For investors looking to “strike it rich” when a company goes public…

There’s a secret “table” inside every business that determines how much you get paid when they exit.

It’s called the Capitalization Table (or “Cap Table”)…

And if you don’t know how it works – and where you will be placed on the Cap Table when you invest in the current round…

You might wind up with far less than you thought if the company IPOs or gets acquired.

That’s why today, we’re going to talk about…

Cap Tables & Capital Stacks

When it comes to raising capital, most investors don’t realize that money – like any other commodity – can be purchased.

In the same way you can go to the supermarket (or grocery store) to buy groceries…

You can go to the Capital Markets to buy money.

But that money isn’t free. There is a Cost of Capital.

And just like any market, there are different buyers for different products, who will accept certain terms at certain prices, based on the risk profile.

Understanding how this dynamic works is really important for you as a private market investor!

Whether you realize it or not… as an investor, you are now a “vendor” in the Capital Markets.

And if you want your “investing business” to make money, it means you need to know…

- What type of Investment Products are out there (equity, debt, and exotics)…

- How to shop for those Investment Products (i.e. “valuation” and “deal terms”)…

- How those Investment Products are allegedly supposed to perform (i.e. the risk:reward ratio) and…

- How – and when – you get paid in the deal!

The answer is hidden inside the document all companies are required to maintain: The Cap Table.

This document lists out all of the share classes issued, who owns them, and how much they paid for their shares…

Which, in aggregate, shows how much the company is worth (i.e. the Market Cap).

Any time the company sells more equity, that Cap Table is updated to reflect the current reality of the business.

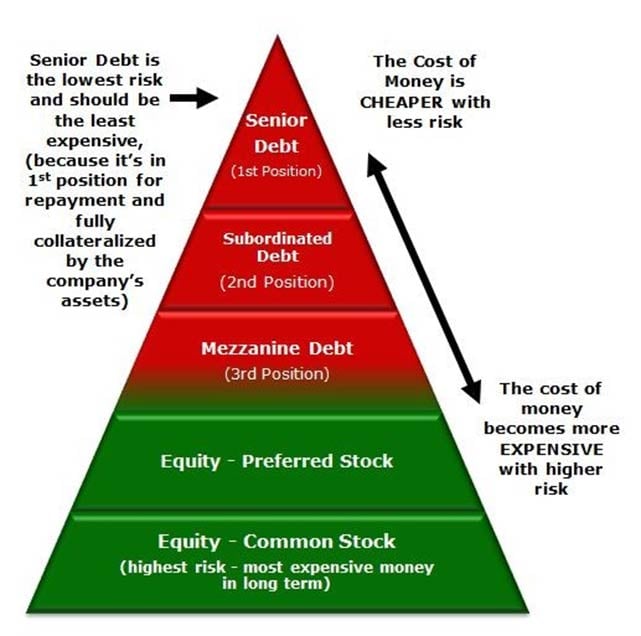

As the company raises multiple rounds of financing, it forms something called a “Capital Stack.”

And depending on where you are in the Capital Stack will determine when – and how – you get paid.

Here’s an example you might find yourself in…

Let’s say you buy Common Stock in an early-stage company at a $10m valuation.

After several rounds of financing, the company is now valued at $100m.

At this point, you might be thinking, “Great! I’m up 10x!”

But that’s not necessarily true. In fact, in most cases you won’t be able to cash out at a 10x return when the company exits.

For example, let’s say for whatever reason, the company is liquidated – either through bankruptcy or M&A – but only at a $50 million valuation (which is essentially a “down round”).

As a shareholder, you have a right to your fair share of the proceeds…

And hey, you suppose a “5x return” isn’t so bad.

But what happens next might mean you wind up with nothing!

Here’s why…

- Whenever a company is liquidated, people get paid back in a certain order (called the “Liquidation Preference”).

Technically, the tax man would get paid first, and employees are entitled to any unpaid wages…

But after that, everything is decided by the Cap Table and where you sit on it.

- At the very top of the stack are the Senior Debt holders.

Because this debt is secured by the company’s assets, it is the cheapest form of capital a company can buy.

Why? Because that debt is in “first position” to be repaid, which makes it the lowest risk.

This Senior Lender is often a commercial bank of some kind, and this Investment Product is typically a low risk, low return proposition for the bank.

For example, this could be a revolving line of credit or a term loan.

- Next up, is the Subordinated Debt

While subordinate is an unfortunately fancy word, it simply means they are next in line to get paid back.

Because of this, Subordinated Debt is higher risk, and therefore commands a higher interest rate than the Senior Debt.

These are typically things like high yield bonds (aka “Junk Bonds”) that represent a higher risk, higher return proposition compared to Senior Debt.

- Next up is something called Mezzanine Debt

Yet another unfortunately fancy word, but this debt is structured a bit differently than the first two…

Unlike Senior Debt and Subordinated Debt – which require the borrower to pay back the loan, plus interest, over a fixed period of time…

This lender typically wants an extra “kicker” to make it worth the risk because this type of debt is third in line.

Not only is the lender expecting some sort of cash repayment term on the loan…

It often comes with a provision that in the event of a default, the debt will convert to equity (called a Convertible Note).

It might also come with additional Warrant Coverage – which gives the lender the option to buy more equity in the company, at a fixed price, over a specified period of time.

[Editor’s Note: We’ll talk more about this specific type of financing in a future email, how we seek to protect our Issuers from taking predatory financing terms, and the opportunity we see going forward using Regulation-A+ to benefit from this deal structure]

- Preferred Stock is next in line after the debt holders have been paid.

As the name implies, Preferred Stockholders have a preference, and that preference is to get paid before other common shareholders.

Oftentimes institutional investors – like venture capitalists – will structure deals that involve them getting preferred shares with voting rights and board seats.

Because of the high-risk nature of early-stage companies, professional investors ask for these types of preferences to protect their investment.

Which, if you were investing millions of dollars of your own money into a risky startup, you’d probably ask for this as well.

Not surprisingly, early-stage companies don’t really like this “loss of control” that happens when taking VC money…

And is a major reason why founders are seeing crowdfunding as a way to maintain control of their company by inviting retail shareholders on the Cap Table instead of the “Sharks.”

And at the very bottom of the Capital Stack…

- Common Stock – the last to get paid

Generally speaking, the founders of the company – and their employees – are the ones who own Common Stock.

The reason why is simple: in the beginning, everyone on the Cap Table has ownership under the same terms as everyone else.

And if you’re wondering why the heck any investor would want to own Common Stock and be at the “bottom of the totem pole”…

It all has to do with the event we’re all hoping for…

What happens when the company goes public?

Before a company goes public, most usually equity shareholders – of all share classes – will be converted to one, single share class: Common Stock!

Why? Because in almost all cases, only Common Stock is the only class tradable on the public markets.

And as we’ve discussed in other articles, when a company goes public, your shares don’t magically appear in your brokerage account.

You have to go through a process to get them deposited in your brokerage account before they can be traded! (go here if you want to learn more about how that works)

And if for whatever reason, there is a delay in getting some share class converted into common stock…

It could mean you miss out on that “first-day IPO pop” you’ve heard so much about…

Or worse, not be able to sell out of your position at the price you want.

Have questions about Cap Tables, Capital Stacks, and Liquidation Preferences?

If so, hit reply and ask us anything.

We realize private market investing is more “complex” compared to the “Point. Click. Get Rich” type claims that you may see elsewhere…

But if you want to get in on the best deals before they go public… and get a piece of the returns you deserve…

Understanding the Cap Table – and the Capital Stack – is foundational knowledge for any investing you’ll ever do.

And even though it’s not a ton of fun to read the legal documents, all of this information has to be disclosed as part of the offering.

Don’t forget: you can always ask questions on the Investor Q&A forum below each offering if you have questions about any of this!

And of course, as long as you’re not asking for personalized investing advice…

We’re here to help you develop the knowledge and confidence you need to feel comfortable investing in Pre-IPO opportunities.

Yours for investing equality,

![]()

Jordan Gillissie – CEO

Equifund