For decades, retail investors have traditionally been the final exit strategy for institutions…

But now, as we officially enter the end of the COVID bull run, Wall Street is apparently warming up to what we see at Equifund.

Retail investors – also known by the moniker “Apes” – represent a $30 trillion market opportunity!

And in the face of massive “fee compression” across index funds and ETFs, Wall Street firms see “liquid alternatives” as a promising source of growth.

Major firms are already competing to capture investment dollars from the so-called “little guy”…

Source: Wall Street Journal, June 7, 2022

And thanks to new SEC interest in reshaping the US stock market… along with what appears to be a full on crypto winter…

We could be in for the most exciting decade in investing history as more “retail-ready” products hit the public stock markets.

But before we get into that, let’s talk about…

A Brief History of Retail Trading in America

On May 1, 1975, the stock market changed forever.

For the previous 183 years, brokers charged a fixed-rate commission for all traders, with no regard for the size of the trade.

This meant small-time investors paid a high percentage of potential profits in fees and commissions… which the Wall Street traders quite liked.

But then, on what is now referred to as “May Day,” the SEC decided to do away with this rule… and brokerage firms were less than pleased.

They argued that unregulated commission rates would weaken the exchanges and destabilize the securities industry.

In fact, the New York Stock Exchange (NYSE) even threatened to sue the SEC if it went through with the change.

But thanks to this “Great Unfixing,” stock brokerages were allowed to charge varying commission rates… and a brand new industry – the discount brokerage – was born.

Leading the way was Charles Schwab, who founded his namesake company in 1971.

The Charles Schwab Corporation began offering discounted stock trades on May 1, 1975, becoming one of the first discount brokerages.

Schwab believed individual investors would flock to lower prices, no-frills service and the independence of directly controlling their own trades.

Apparently, he was onto something big…

A decade later, the Wall Street Journal counted more than 600 discount operations luring away investors from conventional stock brokerages, fueling the so-called “democratization in stock market participation.”

As trading costs fell, more retail investors participated, fostering more competition for their business.

Then, in the 1990’s, we started to see the first real “explosion” of retail traders.

The introduction of cheaper personal computers – along with faster internet speeds – made it easier for individual investors to manage their own portfolio and trade stocks.

This, in turn, drove huge growth – and the IPOs – of several discount brokerages, including E*Trade and Ameritrade.

But where things really started to turn a corner was the mass adoption of the iPhone and the growth of the app store.

Early versions of mobile trading apps were clunky at best, but they delivered real-time quotes, news, and stock charts… along with an ability to make trades directly from your phone.

While most of the major incumbents were focused on targeting high networth individuals (believing that’s where the “real money” was), a tiny wealthtech startup had a different idea…

In 2013, Robinhood launched… becoming the first discount brokerage to offer commission free trades, aimed at the millennial generation.

In a flashback to May Day, this sent shockwaves through the trading industry.

Nearly every major online brokerage company had little choice but to follow suit and eliminate commissions for buying and selling stocks.

Shares of Schwab (SHCW), E*Trade Financial (ETFC), Interactive Brokers (IBKR) and TD Ameritrade (AMTD) all plunged on the news…

And eventually, it resulted in a forced consolidation phase as companies struggled to compete.

In 2019, Charles Schwab and TD Ameritrade combined in a $26 billion all-stock deal.

In late February of 2020, Morgan Stanley announced they’re going to buy E*Trade for $13 billion.

Then, COVID-19 changed everything again…

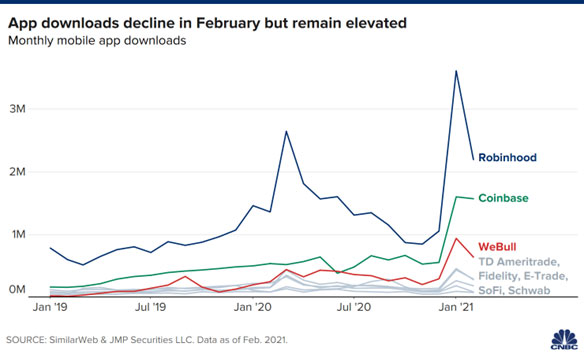

In 2020, 10 million Americans opened up a brokerage account.

In January 2021 alone, roughly six million Americans downloaded a trading app…

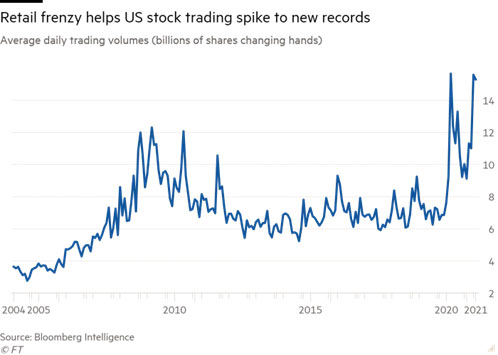

Retail brokerages reported record-high average daily volumes for equity and options trades...

Larry Tabb, a veteran market structure analyst at Bloomberg Intelligence, estimates that ordinary retail investors have on average accounted for 23 per cent of all US equity trading in 2021, more than twice the level of 2019.

This means retail investors in the United States generated about as much equity trading volume as mutual funds and hedge funds… combined!

Even though there’s speculation around whether this trend will or won’t persist, Wall Street can no longer ignore the power of the crowd…

And regulators are beginning to signal significant changes in an effort to protect retail investors.

“Right now, there isn’t a level playing field among different parts of the market: wholesalers, dark pools, and lit exchanges.

Further, the markets have become increasingly hidden from view. In 2009, off-exchange trading accounted for a quarter of U.S. equity volume. Last year, during the meme stock events, that share swelled to a peak of 47 percent.

What’s more, 90-plus percent of retail marketable orders are routed to a small, concentrated group of wholesalers that pay for this retail market order flow.

It’s not clear, with such market segmentation and concentration, and with an uneven playing field, that our current national market system is as fair and competitive as possible for investors.”

Chairman Gensler has asked the SEC to take a holistic, cross-market view of how they could update our rules and drive greater efficiencies in our equity markets, particularly for retail investors.

So far, they’ve outlined six areas for improvement:

- Minimum Pricing Increment

- National Best Bid and Offer

- Disclosure of Order Execution Quality

- Best Execution

- Order-by-Order Competition

- Payment for Order Flow (PFOF), Exchange Rebates, and Related Access Fees

And in a strange twist of irony, the SEC’s efforts to increase competition and providing more transparency may be the end of zero commission trading.

According to Sean Bonner, CEO of Guild Financial, a self-direct investment app that focuses on active and retired members of the military, a significant PFOF change…

“may reset the entire playing field and cost individual investors more money because we’ll have to go back to some sort of commission model.

I can guarantee you that commission model will be much higher than the rebates paying the payment for order flow — much higher, by a factor of 10s to 100s.”

It’s anyone’s guess as to what regulatory reforms the SEC will actually pass…

However, it seems reasonable to assume that the retail investor experience will likely change in the coming years ahead.

Most notably…

The Retailization of Private Markets

In the 80’s and 90’s, the establishment worried about the so-called “Barbarians at the Gate” as private equity rose to power.

But now, as institutional investors are saturated with PE/VC fund options, the Barbarians of Wall Street are about to face off against the Apes of Main Street.

Taking inspiration from the line “apes together strong” in the movie “Rise of the Planet of the Apes”… retail investors, calling themselves “apes,” believe if they are united, they can outlast those that are short on their favored meme stocks.

For the past decade, Blackstone – the world’s largest private equity firm – has been working on growing its retail platform; At the end of 2017-Q3, 18% of the firm’s $387.4 billion AUM was retail investors. [Note: Blackstone now has $915.5 billion in total AUM as of Q1 2022]

On the company’s 2017-Q3 earnings call, Joan Solotar – head of private wealth solutions at Blackstone – said: “There’s no reason that ultimately it won’t account for half the assets we manage” in the next 5-10 years.

Who do they think those assets will come from? According to Ms Solotar: “We are targeting the $1 million to $5 million investor. They are really under-penetrated in the alts business.”

Then, on January 14th, 2020, John Finley – Chief Legal Officer at Blackstone – gave a presentation to the SEC titled “Expanding Retail Access to Private Markets”

In it, he revealed some rather shocking numbers…

Retail investors represent ~$68T of global assets, with $1-$5m households representing roughly $30T of assets.

(1) CapGemini, Oliver Wyman, PWC, as of 2019. Retail measured across global households with financial assets >$1 million.

But that’s just the tip of the iceberg…

By 2025, the total pool of retail assets is expected to balloon to $106T worldwide!

And with an average 5% allocation to alternatives, even a modest increase to a 10% allocation could represent an extra $5.3T of assets shifting to alternatives.

If retail matched pensions at a ~30% allocation, it would mean an extra $26.5T of assets flooding into alternatives!

Combine that with the explosive growth of retail investors entering the markets since the start of COVID-19…

We could see a plethora of traditionally “off limits” private equity plays – like collateralized loan obligations (CLOs) and leveraged buy out (LBOs) – hit the public markets.

Blackstone, the industry behemoth that launched its first perpetual vehicle aimed at individuals in early 2017—a lower-cost nontraded real-estate investment trust—now sources nearly a quarter of its $915 billion in assets from private wealth. The firm has since added two more funds targeting individuals: a nontraded business-development company and a real-estate vehicle focused on Europe.

Blackstone, which expects to reach $1 trillion in assets this year, said in April it gets $4 billion to $5 billion of inflows a month from the three products combined.

In May, Blackstone filed with the Securities and Exchange Commission to launch a fourth fund, designed to offer individual investors access to its private-equity business, which would for the first time give them a slice of the big corporate leveraged buyouts the firm is famous for.

“It’s not lost on distribution partners—who are being approached by everyone under the sun—that competitors have seen Blackstone’s success and are jumping on the bandwagon,” said Solotar.

“It’s a land grab,” said Matt Brown, chief executive of CAIS, a platform that gives independent financial advisers access to so-called alternative investment products. “You’re seeing the mutual-fund boom 2.0,” he said, referring to the rise in popularity of mutual funds during the 1990s.

The Apes Are Here (and the opportunity is now)

Using venture capital firm NFX’s framework for a 3-sided marketplace, here’s how we see our growing ecosystem continue to build around three parties.

- Audience is retail investors looking for ways to diversify their portfolio, increase cash flow, and grow their net worth using alternative investments.

- Advertisers are companies raising capital (aka “Issuers”) through Reg-CF and Reg-A+.

- Content Producers are financial publishers and influencers (or “creators”) who generate revenue by selling ideas, usually in the form of “investment research” and “stock picks”.

Because of the highly regulated nature of securities, this 3-sided marketplace may have the potential for higher levels of defensibility than unregulated media markets.

Based on NFX’s Critical Mass Theory of Startups, there are three primary conditions for marketplace success, all of which we believe have been met:

- Condition #1) Economic impetus: Since 2000, money has been flooding into the private markets at record rates as investors continue to pursue the never ending “quest for yield.”

The Asset Management Advisory Committee (“AMAC”) – formed on Oct 9, 2019 to provide the SEC with diverse perspectives on asset management and related advice and recommendations – established a subcommittee to review retail investors’ access to private investments (the “PI Subcommittee”).

In their September 27th, 2021 report, the committee came to several important observations.

- There are several macroeconomic and structural factors that are resulting, and will likely continue to result, in:

- higher demand for investments and investment choices from retail investors; and

- a more concentrated supply of public market equity investment choices.

The three asset classes examined in the report are Private Equity, Private Debt, and Private Real Estate.

- Currently most retail investors are precluded from accessing many private investments due to restrictions relating to investor qualifications and the immaterial amount of private investments held by traditional retail investment vehicles.

Given the growing demand by retail investors, and the growing concentration of public equities…

The AMAC concludes:

“it is worthy to consider access to a wider range of investments for retail investors in order to better fulfill the growing demand for investment products and choice In particular, we believe that the SEC ought to consider wider access to private investments subject to;

- Such investments providing similar to or better returns than comparable public market investments; and

- Sufficient investor protection.

We’ve seen money flooding into the crowdfunding space at record rates over the past few years, confirming the thesis that retail investors want access to alternative investment products.

According to Crowdfund Capital Advisor, in 2020 capital commitments to Reg CF issuers rose by 77.6% from $134.8 million in 2019 to $239.4 million in 2020.

2021 was another year of records for the online investing industry. Over half a million Americans poured $570 million into 1,500+ offerings on Regulation Crowdfunding websites.

- Condition #2) Enabling technology: The JOBS Act is – in our opinion – the most underappreciated innovation in capital markets, and is the critical enabling technology that unlocks the potential of retail investments in alternatives.

While there’s certainly something to be said about blockchain and its potential impact on financial services…

It is our opinion that regulators will be far more likely to encourage development inside of this framework; investor protection has been a consistent talking point from politicians (like Elizabeth Warren) and both the previous SEC Chairman (Jay Clayton) and current (Gary Gensler).

We’re also seeing discussion drafts of the JOBS Act 4.0… which could continue to drive retail participation in private market assets.

However, there are still notable concerns with regards to the “limited due diligence being undertaken on the investment opportunity, as there is typically no professional manager between the retail investor and the issuer.”

Equifund seeks to solve this primary problem by enforcing strict due diligence and reporting standards as part of our listing requirements.

It is our opinion that eventually, investor returns will become the predominant indicator of success (or failure) of any marketplace, including Equifund.

For this reason, we’re already gaining traction with Content Producers who want to recommend exempt securities offerings to their audience; They rely on our expertise to perform proper deal structuring, due diligence, and customer service functions so they can focus on content.

But we find one of the AMAC’s suggestions particularly intersting:

“We recommend that the SEC limit retail access to private investments to those which have certain types of third-party participation. We refer to this Design Principle as “chaperoned access”.

We believe that chaperoned access will ensure that retail investors only invest in private investments that balance risk, returns, and appropriate fees.

Another way to achieve chaperoned access could be to require any private investment that retail investors have access to also have material participation in the fund or investment from more sophisticated institutional investors on substantially the same terms on the basis that such institutional investors would have carefully considered the risk and potential returns of the investment and the appropriateness of the fees being charged.”

Ironically, we see the primary barrier to “mass adoption” from retail investors in exempt securities offering – like Reg-A and Reg-CF – is adoption from institutional investors.

This brings us to…

- Condition #3) Cultural acceptance: Thanks to hit television shows like Shark Tank – along with the lionization of entrepreneurs and venture capitalists – retail investors want in on the private market deals they see in the media.

And perhaps more important, we’re seeing attitudes amongst the VC/PE crowd regarding crowdfunding change as well.

What was once a “last resort” for companies to raise capital is now being seen as a compelling growth strategy for companies who can use it correctly.

With this in mind, we see a huge opportunity for the rise of so-called “side-by-side” offerings where retail and institutions recognize that companies can benefit from having both types of investors participate in the early stages.

Final Thoughts

Why is the Equifund team bullish on retail?

First… As the African proverb says, “Alone we go fast, together we go far.”

With 200+ million retail investors in America – and ~11m households with $1m – $5m net worth – we see a clear opportunity to become the #1 alternative investment platform for retail investors.

Source: Spectrem Group, 2022 Market Insights Report

The end goal? A market network of founders, investors, financiers, capital markets professionals, and financial influencers that can serve as the growth engine for the next generation of high growth companies.

Second… a retail investor focused strategy could create the ultimate network effect that may potentially drive growth of the market, while building a defensible moat.

We call it The Customer/Shareholder Flywheel; Customers who love the product, become long-term Shareholders, and have incentives to help grow the company as an Advocate in the marketplace (i.e. generate referrals, write testimonials, and provide enhanced product feedback).

With this framework, the Equifund Community doesn’t just bring capital to the table when funding deals. We potentially bring hundreds – even thousands – of customers as well.

Third… with more than 40 years of combined experience helping small cap companies raise capital and go public, we know a thing or two about helping companies attract long term retail shareholders.

To do this, it requires a multi-year strategy that we call the Stock Market Slingshot: an iterative approach to fundraising that seeks to minimize dilution and maximize potential gains for early investors.

As a reminder, Equifund Crowd Funding Portal earns shares – at the same terms our members do – as part of our success fees for Regulation-CF.

This means we have a vested interest in making sure our Issuers do not put themselves in a position where they need financing due to poor planning… can’t raise capital at favorable valuations… and wind up accepting terms that hurt our position.

Also as a reminder, this doesn’t mean we can guarantee that any of our listings will flawlessly navigate the every-changing capital markets…

However, in the pursuit of building a truly “investor first” platform, we believe this helps create more aligned incentives for everyone in our community.

Sincerely,

Jake Hoffberg – Publisher

Equifund