The Digital Health sector is on fire right now.

There’s been more public exit announcements in Q1 than all of last year combined, with more than 80% exiting via “special purpose acquisition company” (SPAC).

And while we remain huge advocates of companies exiting via the public markets vs mergers and acquisitions…

Choosing the right vehicle for going public – traditional IPO, SPAC, or direct listing – can have serious impacts for investors looking for returns.

Today, we discuss the pros and cons for digital health companies looking to exit the private markets and enter the public markets using SPACs.

But first, a quick backstory on how we got to where we are today.

The Beginning of the Digital Health Boom

If you’re new to investing in healthcare companies, here’s the important thing to know…

In 2015, we saw the height of digital health M&A with a whopping 188 acquisitions.

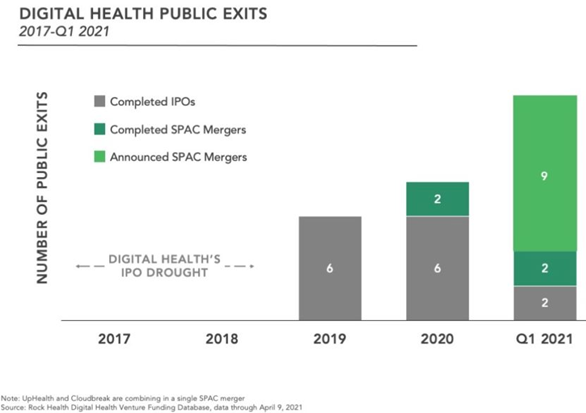

In 2016, 2017 and 2018, there were zero public exits in the digital health sector. But then, after a three-year drought, six digital health companies hit the public market in 2019.

Livongo, Health Catalyst, Phreesia, Change Healthcare, Peloton, and Progyny.

According to venture firm Rock Health…

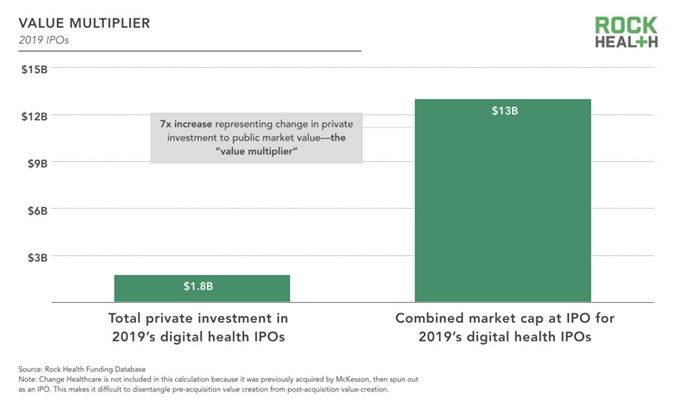

Excluding Change Healthcare for a moment (since it was previously acquired by McKesson1), the founders and employees at the five other companies used $1.4B of investors’ capital, and their own sweat and tears, to turn five great ideas into companies worth $13B at IPO.

This 7X increase is a helpful, if somewhat artificial, way of thinking about the total “value multiplier” these companies achieved with the capital provided by their investors.

Now, that 7x return is calculated across all investment dollars in vs market cap created… not what an early stake in any of these companies would have been worth at IPO…

But this initial flurry of exit activity changed the landscape for digital health companies; In 2019, 113 digital health companies exited via M&A (40% less than in 2015).

Then, in 2020, the pandemic added jet fuel to the digital health ecosystem:

- Startups raised a record-shattering total of $14.1B in venture funding—1.7X more than 2018’s previous high water mark.

- Six digital health IPOs and seven announced or completed SPAC (Special Purpose Acquisition Company) deals. Additionally, there were 145 acquisitions of digital health companies in 2020, up from 113 in 2019.

- Traditional healthcare players doubled down with significant moves such as Boehringer Ingelheim’s $500M deal with Click Therapeutics and Phillips’ $2.8B acquisition of BioTelemetry.

- Enterprise disruptors such as Best Buy, Walgreens, CVS, Salesforce, Amazon, and Walmart continued to invest in the $3.5 trillion healthcare market opportunity.

- The now famous Telehealth-Livongo merger that kicked off the Digital Health Platform wars.

And now, in 2021, we’re seeing what could be the tipping point for major public exit activity across the entire digital health ecosystem.

Which brings us to the point of this email…

The Case for Digital Healthcare SPACs

Without going deep into the weeds about how SPACs work… people known as “sponsors” put together this vehicle to raise money from investors.

Then, they go look for companies to buy using the money they just raised, of which they usually only have an 18 – 36 month window to complete the transaction.

This means there is a very real time pressure for these sponsors to find deals!

And this is where the problems start for SPAC investors…

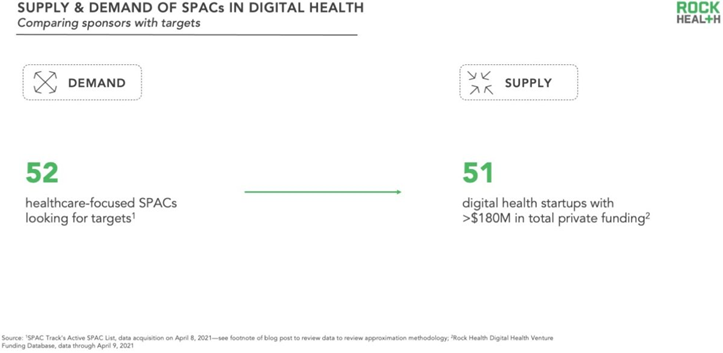

Why? Because there’s no escaping the laws of supply and demand.

According to Rock Health…

We found approximately 52 healthcare-focused SPACs, at least three of which have publicly stated an interest in digital health targets.

The average trust value (or funds raised by the SPAC) of the 52 relevant SPACs comes to $234M. Per the 80% requirement, they’ll need to spend a minimum of $187M on a SPAC target.

To assess supply, we looked at the most highly-capitalized digital health companies, assuming that this is the cohort most likely to be planning an exit.

According to Rock Health’s Digital Health Venture Funding Database, 51 digital health startups have raised at least $180M in total private funding to date.

But here’s the thing about SPACs most investors don’t really understand…

The SPAC sponsor typically stands to gain 20% of the public company once the deal is complete.

This means they have a heavy incentive to get any deal completed – even if it’s over-valued – to avoid giving the money they raised back to the investors!

And with more money chasing less qualified companies… there’s a real risk of taking a company public that isn’t ready for it.

Generally speaking, if a company is considering going public via SPAC, it means they should have already considered going public via traditional IPO or direct listing routes…

But there’s an interesting reason why some digital health companies choose the SPAC route.

According to Dawn Whaley, President of Sharecare….

“As a digital health platform, we have a complex and comprehensive story and the SPAC process allows us to explain it in detail. Additionally, the SPAC vehicle allows us to focus on the look forward financials and the potential growth in our model.

We selected a partner with great experience in capital markets and very successful SPACs who understands our mission and business.”

Now, as the publisher here at Equifund, I’m all for companies taking greater control over their media narratives…

But in my opinion, they need to start that process way sooner than the “hey, let’s go public” decision.

And the single best way to do that? Crowdfunding and the “Customer/Shareholder Flywheel.”

Because there’s simply nothing better than having a core group of loyal customers who love your product… AND who also own your stock and are advocate for your company.

While it does take a lot more foresight and effort to build compelling media narratives for early stage companies (of which we help all of our issuers on our portal build)…

The end game is a long-term branding exercise that allows any company to tell their story for years before their exit, and help them boost their chances of success in the public markets.

Sincerely,

Jake Hoffberg – Publisher

Equifund