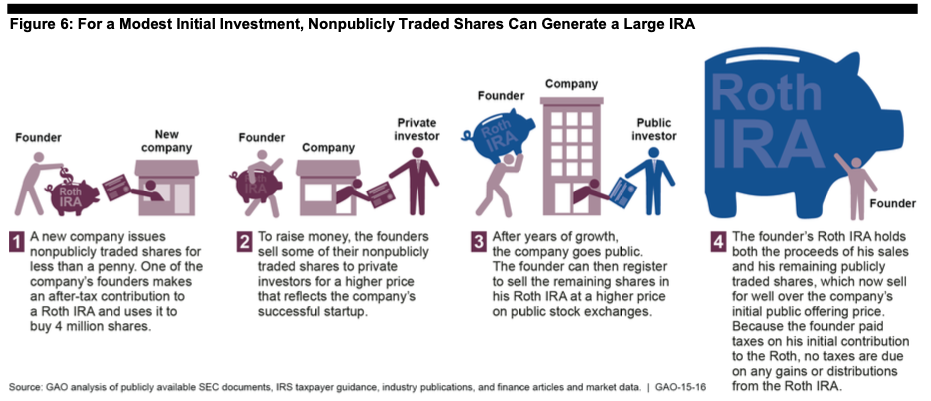

This method revolves around capitalizing on non-publicly traded shares, typically available to a select few, usually founders, early employees, or initial investors of a company.

How Nonpublicly traded shares can generate a large IRA. Source

Here’s how it works:

1. Gain Limited Access

It’s essential to note that these shares, being non-public, are not available to the general public. Only a handful, often those involved in the inception of the company, have the privilege to acquire these shares.

2. Acquire Shares

To truly magnify your returns, you need to invest at a ground floor level, often when a company is just a fledgling start-up. These shares are typically available at a ‘par value’, which can be as low as $0.001 per share or less. This low valuation is where the magic starts.

3. Capitalize

The game’s name is patience. If and when these startups blossom into thriving businesses or get acquired for big bucks, the valuation of your shares skyrockets. The key is to cash in at the right moment.

Building a Mega IRA with Private Equity

The realm of private equity (PE) offers a fascinating opportunity to supercharge your IRA, similar to the “Peter Thiel Roth IRA” strategy. Here’s a simple breakdown:

Access to Unique Share Classes

Private equity funds often have varied share classes. To explain this, we can borrow from the “cheap stock model” as described in the GAO report. In this model, there are typically two share classes:

Preferred Share Class: This has a higher initial value and is considered less risky.

Common Share Class: This is the lower-valued, riskier one. But it’s where the real magic can happen. For example, in one publically reported PE transaction, employees in a PE firm used their IRAs to invest about $25,000 in such low-valued shares of a portfolio company.

In less than 2 years, when the company went public again, these shares’ value skyrocketed to nearly $14 million. Ultimately, the employees cashed out with over $23 million, marking an astounding return of more than 1,000 times their initial investment.

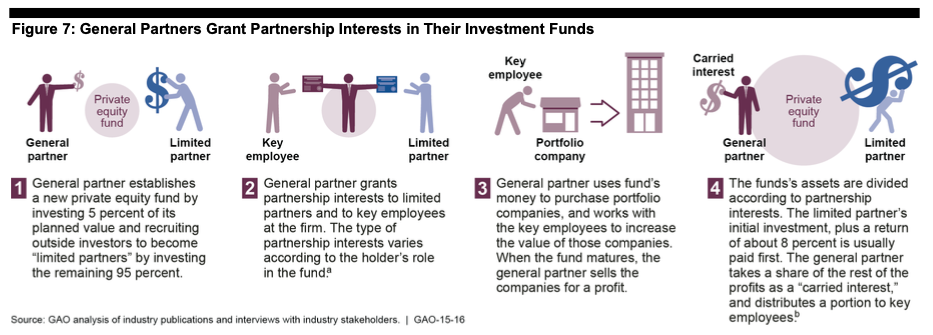

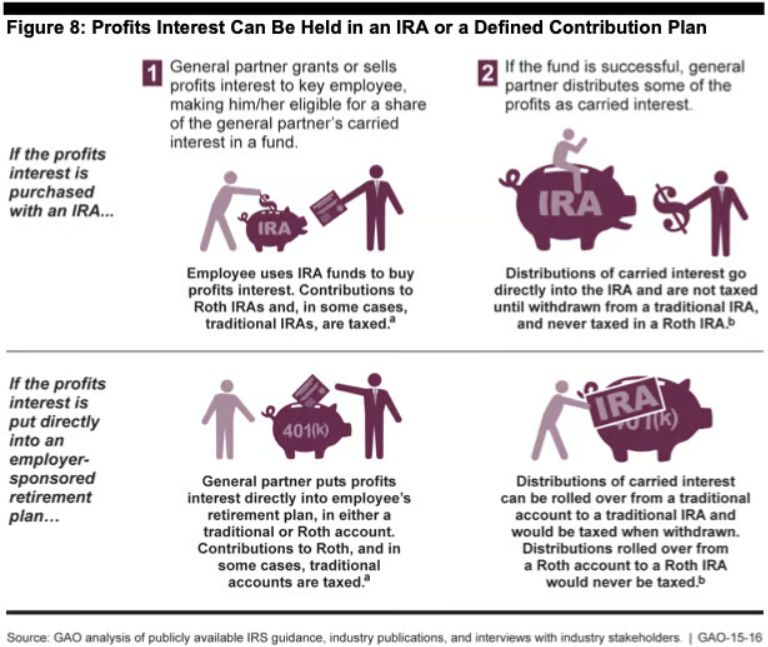

Securing Carried Interest

Beyond the shares, if you’re strategically positioned in a PE firm, you might also have a shot at the “carry”, or carried interest. This is a performance fee that the general partner (or the main entity managing the private equity fund) receives. Here’s how it can play out for you:

How GP’s grant partnership interests in their investment funds. Source

The general partner often distributes a part of this fee to select key employees. This is done by granting these employees a “profits interest” in the fund. Interestingly, this profits interest can sometimes be valued as low as $0.00. This might sound strange, but it’s because these interests aren’t cash investments into the fund by these employees.

Instead, they’re agreements. Essentially, the employees are promising to bring their expertise, innovative ideas, and hard work to ensure the fund’s success. In return, they get a slice of the fund’s profits. The best part? When these profits interests are granted, they’re treated as a nontaxable event.

So, if you’re within the corridors of a private equity firm,you can leverage the right share classes and carried interest, to emulate a “Peter Thiel Roth IRA” approach.

Investing Through Alternative Investment Platforms

But what if you don’t work at a private equity fund and have no access to the carry? Your third and final option is to invest in private offerings on alternative investment platforms like Equifund. While you may not be able to acquire “cheap shares” or profit interests in your account, you may have the opportunity to invest early in promising companies that could deliver above market returns.

Comparing Roth IRAs and Traditional IRAs

How profit interest can be held inside an IRA or DC plan. Source

When contemplating which type of retirement account to invest in, it is important to fully understand the differences between Roth IRAs and Traditional IRAs. These accounts differ based on tax breaks available as well as requirements for contributions and eligibility. A Roth IRA provides a great advantage because all growth within these investments will be entirely free from taxation when withdrawn during retirement, whereas with a traditional plan, any income taxes due must still be paid upon withdrawal.

Income Tax Advantages

Roth IRAs provide tax-free growth and withdrawals, making them an attractive option for those looking for ways to reduce taxes in their retirement. Comparably, Traditional IRAs offer the advantage of tax deductible contributions leading to deferred taxation on future earnings as well as withdrawals. This suggests that while Roth may ultimately lead you to pay income tax but towards a lower overall taxable amount during your senior years, traditional IRS can help offset some of your current income levels by providing deductions off the top before any taxing takes place.

Contribution Limits and Eligibility

When it comes to Roth IRAs and Traditional IRAs, not only are the contribution limits different, but also eligibility requirements. Both of these retirement accounts have a $6,000 limit for 2021 or $7,000 in case individuals aged 50+ wish to make contributions. When deciding on which type is best suited for them, one must consider that while Roth has income restrictions as part of its criteria, Traditional does not impose such limitations. Understanding both options before committing funds into any form of savings plan is essential.

The Senate Finance Committee’s Response to Mega IRAs

The Senate Finance Committee has expressed concern over Mega Roth IRA accounts, which are funded with post-tax money, such as Thiel’s.

Concerns Over Tax Revenue Loss

Worries of policymakers stem from the possibility that high-income individuals may take advantage of Roth IRA tax benefits to avoid paying taxes themselves, leading to a severe depletion in tax revenues at a time when economic disparity is escalating and budget deficits are rising. Concerns have also been raised regarding the potential for misuse with regards to evading taxes through Roth IRAs.

Potential Policy Changes

Policymakers may consider amendments to contribution amounts, qualification requirements and tax benefits related to Roth IRAs in order to quell any worries. This could involve capping contributions at a certain level, like $5 million, or mandating account holders take out sizable funds from their accounts. Such alterations seek both maintaining the intent of aiding middle class families with these Roths as well as avoiding taxes being avoided using such plans.

Final Thoughts on the Peter Thiel Roth IRA

The allure of the Roth IRA, especially when we see high-profile figures like Peter Thiel amass significant tax-free gains from audacious stock plays, is undeniable. However, it’s crucial to remember that these strategies aren’t one-size-fits-all.

For the average American, the Roth IRA provides a valuable tool for saving for retirement. Still, diving headfirst into high-risk, high-reward ventures requires careful consideration. Wealthy individuals can afford to offset losses through a myriad of other transactions – a safety net that might not be available for most. Moreover, when you use a Roth IRA, you’re saying goodbye to any potential tax deductions from investment losses, which can be a significant benefit in a taxable account.

Additionally, there’s the not-so-small matter of costs. Setting up a Self-Directed IRA (SDIRA) comes with its own suite of fees, from account opening and closing fees to transaction fees and everything in between. And if we remember that these businesses aren’t operating as charities, the potential to see significant portions of your savings disappear in fees becomes a genuine concern. This problem is exacerbated for those with smaller account sizes.

In summary, while the Roth IRA’s potential is great, it’s not a vehicle that should be driven recklessly. The average American should tread carefully, bearing in mind both the opportunities and pitfalls. And, as always, seeking guidance from a qualified financial advisor is paramount. They can provide clarity on which investment strategies align best with individual retirement goals and financial circumstances.

Frequently Asked Questions?

How much does Peter Thiel have in his Roth IRA?

Peter Thiel has accumulated a net worth of $5 billion over the past twenty years, thanks to his Roth IRA investments.

What did Peter Thiel do with Roth IRA?

In 1999, using the tax advantages of a Roth IRA, Peter Thiel managed to transform an initial investment of $2,000 into an impressive net worth of approximately 5 billion dollars by 2019. This allowed him access to his retirement savings without having to pay any taxes once he turns 59 1/2 and takes advantage of said Roth benefits.

What are the contribution limits for a Roth IRA?

For 2021, those who are 50 or older can contribute up to $7,000 into their Roth IRA based on taxable income. For individuals under the age of 50, the contribution limit is set at $6,000 for a Roth account.

Want to learn more about investing in private market deals?

Here at Equifund, we help investors access early-stage opportunities not found anywhere else. To view our current listings, go here now.