If you found that issue intellectually interesting – but somewhat lacking in real world application – today’s issue marks the beginning of a multi-part series on the Worldviews of the top private equity firms.

Why? Because in one of our inaugural issues of Private Capital Insider, I promised…

To provide everyday investors with an inside look at the major trends and opportunities we’re seeing unfold in Private Capital Markets…

The moves being made by the players in Private Capital…

And a look at the new wave of “alternative” investment products being launched, specifically for retail investors.

While I think we’ve done an admirable job of covering foundational investor education topics, discussing Wall Street’s push to raise capital from retail investors, and some of the various challenges we’ve seen from new retail-focused alternatives (like the Blackstone Real Estate Trust)…

We haven’t done much by way of providing coverage on what the top private equity firms are up to…

How these institutional investors think about investing…

And why we think it’s useful to understand the Worldviews of the largest – and most powerful – investors on the planet today.

Let’s dive in,

-Jake Hoffberg

P.S. Today’s edition builds off the foundational investment philosophy we discussed in the January 17th (Searching for “Truth” in Early Stage Investing) and the January 25th (Turning ideas into investments (that hopefully make money) editions of Private Capital Insider.

P.P.S Looking for back issues of Private Capital Insider?

A Quick Primer on Publicly Traded Private Equity

We’ve briefly discussed publicly traded private equity investment opportunities – called “Semi Liquid Private Funds” (SLPFs) or “listed private equity” – here.

And while you might gain a technical understanding of how these financial products are structured…

We’re going to focus primarily on why a successful private equity firm would go public in the first place.

After all, why would a manager of what is arguably the most profitable business model in capitalism open their doors to the public markets?

Simply put, they go public for many of the same reasons privately held companies do…

- Providing liquidity to general partners (and other shareholders)

- Greater access to capital (especially from retail investors)

- Opportunities to expand their business into other financial services (or other fund strategies)

Historically speaking, we’ve seen various versions of SLPFs – often in the form of business development companies (BDCs), real estate investment trusts (REITs) and master limited partnerships (MLPs).

For those who are unfamiliar with these structures, in exchange for a reduction or elimination of corporate taxes, the fund must distribute at least 90% of their income to shareholders.

Generally speaking…

- MLPs tend to focus on acquiring cash-generating assets backed by oil and gas properties or pipelines

- REITs are focused on acquiring cash-generating real estate properties, and

- BDCs are considered specialty finance companies, and primarily make investments in the debt and/or equity of small- to mid-sized companies, predominantly in the U.S.

In form and function, a BDC is the closest “cousin” to a traditional private equity firm.

Created by Congress in 1980, the primary requirements for being registered as a BDC are for a firm to invest 70%+ of its assets into non-public companies worth $250 million or less, and to distribute 90%+ of income to investors.

As you might conclude from this requirement, BDCs were designed to provide small(er) companies access to capital (note: the SBA’s SBIC program is also an example of the push to provide access to capital for small firms).

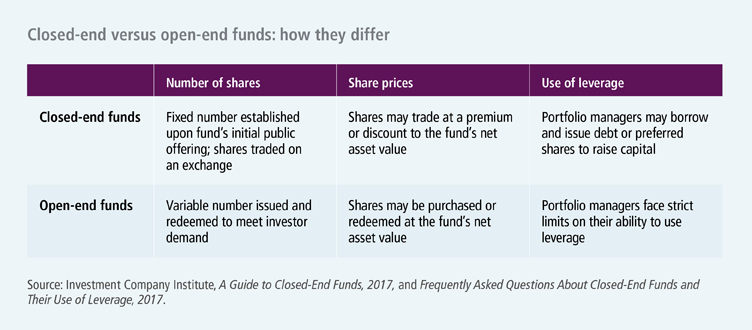

Structurally speaking, a BDC is a closed-end fund (CEF).

While private equity funds are typically also CEFs, we’re seeing many of the newer publicly listed private equity vehicles structured as interval funds – which is more of an “Open/Closed” hybrid than a true CEF.

An open-ended fund structure has historically been more common in hedge funds or other funds, where the underlying investments are highly liquid in nature (e.g., public securities), to allow for investors to redeem their interests, or otherwise exit their position.

For the sake of brevity, we’re not going to go into the nuances of these structures, and instead focus on the value propositions of listed private equity.

As a quick refresher, the actual private equity firm – considered the General Partner (or GP) – is compensated through a combination of:

- Management fees (usually 2% of capital committed, per year) – Open-ended funds typically charge management fees based on either invested capital or the net asset value (or “NAV”) of the fund. In contrast, closed-ended funds most often charge management fees based on capital commitments during the investment period and invested capital thereafter

- Carried interest (usually 20% of the net profit), and

- Various transaction fees (i.e., any other way they can charge fees)

On the other side of this split are the Limited Partners (called LPs).

As you might imagine, if you had to choose between the guaranteed returns the GP gets, or the speculative returns the LPs get, you’d probably want to own a piece of the GP’s business, right?

That’s exactly what you get to do when you invest in listed private equity – a chance to participate in the GP side of the equation (which is also referred to as “GP Stakes”).

This means that an investor in an SPLF benefits when the GP generates more fee income from its LPs.

From a tax perspective, BDC investors get a 1099-DIV, while private equity shareholders receive a K-1 form for being a member of a partnership.

While there is an obvious conflict of interest inherent to this business model…

Interval funds, non-traded CEFs, non-traded BDCs, and non-traded REITs are all slightly different, and all make up the “semi-liquid” structure space currently capturing allocations from wealth management firms.

These structures aren’t an asset class unto themselves, but a “vehicle” for investing into a specific strategy or otherwise gain exposure to an investment thesis.

This, according to Hubbis, provides investors with “a tantalizing, hybrid private markets offering, combining illiquid long-term asset classes with the allure of liquidity.”

Blackstone, Starwood, Apollo, Carlyle, KKR, Blue Owl, Lord Abbett, Nuveen, First Eagle, JPMorgan Asset Management, Allianz Global Investors, EQT, and Ares are some of the top institutional managers that have joined the space of “semi-liquid” vehicles in recent years.

While we can debate exactly how liquid these investment vehicles actually are – as we’ve already seen redemption issues with the Blackstone REIT in 2023…

Because interval funds are required to register as a “40 Act Fund,” they have reporting and operational requirements that provide greater transparency compared to non-traded funds.

Although BDCs and REITs are regulated under different provisions of the 1940s Act, they are similar to interval funds in the sense that they may offer liquidity provisions in their non-traded vehicles, and the funds are registered with the SEC.

And with that in mind, let’s turn our attention to our first publicly traded private equity firm…

KKR: The Barbarians at the Gate

For fans of the movie Wall Street, you probably remember Michael Douglas’s role as Gordon Gekko – a corporate raiding investment banker.

While the character isn’t based on any single person in particular…

Henry Kravis – co-founder of Kohlberg Kravis Roberts & Company (KKR) – is behind some of the biggest private equity deals in history.

The firm is also famous for their controversial leveraged buyout of RJR Nabisco, a deal so controversial that it became the subject of the book and movie “Barbarians At The Gate.”

While there’s plenty of fun stories of greed and glory in KKR’s past, let’s fast forward to its pathway towards becoming a listed private equity firm.

In May 2006, Kohlberg Kravis Roberts raised $5 billion in an initial public offering for a new permanent investment vehicle (KKR Private Equity Investors or KPE) listing it on the Euronext exchange in Amsterdam (ENXTAM: KPE).

KKR raised more than three times what it had expected at the outset as many of the investors in KPE were hedge funds seeking exposure to private equity but could not make long-term commitments to private equity funds.

While the fund showed lackluster first-day performance – which caused several other firms to shelve their potential listings – it was a historic moment none the less.

On March 22, 2007, the Blackstone Group filed with the SEC to raise $4 billion in an initial public offering, making it the first US-based private equity manager to do so.

Less than two weeks later, KKR filed with the SEC in July 2007 to raise $1.25 billion by selling an ownership interest in its management company… offering investors, for the first time, a “GP Stakes” in the firm.

However, due to a variety of reasons, the offering was repeatedly postponed – in 2010, the firm finally listed on the New York Stock Exchange, trading under the symbol “KKR” – up 315% since inception.

Based on KKR’s website, they currently have three funds to choose from.

- KKR Income Opportunities Fund (KIO) – Launched July 26, 2013, the Fund’s primary investment objective is to seek a high level of current income with a secondary objective of capital appreciation. The Fund will seek to achieve its investment objective by investing primarily in first- and second-lien secured loans, unsecured loans, and high yield corporate debt instruments.

- KKR Credit Opportunities Portfolio (KCOP) – Launched February 28, 2020, the Fund provides individual investors access across the institutional KKR Credit platform for the first time through a single investment. The Fund allocates across opportunities in credit to seek the best relative value opportunities.

- KKR Real Estate Trust (KREST) – Launched May 21, 2021, the Fund intends to invest primarily in thematically-driven, income-generating commercial real estate, prime single tenant real estate, and private real estate debt and preferred equity interests in the U.S., with a flexible mandate to invest globally, including developed markets in Europe and Asia.

If you want to research more about those specific products, please be sure to check out the investor relations materials provided by the firm…

But to get to the whole point of today’s issue, let’s dive into the most recent publications coming from KKR regarding their Worldview and Investment Thesis for 2024 and beyond.

The “Regime Change” Thesis

While any analyst at any firm can publish – theoretically – whatever their opinion is…

One of the things I’ve learned over my years as a financial ghostwriter is to look at how the firm’s viewpoint has changed over the years – and how accurate their forecast were.

Spoiler Alert: it’s really hard to predict the future and forecasts are often wrong.

With that said, in order to perform any sort of underwriting and due diligence, you must start with assumptions, and then focus on the outcomes those assumptions predict.

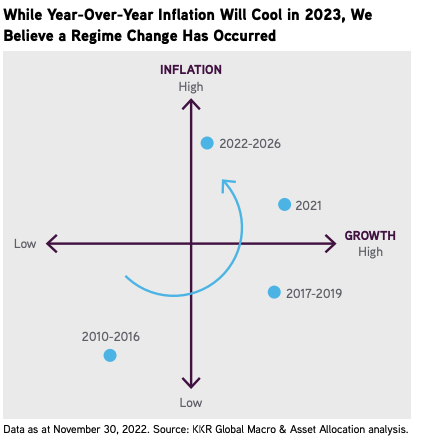

Today, you’ll find KKR is touting their “Regime Change” thesis, which is a relatively straightforward idea. According to the firm in May 2022,

We believe that we are entering a new environment for investing, an environment where structural forces – in particular the changing structural relationship between stocks and bonds – demand a new approach to portfolio construction.

Key to our thinking is not only are forward returns likely to be lower for risk assets such as Public Equities, but also traditional Fixed Income may no longer serve as a shock absorber, or diversifier, when paired with other asset classes in a diversified portfolio.

Against this more challenging backdrop, however, we still believe that there are compelling opportunities to build upon a traditional ‘60/40’ portfolio to deliver attractive risk-adjusted-returns in the environment we envision.

Specifically, we think that adding asset classes such as Private Real Estate and Private Infrastructure can enhance the Equity part of the ‘60’ portfolio, while Private Credit can bolster the ‘40’ segment of the Fixed Income portfolio.

Since the firm began pounding the table on this thesis, we’ve had a chance to watch some of these ideas play out in real time.

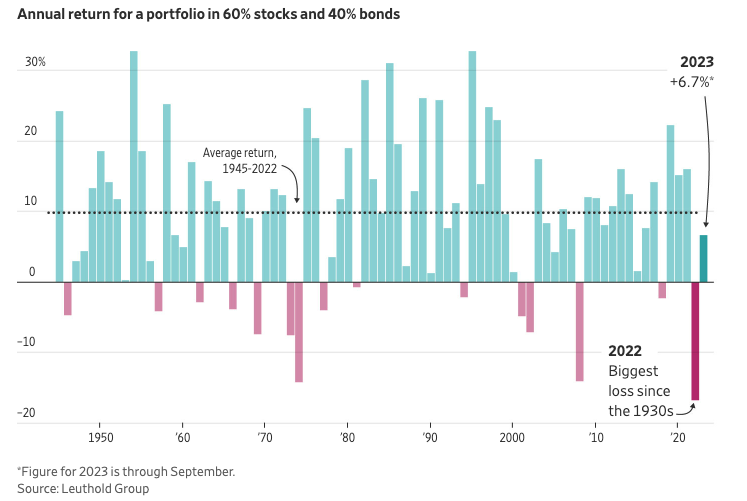

In 2022, not only did the 60/40 portfolio have its worst return in something like 100 years…

Depending on exactly what you count as inflation, we arguably started to see the year-over-year inflation cool in 2023 as well, as forecasted by the chart below.

As we move forward into 2023, the firm continues to publish more on their Regime Change thesis. In March 2023, the firm said,

We have proposed – given this new environment – that investors consider pursuing two main objectives aimed at improving their asset allocation. They are, in order of importance:

1. Increasing inflation protection by adding more Real Assets, given our house view that there will be a higher resting rate for inflation this cycle; and

2. Improving the robustness of a diversified portfolio by adding private Alternatives, including more floating rate private debt (e.g., Private Credit) and Real Assets, based on our belief that the established relationship between stocks and bonds that exists in a traditional 60/40 portfolio has now changed.

While there has been plenty of hype around Private Credit from asset managers everywhere…

KKR adds much needed color to the discussion around Private Equity’s role in asset allocation. According to the firm,

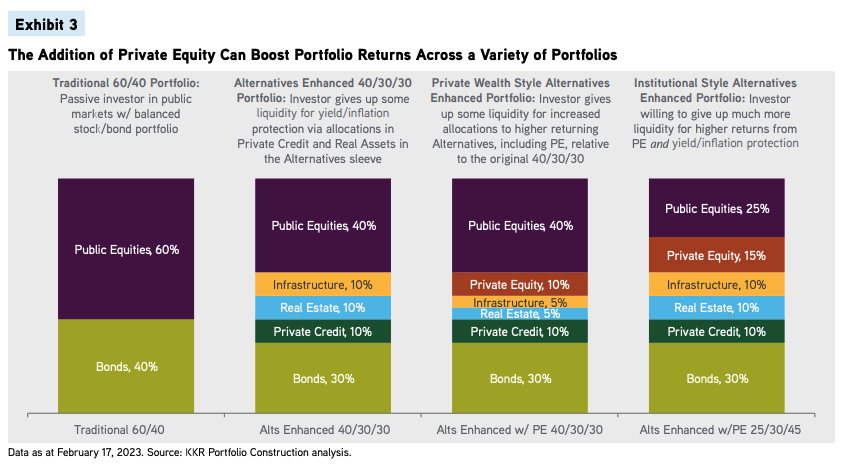

We recognize that a 45% allocation to Alternatives (i.e., the Institutional style portfolio), which is the level many more established endowments, family offices, and pensions are targeting in their asset allocation frameworks, might feel too lofty for those who place a higher premium on liquidity.

As such, we decided to think about a total allocation towards Alternatives of 30%, including Private Credit, Real Assets, and Private Equity.

One can see this more Private Wealth style portfolio, which includes an Alternatives bucket of 10% Private Equity, 5% Real Estate, 5% Infrastructure, and 10% Private Credit, in Exhibit 3.

To be sure, not everyone is going to want 30% in Alternatives; but for the segment that does, there are lots of variations that one could consider.

Our goal, among others, in this note is to create a basic framework allowing all investors to begin to better appreciate some of the trade-offs between return, liquidity, risk, and inflation protection that various asset classes provide, while emphasizing Private Equity

- Private Equity generally outperforms Public Equities in almost all environments except the ‘low inflation/low growth’ regime. In high inflation periods, for example, PE has generated returns in excess of about 6% above public stocks. Interestingly, Private Equity’s excess returns are actually greatest when Public Equities deliver low returns.

- Infrastructure and Real Estate assets often have inflation indexation embedded in their cash flows; the replacement value of their assets also increases in a rising nominal GDP environment.

- Private Credit may potentially improve the return and risk profile of a traditional portfolio, as its floating rate feature may help boost the income-generating component of the fixed income allocation in a rising rate environment. It can also act as a portfolio diversifier and can shorten duration in many instances.

If you’d like to read their analysis of what drives Private Equity outperformance, definitely read this report.

Fast forward to their September 2023 publication, Regime Change: The Changing Role of Private Real Assets in the ‘Traditional’ Portfolio,

To review, in our first article in this series in May 2022, we argued that Real Assets could help enhance returns of the traditional 60/40 portfolio by providing more upfront yield, enhanced inflation protection in this new macroeconomic environment that we continue to envision.

Central to our thesis is that liquid government bond portfolios, which in the past have traditionally served as shock absorbers or diversifiers, may no longer fulfill this purpose.

This view has been reinforced by the behavior of the bond market in both 2022 and 2023, driven by sticky services inflation, Japan exiting Yield Curve Control, and Fitch’s downgrade of U.S. debt

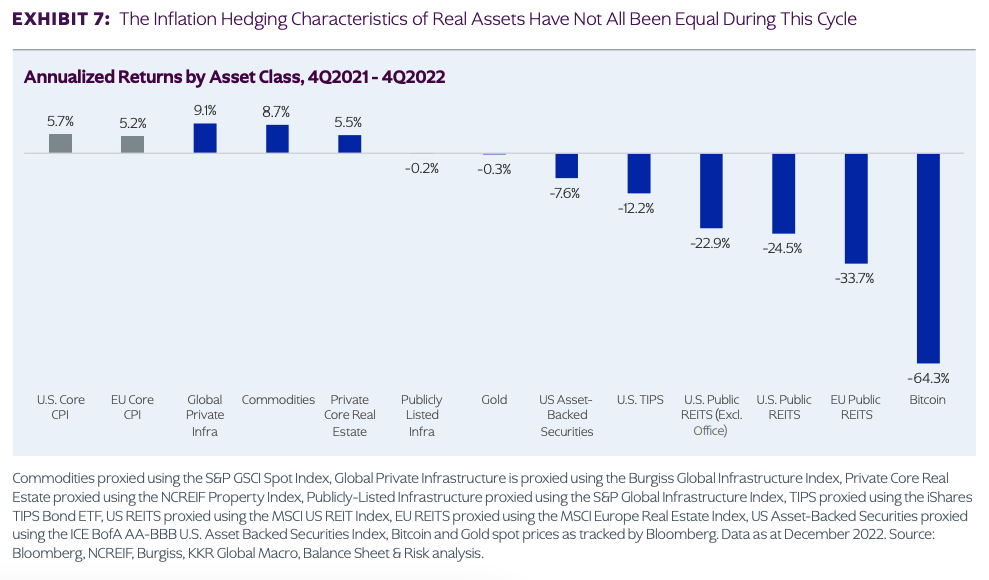

However, even for those who are already believers in our narrative, there is another important wrinkle to this story to consider: Not all Real Assets are created equal, in our view.

One can see from Exhibit 7 that many of the more ‘accepted’ inflation hedges such as TIPS and REITs have not performed well this cycle.

As a result, allocators could have been right on their inflation call but wrong on their choice of asset class, possibly by relying too much on what worked in the past.

By comparison, many Private Real Assets have delivered both strong upfront yield as well as a compelling total return during one of the fastest increases in both interest rates and inflation that we have seen in 50 years

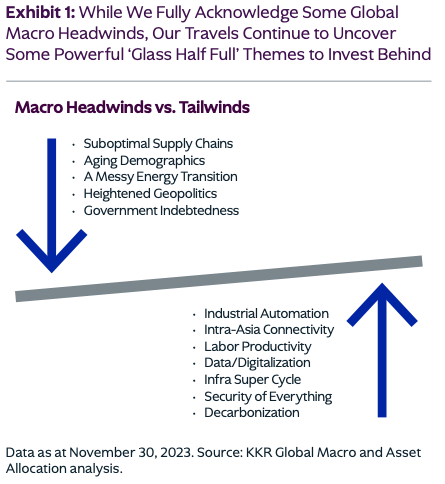

Now, let’s fast forward again to the firm’s 2024 Outlook, “Glass Half Full”,

The four key pillars of our Regime Change thesis – a sizeable fiscal impulse, sticky labor costs, a messy energy transition, and a fundamental restructuring of global supply chains – all argue for a different approach to asset allocation, we believe, including a meaningful reduction in the role government bonds can play in a diversified global portfolio.

Importantly, though, we still think that too many people are locked into the paradigm that the S&P 500 is trading at lofty headline valuations and the U.S. economy is topping out and headed for a hard landing.

As a result, they are sitting idle, as they feel there is little to no value in the market beyond Cash (i.e., despite a strong year in risk assets, there is still a record $5.6 trillion of assets in money market accounts).

From our perch at KKR, we also believe that the opportunity set to invest behind some of the biggest mega-themes we have seen in years keeps the ‘glass half full’ for global allocators.

Importantly, many of the investment opportunities we are highlighting also serve as compelling investment hedges and/or foils to some of the ails in the global economy these days (Exhibit 1)

While I can’t speak definitively whether or not the four pillars mentioned in this report were mentioned in previous communications…

The point is to show the evolution of this thesis over time, as the firm continues to develop its thinking and incorporate new happenings into their assumptions.

The firm even notes this, explicitly stating,

To date, our Regime Change approach to asset allocation, including being short duration, owning collateral, and being higher up in the capital structure, has served us well. In fact, it has largely been a one-way trade in our favor.

However, buyer beware in 2024: Next year will be different for two reasons. For starters, we are uniformly above consensus on growth (except in Europe) and uniformly below consensus on inflation (except in Japan).

So what is the firm promoting as their asset classes of choice?

Collateral-based cash flows such as Infrastructure, Energy, Asset-Based Finance, and Real Estate Credit.

Our research continues to show that many individual and institutional investors are still underweight Real Assets, especially Infrastructure and Energy, during a time when the need for inflation protection in portfolios remains high.

We are also encouraged that investors are ‘expanding’ the definition of infrastructure to include more operational improvement stories. We really like having this additional value creation lever in a high and/or rising rate environment.

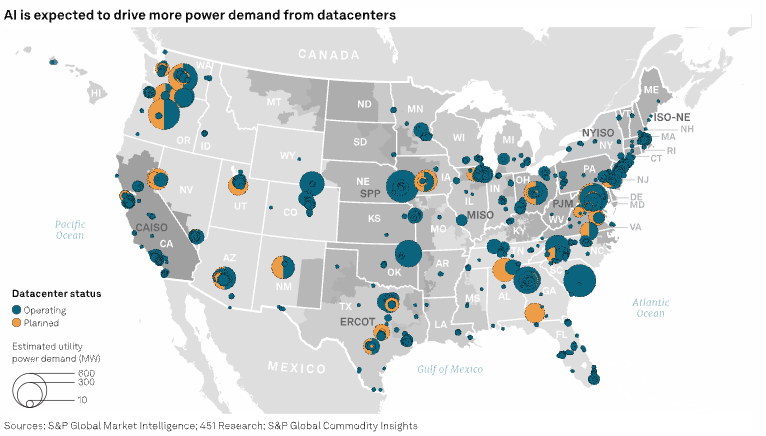

While most investors are focused on the semiconductor angle of the current AI boom, KKR is focused on the energy demand required by these systems.

Against this backdrop, they are bullish on critical energy transmission assets, data centers, and cooling technologies.

All told, some estimates suggest that the servers used in model training and inference could consume an additional 2.5 gigawatts of data center annually by 2024, which represents an increase of 10 – 15% to the current 19-gigawatts TAM (Exhibit 24).

According to Stephen Oliver, vice president of corporate marketing and investor relations at Navitas Semiconductor, “From 2023 to 2030, we are looking at about an 80% increase in US data center power demand, going from about 19 GW to about 35 GW,”

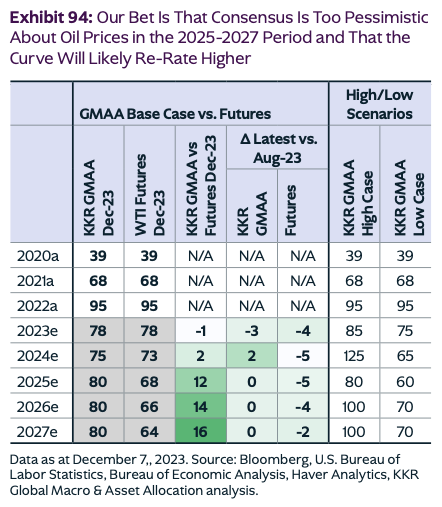

Supporting this thesis is KKR’s oil forecast that ‘$80 is the new $60’ as a midpoint for WTI oil prices in coming years.

If this is the case, we could see some major action in US shale producers in terms of free cash flow and return on equity.

The key driver is their expectation that the global supply/demand balance will flirt with a modest surplus in the first half of 2024 – even after the approximate 0.9 million barrels per day of additional OPEC+ ‘voluntary’ cuts for 1Q24.

And this leads us to what the firm calls the “Three C’s”

- Shale Consolidation: In an oil price environment like the current one, KKR thinks shale production growth today is approximately half of what one would have expected pre-pandemic.

Also, given the current hostility shown by the Biden administration towards the oil & gas sector, this creates a logical setup for consolidation as E&P managers focus on cash flow.

- Production Costs: The PPI for oil and gas drilling has increased more than 20% since 2019, yet long-dated oil futures prices remain in the $60-70 range, where they centered in the 2017-19 era.

- OPEC Control of Incremental Supply: Modest growth of U.S. Shale production may leave OPEC in the driver’s seat of incremental global supply.

OPEC has demonstrated a preferred price range of $70-100, with interventions most likely to occur outside those bounds.

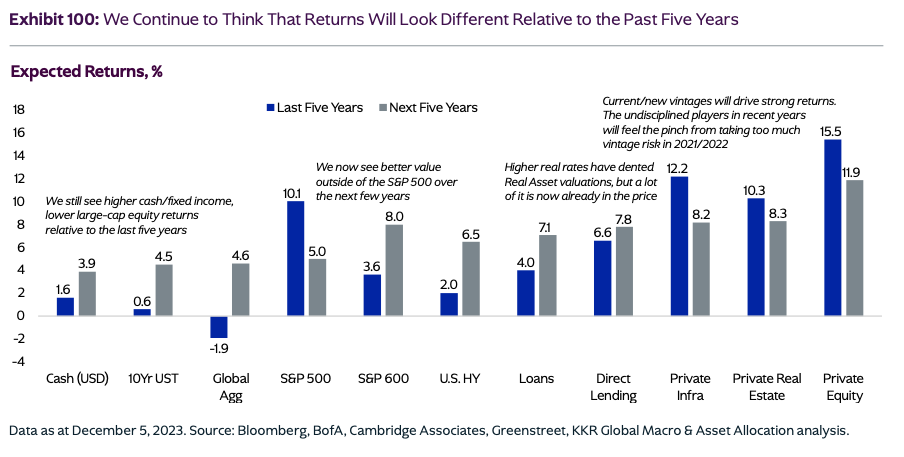

Meanwhile, the firm believes private market valuations now look more reasonable compared to public markets.

Specifically, the public markets are still adjusting to an environment of higher-for-longer rates, and parts of the next twelve months will feel like a typical downturn (including a potential fixed-income rally).

As such, KKR believes that investors who pull back on deployment today will miss out on some very compelling vintages.

KKR’s advice? “Keep it Simple” and stay focused on quality and less on risk, but still deploy capital thematically.

What Did You Think About Today’s Issue?Select an option below and send us any feedback you have. We’re always looking for input from our readers on how we can improve our editorial.

|

| Login or Subscribe to participate in polls. |