While everyone else is talking about the Dow Jones Industrial, S&P 500, and Japan’s Nikkei 225 hit new all-time highs, Nvidia having the largest single day market cap gain in history, and Reddit’s plans to go public on the NYSE…

Here are the stories that haven’t been getting much attention.

- Despite the stock market exuberance, billionaires (like Jamie Dimon, Mark Zuckerberg, Bill Gates, and Jeff Bezos) and members of Congress (like Senator Tommy Tuberville) are all selling massive amounts of stock. Probably nothing.

- The North American Securities Administrators Association issues a letter opposing HR 2799 or the Expanding Access to Capital Act – legislation that is designed to help entrepreneurs and small businesses, while boosting the economy.

That’s what we’re covering in today’s Weekend Edition of Private Capital Insider.

Let’s dive in,

-Equifund Publishing

P.S. As a reminder, we cannot provide any individualized advice or investment recommendations.

If you need help, please consult with a qualified financial professional who is licensed to provide investment advice.

When Insiders Sell In Concentrated Markets

While this newsletter is primarily focused on what’s happening in private markets…

There’s simply no ignoring the impact public markets have when it comes to the majority of investor portfolios.

Especially when the paradoxical narratives we’ve been tracking – ”the most predicted recession of all time” and “Just Add AI!” – are battling it out.

But no matter how convincing any narrative sounds, inevitably, there needs to be a clear catalyst that forces a new consensus in the market (and therefore, new price discovery).

As usual, we do not make predictions, nor do we make buy/sell recommendations…

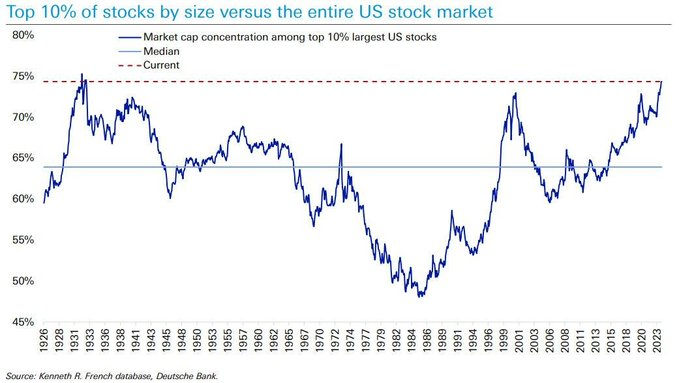

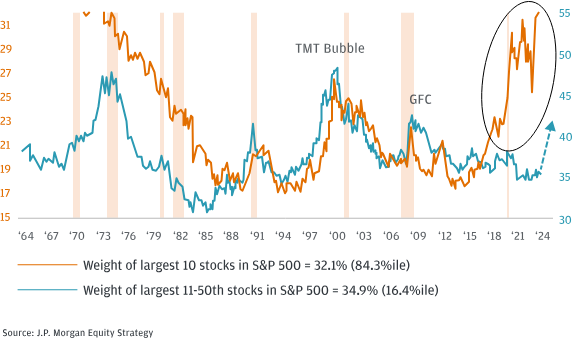

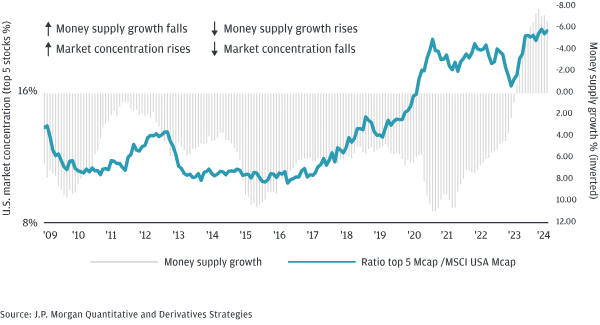

But we have to talk about the absurd concentration in the stock market right now.

At the time of publishing, the top 10% of stocks in the U.S. now reflect ~75% of the entire market – levels we haven’t seen since the Great Depression and Dot Com crash.

But more specifically, the top 10 stocks by market cap are ~30% of the entire market.

And to reiterate one of our key assumptions – that all market crashes inevitably begin due to a liquidity crisis – stock market concentration and liquidity have an inverse relationship.

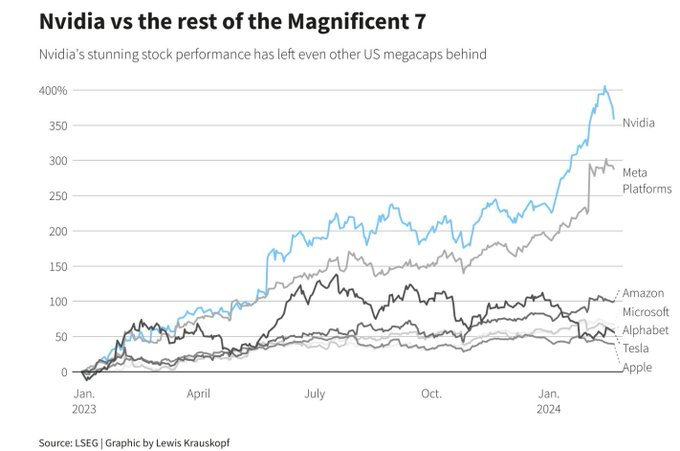

But where has all this money been concentrated?

The large capital investments required to build out AI and LLM infrastructure favor the largest multinationals. These companies should continue to win market share from smaller players due to massive economies of scale and their global footprint. For this reason, the investor excitement in the space has been persistent and relatively narrow.

Basically, it’s all gone into Nvidia and Meta (the “Just Add AI!” narrative winners).

Which, to our amusement, has produced some solid memes about the stock.

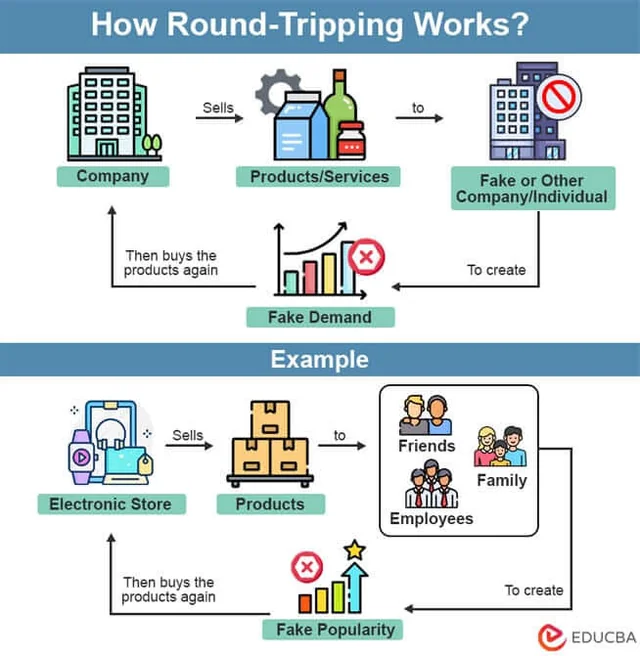

And just to make the Nvidia story a bit spicier, Nvidia is being accused of a fun financial engineering trick called “Round Tripping” – artificially boosting by making investments, or providing vendor financing, in (sometimes) fake companies, which then spend the cash you gave them to buy your products.

Nortel & Cisco’s collapse during the dot-com era by the use of “vendor financing,” where a vendor loans money to customers so they can buy their products…

Palantir was accused of doing this during the SPAC craze, losing ~$400m.

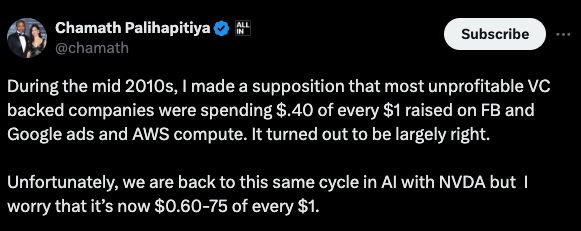

Speaking of SPACS, even SPAC King Chamath Palihapitya is further stating that a huge amount of VC money being put into startups eventually winds up at Nvidia.

- Jeff Bezos: $8.5 billion of $AMZN

- Mark Zuckerberg: $428 million of $META

- Jamie Dimon: $150 million of $JPM, marking his first sale since taking the helm in 2005.

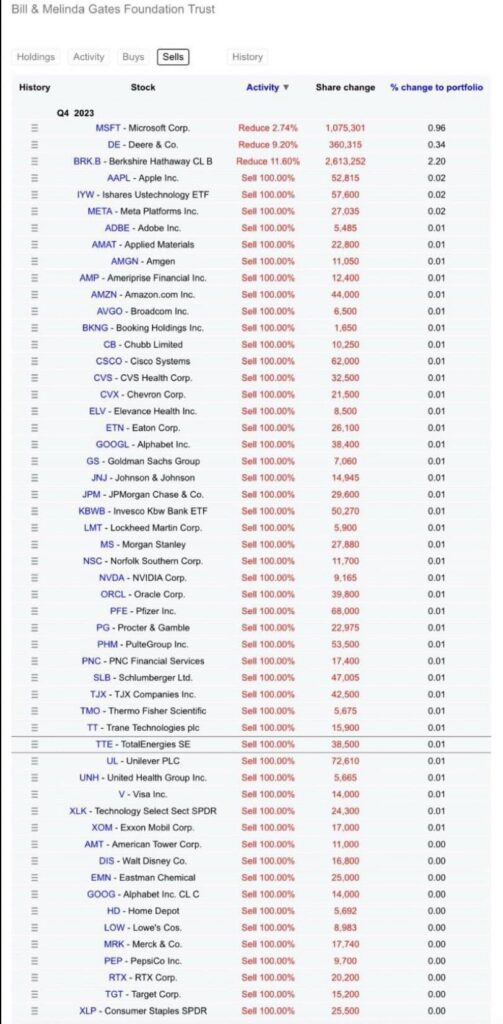

Not to mention, the Bill & Melinda Gates Foundation, as per their 2023-Q3 13F filing, has apparently wholly divested from stocks of Apple, Meta, Amazon, Alphabet, and Nvidia.

To be fair, rich people selling stock doesn’t mean there is a crash coming…

But when they have a track record of conveniently selling right before a major crash happens, maybe we should pay attention?

Either way, in order for the momentum in the market to shift and cause sentiment collapse, there needs to be some sort of catalyst (or event) that triggers it.

As is typical for crisis periods, if the economy slips into a recession, market concentration should remain narrow and we would expect a rotation from cyclicals to defensives.

Only in a soft landing scenario would we expect leadership to broaden into smaller, lower-quality and cheaper companies

In the past, a steep rise in concentration and narrow leadership has always reversed, with the S&P 500 equal-weighted index outperforming the market cap-weighted index.

The peak in this concentration episode is likely to coincide with the inflection in the business cycle, recession and greater anti-trust regulations.

While I think we’re all assuming the “they” who run things won’t allow a major stock market crisis during the run up to the 2024 election…

We still are of the opinion that prioritizing downside protection and liquidity is often the correct posture to take for small-balance investors.

Remember, no one ever went broke selling too soon.

Now might be a good time to consider how your portfolio is allocated, whether or not you need some more defensive positions, or should otherwise increase your cash holdings.

As usual, if you need help with your specific situation, please consider contacting a qualified financial professional.

Rules and Regulations: Expanding retail investor access to private markets

In a previous Weekend Edition, we talked about the consortium of 15 bills floating through Congress known as the “JOBS Act 4.0”

Of those fifteen, four were passed by the House of Representatives in 2023:

- H.R. 2792, the Small Entity Update Act, sponsored by Chairman Ann Wagner (MO-02), would direct the SEC to assess regulatory costs of compliance for small and growing businesses, ensuring that regulations placed on these businesses are not overly burdensome.

- H.R. 2795, the Enhancing Multi-Class Share Disclosures Act, sponsored by Rep. Gregory Meeks (NY-05), would ensure shareholders receive more uniform information in proxy materials without prohibiting multi-class share structures altogether.

- H.R. 2796, the Promoting Opportunities for Non-Traditional Capital Formation Act, sponsored by Rep. Maxine Waters (CA-43), would empower underrepresented and rural small business owners to learn about capital formation opportunities.

- H.R. 2797, the Equal Opportunity for All Investors Act, sponsored by Rep. Mike Flood (NE-01), would increase the number of pathways to qualify as an accredited investor by instituting a test administered by FINRA, allowing sophisticated-but-not-wealthy individuals to access high-growth asset classes that would not otherwise be available to them.

Earlier this month, the North American Securities Administration Association (NASAA) published a letter to Congress opposing The Expanding Access to Capital Act (H.R. 2799).

As a quick refresher, the bill pledges to make a significant upgrade to Regulation A+.

How? By turbo-charging the maximum offering amount from $75M to a whopping $150M per year.

If enacted, it would be a seismic shift for Reg A+ and equity crowdfunding, making the exemption far more attractive to larger companies with hefty capital appetites.

H.R. 2799 also proposes a get-out-of-jail-free card for some low-revenue companies, allowing them to court accredited investors sans the tedious SEC registration process.

In a nutshell, it’s about making capital more accessible, and plentiful, for small- and medium-sized businesses.

So why is NASAA opposed to this? According to their letter,

NASAA strongly opposes four (4) titles in

H.R. 2799 because they would make it impossible or more difficult, depending on the bill in question, for state securities regulators to promote responsible capital formation and protect

investors in their states.

In short, the legislation would establish two categories of investment professionals, private placement brokers and finders, and allow them to engage in many activities that have for decades been regulated because of investor protection concerns.

This title would establish a registration safe harbor for private placement brokers.

To establish the safe harbor, the title directs the SEC to promulgate regulations that are “no more stringent than those imposed on funding portals” and “require the rules of any national securities association [such as the Financial Industry Regulatory Authority (“FINRA”)] to allow a private placement broker to become a member of such national securities association subject to reduced membership requirements.

Last and importantly, the Unlocking Capital Act would amend Exchange Act Section 15 to prevent state governments from imposing registration and other requirements on private placement brokers and finders that are greater than the new safe harbors.

Stated differently, state governments seeking to register private placement brokers would need to set up new bespoke registration and regulatory regimes for private placement brokers.

In addition, state governments could no longer require finders to apply to be registered or licensed with the state before they begin to solicit investors in the states

NASAA is the entity that represents state securities regulators, as well as regulators in Canada and Mexico.

Historically focused on investor protection, NASAA has been a consistent critic of investment crowdfunding, as well as improvements to the capital formation process.

While it’s easy to dismiss the concerns of NASAA as little more than a desire to protect their powers…

They present what we would consider reasonable objections, especially with regards to the looser registration requirements for “finders.”

However, if we look at the current state of FINRA revenue, it’s pretty obvious they are looking for new ways to generate revenue (which primarily comes from fines and license fees).

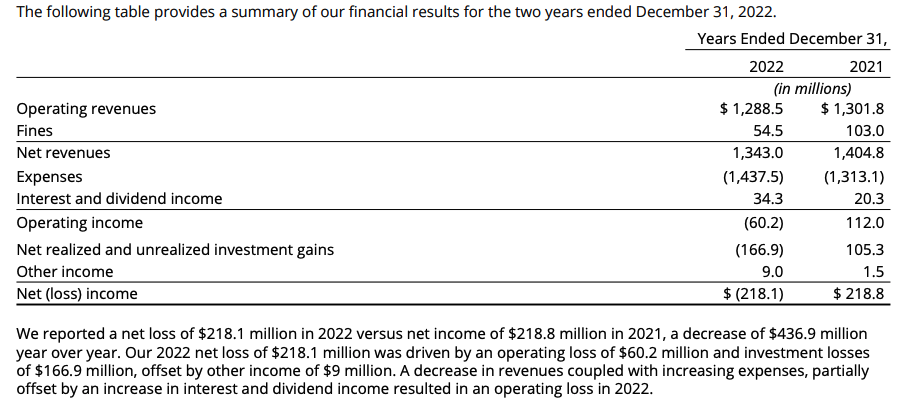

FINRA reported a net loss of $218.1 million in 2022, compared to net income of $218.8 million in 2021.

FINRA’s losses are concerning because they raise questions about the organization’s ability to effectively regulate the securities industry.

FINRA is supposed to be a watchdog for investors, but it is difficult to do that when the organization is losing money.

For this reason, one of the items we’ve long had on our Equifund Bingo Card is FINRA creating a new license for the swath of “creators” who publish financial-oriented content online…

Especially those who want to be able to legally get paid a sales commission on capital raised, when introducing an issuer’s stock to their audience.

But I digress from the main point of this article…

This week, the Grandfather of equity crowdfunding, Sherwood “Woodie” Neiss, issued a response to NASAA (note: we interviewedWoodie in 2022).

Neiss states:

Before Regulation Crowdfunding became law, opponents claimed that it would “make it easier for companies to cheat investors, ” or that it “sacrifices essential investor protections without offering any prospects for meaningful, sustainable job growth,”

Nearly eight years later, we can unequivocally state that those fears were unfounded.

In addition, it is arguable that given the vast bipartisan support of Regulation Crowdfunding, no ‘investor protection legislators’ would have voted in favor of a law that directs the SEC to promulgate rules to implement a path for issuers to circumvent applicable securities laws.

Conversely, Regulation Crowdfunding sets forth the most prescriptive exempt offering outside of Regulation A+ (which is qualified by the SEC).

It is most likely for this reason that

a) there has been hardly any fraud or enforcement actions in the marketplace,

b) fraudsters are deterred from the deep disclosure requirements within Regulation Crowdfunding, and

c) per NASAA’s letter there are much easier ways for fraudsters to take advantage of investors

Regulation Crowdfunding is successful because it has built-in investor protection mechanisms, disclosure requirements that do not exist elsewhere in the securities laws, and ongoing reporting requirements that benefit investors.

Selfishly speaking, we are, of course, in favor of anything that would benefit our core business at Equifund, attract more – and higher quality – issuers into the crowdfunding ecosystem, and allow more people to participate in those private offerings.

However, we also recognize that private markets carry significant risks that many individual investors simply aren’t aware of, or prepared to take.

What are your thoughts? Be sure to rate this issue, and leave us a comment on the poll.