Last week, I ran a free investor education webinar called “Intro to Pre-IPO Investing” (which you can watch here).

Even though it’s 2 hours of training content that will help you quickly get up to speed on the basics of Pre-IPO investing…

We didn’t get a chance to dive into the finer details of what has to happen in order for a company to complete the IPO (and by extension, give investors an opportunity to cash out).

So today, we’re going to take a look at a topic that might be on your mind.

How do mining & exploration companies go public?

When most people think about IPOs, they think about high-flying, venture backed tech companies.

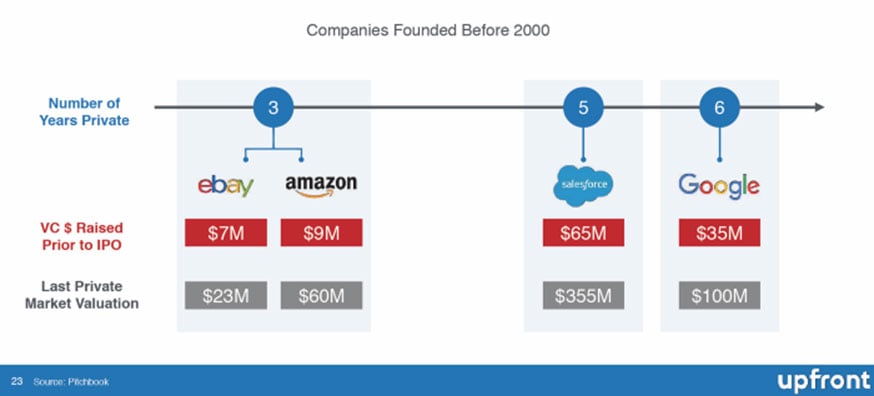

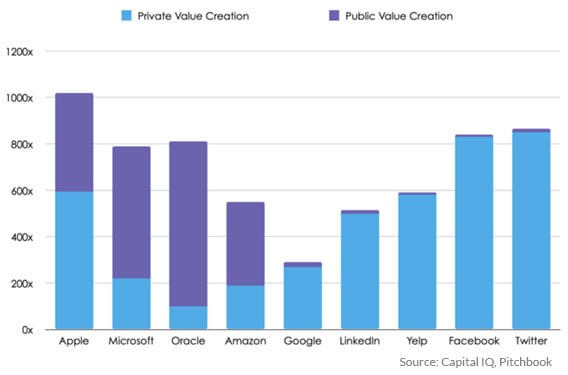

Once upon a time, the best companies IPO’d somewhere between 3-7 years after formation.

Why? Because at the time, it was the best way for smaller companies to get access to significant sums of capital.

As a result, most of the value capture happened after the company went public.

But all that’s changed over the past 20 years…

Since the dot com bust in 2000, trillions of dollars have flooded out of the public markets and into the private markets – providing funding to fuel growth until private companies are farther down the value chain.

That’s why more companies have been staying private, for longer…

And it’s why retail investors have been locked out of some of the most exciting companies they’d have normally had access to a few decades ago.

With access to hundreds of billions of dollars in early stage capital, companies are staying private for an average 10-12 years…

And their valuations can be in the billions before they ever reach the public markets.

What does this have to do with mining and exploration companies you ask?

Because mining and exploration is an incredibly capital intensive business that takes years – even decades – to prove out, if it ever does.

But unlike the tech ecosystem that has trillions of dollars chasing after private deals…

Mining deals still rely on the public capital markets for an important source of fundraising.

For this reason, it means we typically see junior miners quickly go to public markets to get access to capital…

And when they do, they are almost always pre-revenue companies that need (and burn) large amounts of cash to execute their business plan.

That’s why investors need to have proper expectations when investing “Pre-IPO” into mining and exploration deals…

The IPO is more of usually a fundraising event than an exit event.

With that in mind, let’s talk about some of the key considerations every mining company faces when deciding to go public.

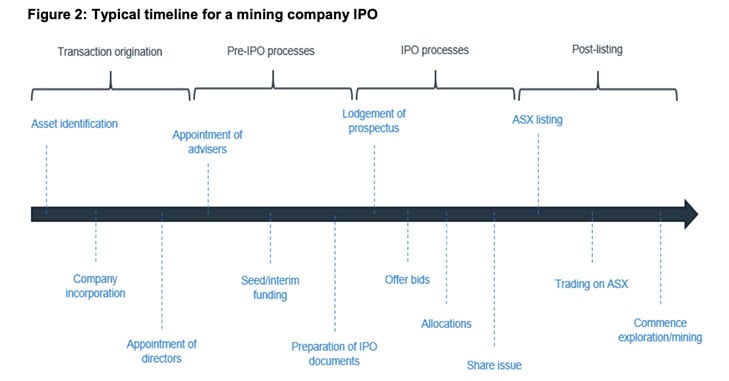

Source: “REPORT 641 An inside look at mining and exploration initial public offers” written by the Australian Securities and Investments Commission, published Dec 2019

Source: “REPORT 641 An inside look at mining and exploration initial public offers” written by the Australian Securities and Investments Commission, published Dec 2019

Phase 1) Transaction Origination

In this phase, we have:

- Asset Identification

- Company Incorporation

- Appointment of Directors

In the beginning, there needs to be some sort of mineral asset in play.

In some cases, the asset is discovered through “greenfield” exploration – which essentially means a new discovery from scratch.

However, it’s more common that an existing asset is acquired through some sort of transaction, or a new discovery is made near a known deposit.

According to a report released by the Australian Stock Exchange (ASX), there is an active primary market for mineral assets where:

- Individuals or small entities acquire and hold mineral assets and approach lead managers or other professional advisers for support for listing; or

- Professional advisers, in particular lead managers, seek out mineral assets to put together a portfolio of mineral assets for listing.

Phase 2) The Pre-IPO Process

In this phase, we have:

- Seed funding

- Appointment of advisers

- Preparation of IPO documents

Arguably, the most critical portion of the Pre-IPO process is acquiring seed funding for the project.

Not only will the company need capital to pay for the costs of going public, they often need some sort of funding to start operations. This could include some early “boots on the ground” exploration work as the company works to prepare a technical report – usually prepared by a “Qualified Person” – that describes the potential value of the mineral asset(s) being listed.

The exact format of the report will differ depending on which listing venue the company decides to go public.

For example, roughly 47% of all mining companies are listed on the Toronto Stock Exchange (TSX). In order to list on the TSX, all mining companies are required to submit a technical report called the National Instrument (NI) 43-101.

For listings in the U.S. (i.e. the Nasdaq or NYSE), mining companies were required to submit technical reports under the rules of Industry Guide 7. However, because of the global adoption of mining disclosure standards based on the Committee for Mineral Reserves International Reporting Standards (CRIRSCO) standards, the SEC is replacing Guide 7 with CRIRSCO-based codes (which is a more complicated topic we don’t have time to cover).

Once they have these documents in place, the next step is to hire an investment bank to act as adviser and underwriter for the deal.

Once this happens, the SEC’s rules impose strict limitations on communications around a planned IPO – which remain in effect up to 25 days following the pricing of the IPO as underwriters continue to sell shares.

Specifically, SEC regulations prohibit communications – outside of a normal course of business – that improperly solicit the securities to be offered in an IPO.

For companies used to being transparent and running active PR programs, these restrictions can be frustrating.

However, violating the SEC’s communications restrictions — often called “Gun jumping” — can cause an offering to be delayed for weeks or even months, or even canceled.

These restrictions apply to every corporate communication, from press releases and social media posts to marketing campaigns and simple emails – anything that could be considered intentional or unintentional solicitation.

These rules can cause significant friction, especially for companies that are used to being transparent and have active PR programs and investors who are used to receiving information.

Regardless, once this process begins, the underwriter is now responsible for preparing promotional materials, pitching potential investors, and otherwise determining the price of the stock.

Based on a variety of factors, the investment bank can also provide guidance on strategies for going public.

One option is to go public through the traditional IPO.

However, they can also take the company public by merging with an already public shell. This is commonly called a Reverse Takeover (RTO) and is similar in function to the recently popular Special Purpose Acquisition Corporation (SPAC).

For the purposes of this article, we’ll assume the company is planning a traditional IPO.

For new listings, each trading venue has different listing standards to qualify. One of the most important is the requirement around the number of shareholders, how many shares they own, and the total amount of freely tradable shares (sometimes called “Spread Requirements”).

Because most mining companies raise less than $10 million at the IPO, they could likely raise the amount of capital relatively easily from their existing network.

However, to meet the shareholder requirements, they often invite retail shareholders into the deal.

For this reason, we see Regulation Crowdfunding as an obvious mechanism for smaller issuers to meet the Spread Requirements.

Phase 3) The IPO Process

In this phase, we have:

- Lodgment of prospectus

- Offer bids

- Allocations

- Share issue

At this point, the company officially begins its “Road to IPO” (so to speak).

And with it come certain expectations from the regulators around public communication.

Assuming the company goes public in the United States, they would be required to file a Form S-1 registration statement with the Securities and Exchange Commission (SEC).

Once this happens, the company management team, investment bankers, and lawyers go on something called a roadshow – a series of presentations, where potential institutional investors will ask questions about the company to gather investment research.

Management teams must not offer any new information that is not already contained in the registration statement but can provide some level of informational gathering.

That’s why it’s critical the team has a well-crafted presentation and an “Equity Story.”

When it comes to raising capital – especially for early-stage ventures who often lack meaningful revenue – the message can often be what makes or breaks the deal.

Why? Because the message needs to be crafted for the right moment in time to attract the right type of investor to the deal.

If you’ve been following our editorial for the past few months, you know that we are bullish on ESG in Mining

In the private markets, valuations and share prices are set in a somewhat “ad hoc” manner – in the early stages, there’s some guess work involved around assumptions being made, and investors don’t have access to all the information.

In the public markets, all information must be disclosed and the share price is eventually determined by the market – the stock is worth whatever the market will bear.

However, in this specific stage, it is determined by the investment banks ability to sell the deal to their book of clients.

The lead manager will seek Offer bids – which is an offer to buy X amount of stock for $y – from all of the potential investors.

According to Bill Gurley, legendary venture capitalist and general partner at Benchmark…

When a company goes through a modern IPO process the bankers expressly tell the company that the “target” demand-supply ratio should be 30-50X oversubscribed.

Then, the lead manager will Allocate the shares to specific parties, based on whomever they like best in that list of potential investors.

Then, the lead manager will Issue Shares to those investors and the official IPO begins the next day.

Phase 4) Post-IPO Offering

In this phase, we have:

- Listing

- Trading

- Operations

Once the company is officially listed, now secondary trading begins.

The first 25 trading days of any newly listed security is a key metric of success or failure for any stock.

The last thing any newly trading company wants is their stock price to crash in the first month of trading.

For this reason, companies hire marketing, advertising, and/or public relations firms to help generate positive information – or “News Flow” – to influence share price performance.

The public promotional methods include setting up social media accounts, email ‘blasts’ from investor forums and platforms, and the use of quasi-news platforms with ‘sponsored content’.

But getting to the public markets is only the beginning of the company’s journey.

Long term shareholder value isn’t created by short term speculation. It’s created by discovering and developing mineral assets.

Because mining companies typically don’t have revenue– nor will they have any in the near term future – this means they are 100% reliant on outside funding to continue operations.

This means setting proper expectations with investors about key milestones in the prospectus – and efficient and effective Use of Funds – is key to continuing to drive shareholder value (and by extension, the stock price and any future fundraising efforts).

Additionally, this also means acquiring investors who are long-term focused and understand the nature of mining plays… not short-term speculators who want immediate gains.

However, in order to continue to keep investors engaged and interested in a longer-term hold, it often means an ongoing marketing and PR effort to continually generate more “News Flow” to existing and potential shareholders.

Final Thoughts

Regardless of where a company decides to go public, most experts agree it takes 12-24 months to properly prepare for a public offering… and anywhere between 3 – 9 months to fully execute the IPO.

Developing new mineral assets can take tens of millions of dollars in funds – and 5-10+ years – to properly develop.

However, a major discovery can provide potentially extraordinary long-term returns for investors who have the patience.

Sincerely,

Jake Hoffberg – Publisher

Equifund