If you’re interested in investing in exciting medical technologies (MedTech) that can potentially lower healthcare costs, improve patient outcomes, and deliver shareholder returns…

Chances are, you’ve seen countless advertisements about how robotics, machine learning (ML), and artificial intelligence (AI) are going to be a gamechanger.

And you’ve no doubt had the opportunity to invest in MedTech deals that claim they are the future of medicine as we know it.

But are they? And if they were, how would you – an everyday person who probably doesn’t have a medical degree, or any relevant experience in surgery – even know?

That’s exactly what we’re going to explore in today’s issue.

How to Cut Through the Hype When Evaluating Deals

For some context, before I came to Equifund, I spent ~5 years working for a large publishing company that sells information about exciting investment opportunities to retail investors.

And the most important thing I learned about marketing investment opportunities?

The exciting ideas that get the most clicks are rarely the best performing investments.

But unfortunately, when you’re in the entertainment business (and I use that word on purpose), you’re at the mercy of the dreaded “hype cycle.”

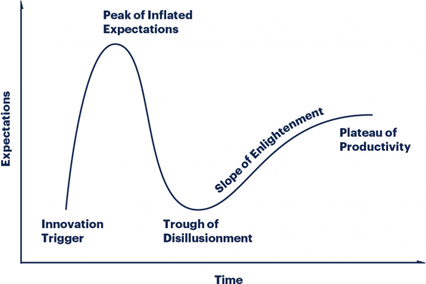

Coined by the preeminent research firm, Gartner, the hype cycle describes how emerging technology goes through five key phases.

- Innovation Trigger: A potential technology breakthrough kicks things off. Early proof-of-concept stories and media interest trigger significant publicity. Often no usable products exist and commercial viability is unproven.

- Peak of Inflated Expectations: Early publicity produces a number of success stories — often accompanied by scores of failures. Some companies take action; many do not.

- Trough of Disillusionment: Interest wanes as experiments and implementations fail to deliver. Producers of the technology shake out or fail. Investments continue only if the surviving providers improve their products to the satisfaction of early adopters.

- Slope of Enlightenment: More instances of how the technology can benefit the enterprise start to crystallize and become more widely understood. Second- and third-generation products appear from technology providers. More enterprises fund pilots; conservative companies remain cautious.

- Plateau of Productivity: Mainstream adoption starts to take off. Criteria for assessing provider viability are more clearly defined. The technology’s broad market applicability and relevance are clearly paying off.

What does any of this have to do with investing? A whole lot, it turns out.

As an investor, it’s incredibly tempting to invest in “what’s hot right now.”

Why? Because it’s hard work to have a long term view of the markets and have the discipline to buy undervalued assets with growth potential.

So, in an effort to skip over a lot of the boring (and hard) work that goes into due diligence…

We tend to look for shortcuts: What do the so-called “experts” say?

And by “experts,” I mean “people trying to sell you something.”

Don’t get me wrong. It’s way more fun to read about futuristic technology being created by larger than life founders that promise riches beyond your wildest dreams…

But just because a company has fancy buzzwords and slick marketing campaigns doesn’t make it a good investment.

And just because other people are throwing stupid amounts of money at similar companies with absurd valuations…

That doesn’t mean you should blindly jump into whatever is being pushed right now as the “next big thing.”

After nearly two years of total insanity in the markets, hopefully retail investors are starting to learn this lesson (again) as we see public market valuations take a nosedive.

That’s why I’m not surprised to see these headlines hitting the mainstream media.

So what the heck does any of this have to do with robotics and ML/AI in MedTech?

It all comes back to one of the keys to investment success.

The Courage to Be Contrarian

You’ve probably heard the Buffet quote: “Be fearful when others are greedy and greedy when others are fearful.”

It’s one of the cornerstones of being a contrarian investor (which means to go against popular opinion).

But as Reid Hoffman – founder of LinkedIn – says “It’s actually pretty easy to be contrarian. It’s hard to be contrarian and right.”

Why? Because a lot of things have to go right in order to create shareholder value and investment returns.

- Your market thesis needs to be directionally correct…

- The company you’re investing in needs to have enough skill, capital, and luck to capture market share…

- The broader market eventually has to come to the same conclusion you did in order to continue driving valuation metrics.

But even if you get all three of these things right, your eventual returns are largely determined by the deal terms and valuation you’re getting when you invest (i.e. your entry point).

In my opinion, one of the single hardest places to get this right is in pre-revenue MedTech companies.

Unlike tech companies that can quickly – and cheaply – stand up a minimum viable product…

The “move fast and break things” ethos in tech doesn’t work well when people’s lives are on the line.

It’s expensive to not only develop new technology… but get regulatory clearance/approval to sell it.

According to Pitchbook, it costs an estimated $31 million to develop a new device through the 510(k) Clearance pathway, and $94 million devices going through the PMA pathway.

As you may imagine, the more expensive it is to develop a new device, the more pressure there is to recoup those costs. This means there’s a serious conflict of interest for healthcare systems that are trying to lower healthcare costs and improve patient outcomes.

However, on the flip side, the high barriers to entry come with government sponsored monopolies (i.e. patents) that can be the foundation for significant long term financial returns…

Not to mention the possibility of literally transforming human history by easing suffering, speeding recovery, and potentially curing diseases once and for all.

In my opinion, investing in Life Sciences (i.e. pharmaceuticals, medical devices, and health care) is perhaps the most underlooked and underappreciated ESG investment there is.

Aside from the environmental problems we face, Life Sciences is arguably the highest stakes – and highest total reward – industry we can be investing in today.

So how does this apply to surgical robots, AI and ML in medtech?

For starters, robots are crazy expensive. The da Vinci robotic system costs about $2 million…

And robotic surgery generally costs anywhere from $3,000 to $6,000 more than traditional laparoscopic (aka “minimally invasive”) surgery.

“One thing is certain: The da Vinci hasn’t improved patient outcomes as dramatically as the first wave of minimally invasive surgery did.

To justify its price — roughly 10 times that of a traditional laparoscopic surgery — da Vinci would need to do a lot better overall.

In order to make the purchase of a da Vinci Surgical System feasible, hospitals must perform anywhere from 150 to 310 procedures within six years to offset upfront and ongoing costs.”

And this doesn’t even take into consideration the cost – and time – it takes to train surgeons on new technology.

When it comes to learning how to perform minimally invasive spine surgery – which is what the KDL suite of tools is designed for – spine fellows need to perform at least 40 – 80 pedicle screw placements to achieve proficiency.

That’s just to learn how to get the screws in correctly!

Pedicle screws are used sometimes in a spinal fusion to add extra support and strength to the fusion while it heals. Pedicle screws are placed above and below the vertebrae that were fused. A rod is used to connect the screws which prevents movement and allows the bone graft to heal.

To gain proficiency in minimally invasive transforaminal lumbar interbody fusion (TLIF)? 44 procedures.

And that’s using methods that have been around for decades!

But what requirements do surgeons have when performing robotic surgeries?

According to the same healthline article…

“Some hospitals may require surgeons to perform three robotic surgeries before giving them the okay to operate on a patient with a robot.

Others may require 50 or 100 operations.

Hospital policies are not routinely disclosed to the public… [and] device manufacturers aren’t required to train doctors on their equipment”

But the real problem? The hype cycle!

Companies need to justify the huge cost of developing these new technologies…

And that means they have to sell patients, physicians, and providers on the idea of robotic surgery.

How do they do this? Simple. Advertising and Media/PR campaigns.

According to Dr. John Santa, medical director at Consumer Reports Health: “Americans tend to think that the latest and greatest technology has got to be better, and it’s not in this case”

And this puts healthcare providers in a bit of a dilemma…

Do they cave to the hype and buy the robots in order to get patients through the door?

Or do they continue to use proven methods for performing high risk surgical procedures (like spine surgery)?

It’s not a simple question to answer, especially given the very real shortage of surgeons we’re looking at here in America.

According to Merritt Hawkins, there will be about 24,350 orthopedic surgeons in the U.S by 2025, but a projected demand for 29,400 — representing a deficit of 5,050.

This means healthcare systems are under a very real pressure to do more with less.

The allure of performing more procedures with fewer, high-skilled surgeons is definitely appealing…

But will robots, AI and ML deliver on the hype?

Or is there a hidden “low tech” solution that could take its place?

Investing in the Third Option

Dr. Kleiner – the founder and CEO of Kleiner Device Labs, who is raising capital on the Equifund Crowdfunding Portal – has performed over 6,000 spinal surgeries during his 25 year career.

During that time, he became progressively more focused on decreasing the amount of post-operative pain that his surgical patients experienced.

However, the minimally invasive techniques that surgeons wanted to perform were hampered by instruments that created longer procedures and worsened the outcome.

That’s why he decided to start creating his own tools to make it easier to perform minimally invasive spine surgery that reduced pain for the patient.

You won’t find any space age technology in this device. In fact, there’s not a single piece of electronic hardware to be found!

Instead, it’s a “back to basics” approach designed for surgeons, by surgeons, to help make traditional minimally invasive spine surgeries easier, faster, and cheaper to perform.

The company’s first device – the KG 1 – has already proven to be effective in this task; fusion success rates improved from 75% to 92%.

Their second device – the KG 2 – recently received 510(k) Clearance, and their upcoming “Alpha Launch” is scheduled to begin sometime in Q1-2022.

And tomorrow, Wednesday, February 2nd @ 2pm PST/5pm EST, we’re going to be interviewing Mike Hughes – Chief Commercial Officer at Kleiner Device Labs – to get an update on their vision for 2022 and beyond (click here to RSVP).

Sincerely,

Jake Hoffberg – Publisher

Equifund